This blog post accompanies the SDPB Monday Macro segment recorded on Friday, October 11 and scheduled to air on Tuesday, October 15, 2024. Link to the segment, which begins about a minute into the broadcast.

We have gamified monetary policy, or so it seems.

Schooled readers know I am fond of a quarter-century-old quip by the former Bank of England Governor, Mervyn King, to the Plymouth Chamber of Commerce and Industry at its 187th Anniversary Banquet. King, then deputy governor of the bank, informed his audience, “Our ambition at the Bank of England is to be boring” (Balancing the Economic See-Saw, April 14, 2000). King explained, “A reputation for being boring is an advantage—credibility of the [monetary] policy framework helps to dampen the movement of the [economic] see-saw. If love is never having to say sorry, then stability is never having to be exciting.” Put differently, monetary policy should not distort—think, see-saw—otherwise-optimal free-market outcomes; when it comes to monetary policy, there should be nothing to see here.

Today, monetary policy is anything but boring; we talk incessantly about the policy and the macroeconomy the policy shapes. We debate the wisdom of a change in policy stance—think, expansionary (by lowering interest rates) or contractionary (by raising interest rates)—sometimes on the basis of little else than gut feeling or wishful thinking, as if we were playing a game. While monetary policy fascinates me, I am surprised it does not bore most, given the monetary policy framework to which Mervyn King referred: to wit, a modern central bank endeavors to achieve a set of macroeconomic goals like price stability and full employment, subject to constraints imposed by the economic system in which the central bank operates—think, in the short-run, achieving price stability may impose an employment cost. Typically, the monetary-policy instrument the central bank uses to achieve the goals subject to the constraints is a short-term interest rate.

For the Federal Reserve System, the goals of monetary policy—since a 1977 amendment to the Federal Reserve Act—are to achieve a dual Congressional mandate of stable prices (or, practically speaking, a low and stable inflation rate) and maximum employment (or, put differently, a low unemployment rate). And the monetary-policy instrument the central bank uses is the federal funds rate.

At its last meeting on September 17 and 18, the Federal Reserve System’s Federal Open Market Committee lowered its federal funds rate target 50 basis points from a range of 5.25 to 5.50 to a range of 4.75 to 5 percent. The monetary policy news junkies pounced. The business press has talked about little else since, except last Friday’s employment report—which indicated the labor market far outperformed expectations, creating 254,000 jobs in September; we expected something closer to 150,000—and Thursday’s consumer inflation report—which indicated mildly higher inflation than we expected. Maybe the Fed won’t loosen monetary policy after all? But they all but promised they would? Didn’t they?

We cannot get enough.

In theory, monetary policy is entirely boring: according to the first fundamental theorem of welfare economics, complete markets, complete information, and perfect competition together yield, absent policy interventions, Pareto optimal outcomes—those in which we cannot improve Person A’s welfare without reducing Person B’s welfare. We may not desire the distribution of Pareto optimal outcomes, but monetary theory is largely silent on remedies.

