This blog post accompanies the SDPB Monday Macro segment that airs on Thursday, August 11, 2022. Click here to listen to the segment, which begins at minute 22:30.

On August 7th, the U.S. Senate passed the Inflation Reduction Act of 2022, a 755-page bill that awaits anticipated passage in the U.S. House of Representatives and the signature of the President of the United States. Broadly speaking, the bill appropriates funds to energy reform motivated by concerns related to climate change, authorizes the federal government to negotiate some drug prices for Medicare, and imposes a 15-percent minimum corporate income tax on corporations that generate more than $1 billion of income annually. As of August 3rd, the nonpartisan Congressional Budget Office (CBO) estimated that, on balance, the bill would reduce the federal budget deficit by about $100 billion over the period 2022 to 2031; and increased tax-enforcement measures could reduce the deficit by about another $200 billion.

As a practical matter, passing a bill named the Inflation Reduction Act during a time of record high inflation is entirely unsurprising—an act of nature among legislators who prefer to do something about the inflation problem the U.S. economy currently experiences or, at the very least, to be seen trying to do something about the inflation problem, rather than to do nothing. As former Treasury Secretary Timothy Geithner was fond of saying to fellow policymakers who reasoned themselves unequipped to anticipate their policy responses to the economic destruction the global financial crisis imposed, plan beats no plan.

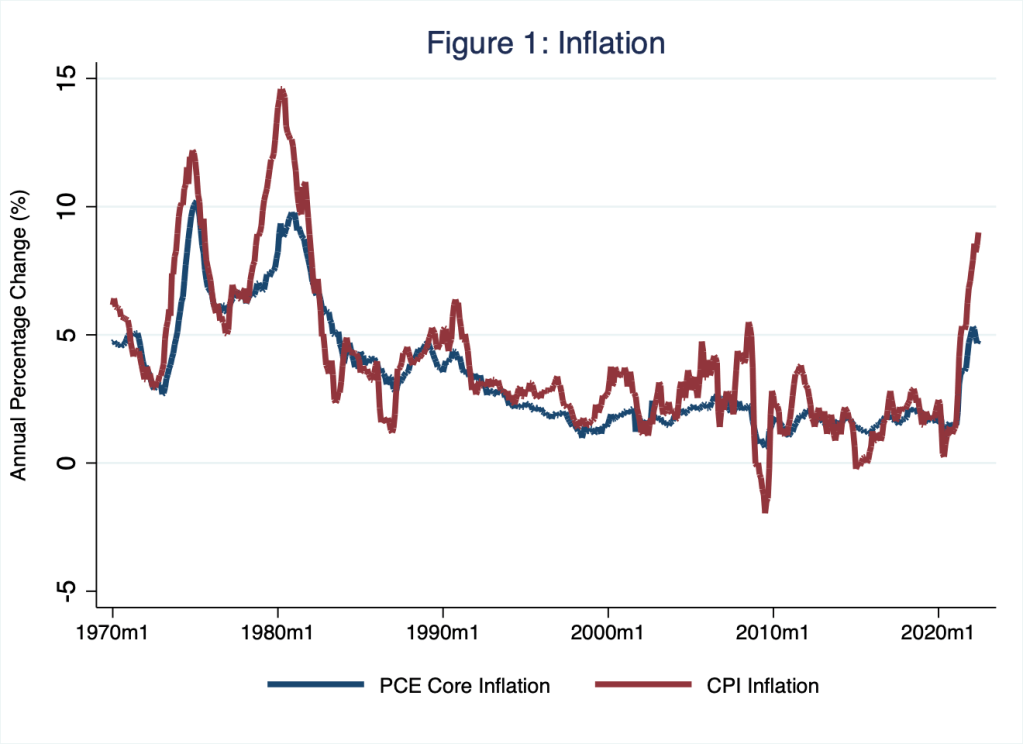

To be sure, the U.S. economy currently experiences relatively high rates of inflation. In Figure 1, I illustrate the rate of inflation according to the Federal Reserve’s preferred measure, a core, or underlying, rate of inflation based on a personal consumption expenditures (PCE) price index (that excludes food and energy), and the more-popular consumer price index (CPI).