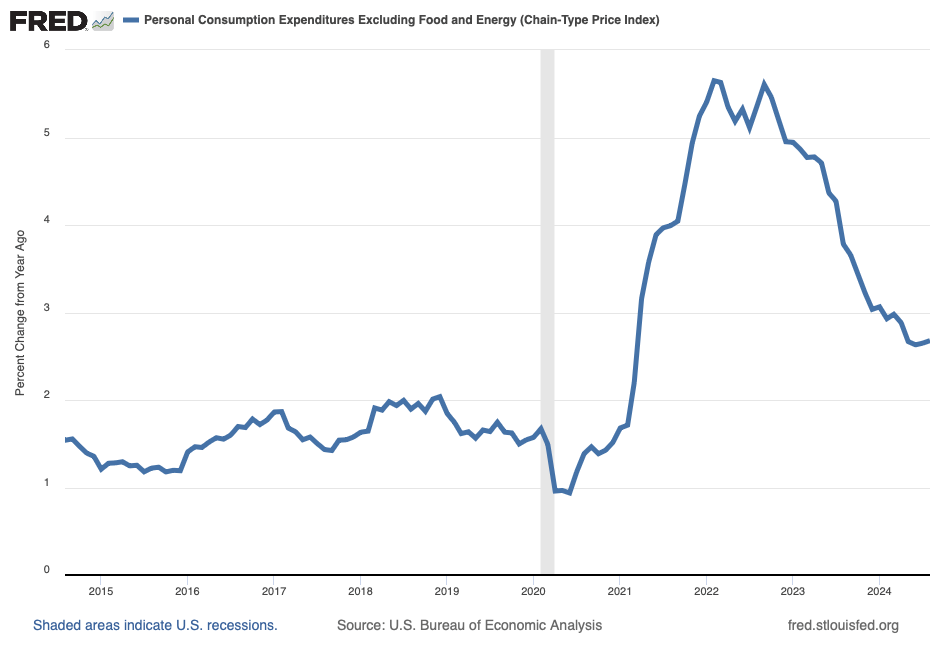

To be fair, and as Monday Macro listeners know well, in practice, monetary policy is not entirely boring. Rather money matters because the assumptions underlying the first fundamental theorem do not hold uniformly. Put differently, the societal impact of monetary policy is not trivial. Thus, advancing knowledge in the field improves our quality of life. In the last few years, distortions in the average price level caused by high and variable inflation have raised the cost of living and, concomitantly, lowered the quality of life of many households. In Figure 1, I illustrate the inflation rate according to the core personal consumption expenditures index, the Federal Reserve’s preferred measure of growth in the average price level.

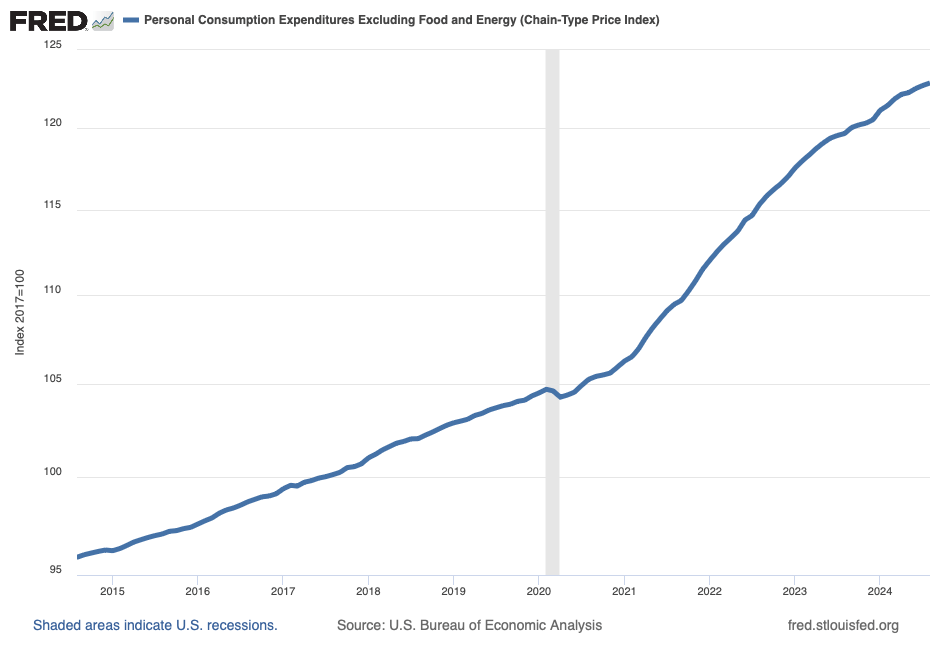

Although the inflation rate has returned to near 2 percent recently, inflation rates above 5 percent in the last few years raised the average price level persistently—the price of eggs is not coming back to levels achieved in 2020, for example. In Figure 2, I illustrate persistence with the average price level, which is much higher today than it would have been had the inflation rate achieved prior to COVID continued after COVID; the inflation rate I illustrate in Figure 1 is the annualized growth rate of the average price level I illustrate in Figure 2.