In June 2022, the PCE measure I illustrate in Figure 1 registered a year-over-year rate of inflation of 4.8 percent, up from 4.7 percent in May. The Federal Reserve’s target for this measure is 2 percent, a rate the central bank and the vast majority of macroeconomists associate with low and stable inflation. Meanwhile, the more-popular (but less precise) CPI measure I illustrate in Figure 1 registered an alarmingly high year-over-year rate of inflation of 9 percent, up from 8.5 percent in May. To put the matter somewhat informally, the last time the red line in Figure 1 was as high as it is now, measured along the vertical axis, the U.S. economy was experiencing the so-called Great Inflation. (For more on the Great Inflation of the 1970s, see Monday Macro segment “That Seventies Show.”) Low and stable inflation, what macroeconomists refer to as price stability, is essential in a market economy, in which relative prices—the price of coffee relative to the price of tea or the price of gasoline relative to the price of coal, for example—rightly inform decisions of households, firms, and governments, provided the purchasing power of money is stable. Thus, price stability allows an economy to allocate resources efficiently.

No wonder policymakers prefer to do something about inflation.

Nevertheless, as a matter of principle, passing a bill named the Inflation Reduction Act during a time of record high inflation seems quixotic—an act of macroeconomic foolishness, assuming the purpose of the bill is to reduce inflation (which it patently is not). I say quixotic, largely because conventional macroeconomic theory does not identify fiscal interventions of the sort this bill comprises or otherwise as major sources of rising or falling inflation. The reasons are twofold.

First, the Inflation Reduction Act is essentially a fiscal intervention that combines allocation policies and redistribution policies. Allocation policies generally address productivity or market failures—such as the negative externalities that burning fossil fuels impose, for example. And redistribution policies generally redistribute existing income or wealth. The energy and drug-pricing reforms in the Inflation Reduction Act constitute allocation policies; the minimum corporate income tax constitutes a redistribution policy. Allocation policies are long-run interventions; such policies tend not to affect the economy in a measurable way in the short run. Thus, even if the allocation policies in the Inflation Reduction Act could reduce inflation—by making labor more productive and, thus, increasing output, for example—the allocation policies would take more time than policymakers have to reduce inflation. If timing is an issue, and it is because high and variable inflation begets higher and more-variable inflation, allocation policies are not the solution to our current inflation problem. And redistribution policies are interventions that tend not to affect aggregate demand significantly, because these policies shift existing income and wealth, rather than produce more of either, at least in the short run. Taxing Peter to pay Paul (no matter the merit of doing so based on objectives of equity and so forth) does not significantly reduce aggregate demand, which is necessary to reduce inflation. Incidentally, allocation and redistribution policies could be budget-deficit neutral, immediately or relatively soon after these policies are implemented; thus it is no wonder the CBO estimates that, on balance, the Inflation Reduction Act would reduce the federal budget deficit by about $100 billion over the period 2022 to 2031; in relation to the federal budget, $100 billion over ten years is essentially zero—budget-deficit neutral.

Put differently, then, the Inflation Reduction Act does not constitute fiscal policy, the only type of fiscal intervention designed to impose short-run consequences on the macroeconomy. Macroeconomists strictly define fiscal policy as government-funded macroeconomic stabilization policy that shapes the short-run features of the business cycle—those irregular fluctuations in aggregate economic activity including expansions and recessions, during which broad features of the macroeconomy deviate from their steady-state behaviors: unemployment or the rate of inflation rises above or falls below normal, say. For example, the roughly $4.7 trillion the federal government now-famously deployed in response to the recession caused by the pandemic qualified as fiscal policy. Incidentally, fiscal policy tends to affect the federal budget deficit, because such policies do not offset changes in spending with changes in taxes; for example, an expansionary fiscal policy increases spending but does not, then, tax it away. That the Inflation Reduction Act is largely budget-deficit neutral essentially reveals the act does not constitute fiscal policy in the strictest macroeconomic sense.

Second, fiscal interventions, including fiscal policies, are not the primary sources of inflation in any case. Rather, as economics Nobel laureate Milton Friedman (1912 – 2006) famously proposed, inflation is always and everywhere a monetary phenomenon. Thus, inflation is uniquely and ultimately an outcome of monetary policy. Monetary policy is a macroeconomic stabilization policy conducted by a central bank—as opposed to Congress—when it targets the money supply, interest rates, and aggregate demand to achieve macroeconomic outcomes, including low and stable inflation and full employment. According to monetarism, the strand of economic thought that Friedman promoted, inflation occurs because too much money chases too few goods; monetary policy targets the quantity of money, and so inflation is purely a monetary phenomenon, full stop. The glaring corollary of Friedman’s proposition is, of course, that inflation is generally not a fiscal phenomenon. (The exception here is the somewhat complicated and controversial fiscal theory of the price level [FTPL], in which debt-financed fiscal interventions are potentially inflationary if government deficits stimulate household spending, while the central bank sits by passively targeting interest rates. I do not focus on this theory in this post, because the theory is rather nuanced and because the Inflation Reduction Act is budget-deficit neutral.)

The argument that inflation is a monetary phenomenon relies crucially on the presumed relationship between the supply of money and its purchasing power and, in turn, on the relationship between the central bank and the supply of money. To understand how specifically the supply of money and the rate of inflation are related, and why reducing inflation is a macroeconomic policy that falls within the purview of a central bank, consider the following quantity equation.

M x V = P x Y

In this equation, M represents the supply of money, V represents the income velocity of money, P represents the average price level, and Y represents real income, which economists typically measure as real Gross Domestic Product (GDP). Velocity is a crucial feature of the quantity equation and the relationship between the supply of money and the rate of inflation more generally. Economists define velocity (V) as the average number of times the supply of money (M) is exchanged to purchase nominal income (P x Y). For example, suppose the supply of money in the economy is $50 (M); and during a year in the economy, 100 pens are produced, purchased, and valued at a price of $2 each (P x Y). In this example, the income velocity of money equals 4 (V): $50 of money pays for $200 of nominal income per year, because each dollar in the supply of money is exchanged on average 4 times per year.

The quantity equation explains how the supply of money affects the average price level and, thus, the rate of inflation, provided we assume why individuals hold—or, in the parlance of monetary economics, demand—money, as opposed to illiquid assets such as real estate or equity shares in corporations. Assume, as economists often do, individuals hold money in fixed proportion to their nominal income, so the velocity of money is constant over time. In this case, the supply of money and nominal income are proportional: a percentage change in the supply of money causes an identical percentage change in nominal income.

Finally, a portion of the percentage change in nominal income (P x Y) is reliably driven by non-monetary forces including changes in physical capital, human capital, the labor force, and innovation—long-run features of the macroeconomy that, to be fair to the Inflation Reduction Act, allocation policies could in principle affect, albeit with long and relatively unpredictable lags. Conceptually, controlling for the effects of these non-monetary forces on nominal income isolates the effects of the supply of money on the average price level: all else equal, the supply of money determines the average price level; or put differently, the growth in the supply of money is the principal cause of the rate of inflation.

Thus, as monetarist thinking (and much conventional macroeconomic thinking more generally) goes, the central bank fundamentally influences the growth of the money supply because the defining feature of a central bank is that it issues the economy’s monetary base. For example, in the case of the Federal Reserve System, the monetary base consists of Federal Reserve liabilities circulating as currency in the hands of the nonbank public or banks’ reserve accounts deposited at the Federal Reserve. Because the monetary base is the principal driver of the supply of money, and the growth of the supply of money is the principal driver of the rate of inflation, economists generally view inflation as an outcome of monetary policy.

In a letter dated August 4th, 2022, the CBO responded to four questions Senator Lindsey Graham asked the agency about the Inflation Reduction Act. One of these questions was, “How would enacting the bill affect inflation in 2022 and 2023?” The CBO responded, in part,

In calendar year 2022, enacting the bill would have a negligible effect on inflation, in CBO’s assessment. In calendar year 2023, inflation would probably be between 0.1 percentage point lower and 0.1 percentage point higher under the bill than it would be under current law, CBO estimates. That range of likely outcomes reflects uncertainty about how various provisions of the bill would affect overall demand and output, the supply of labor, the persistence of disruptions in the supply of goods and services, and how the Federal Reserve would respond to offset any increase in inflationary pressure. (Emphasis added.)

https://www.cbo.gov/system/files/2022-08/58357-Graham.pdf

Thus, the CBO estimates, rightly I reason, that the Inflation Reduction Act of 2022 would have a negligible effect on inflation; instead, inflationary outcomes will ultimately depend on how the Federal Reserve responds to inflationary pressures—always and everywhere a monetary phenomenon, indeed.