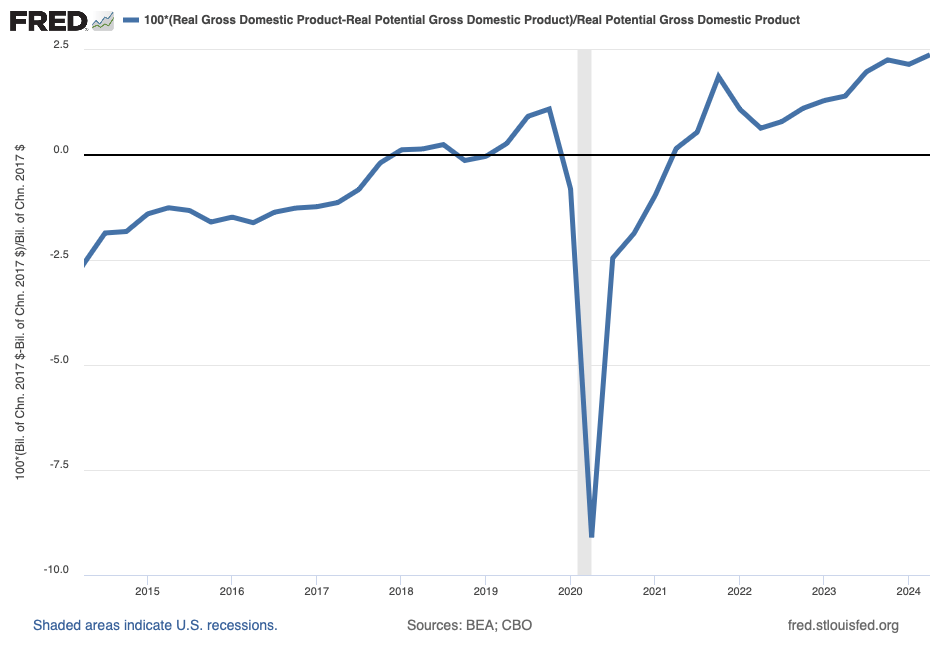

Meanwhile, as I illustrate in Figure 3, actual output has risen above potential output, which we reason the economy would achieve if all resources were fully employed.

Thus, over the last few years, monetary policy has overheated the economy, stoking inflation and pushing output to levels relative to potential that we had not observed in the years before COVID.

Perhaps not surprisingly, our experience motivated us to Google search for information about macroeconomic variables such as inflation (Figure 4) and unemployment (Figure 5), for example.

Numbers on the y-axes of Figures 4 and 5 represent search interest relative to the highest point in the figure for the given region and time. According to Google Trends, “a value of 100 is the peak popularity for the term.” Thus, in the last two decades, search activities for “inflation” and “unemployment” were never greater than during the pandemic (“unemployment”) or shortly thereafter (“inflation”).

Though I understand why monetary policy is not boring right now, I remain surprised by the degree of Monday-morning central banking, reckoning early and often whether the central bank will lower or raise rates, should lower or raise rates, and by how much. When did monetary policy become the subject of a parlor game?

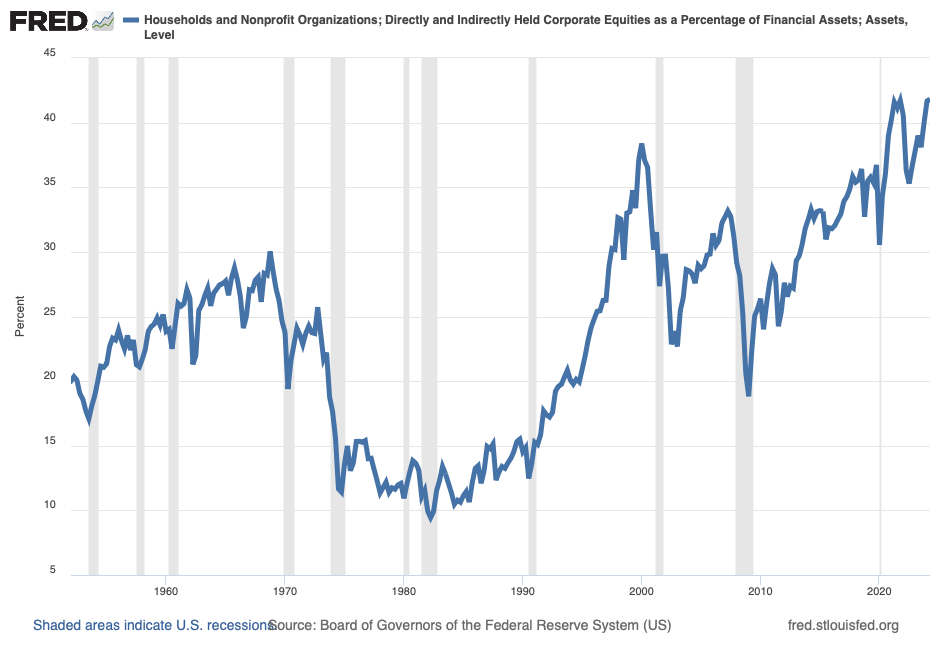

I propose the gamification of monetary policy is the result of a confluence of the ubiquity of informational and transactional technologies and the rising share of household financial wealth comprised of equities—think, stocks. The ubiquity of informational and transactional technologies is self evident, which you probably just read on your smartphone. Meanwhile, according to Figure 6, as of the second quarter of 2024, the share of household financial wealth comprised of equities registered 42 percent, the highest share on record; moreover, more households than ever before own equities (though the wealthiest households continue to own the majority of equities).

Thus, more than ever before, American households have motive, means, and opportunity to track and take positions in—to gamify—equity markets; simply swipe to buy, sell, or hold.

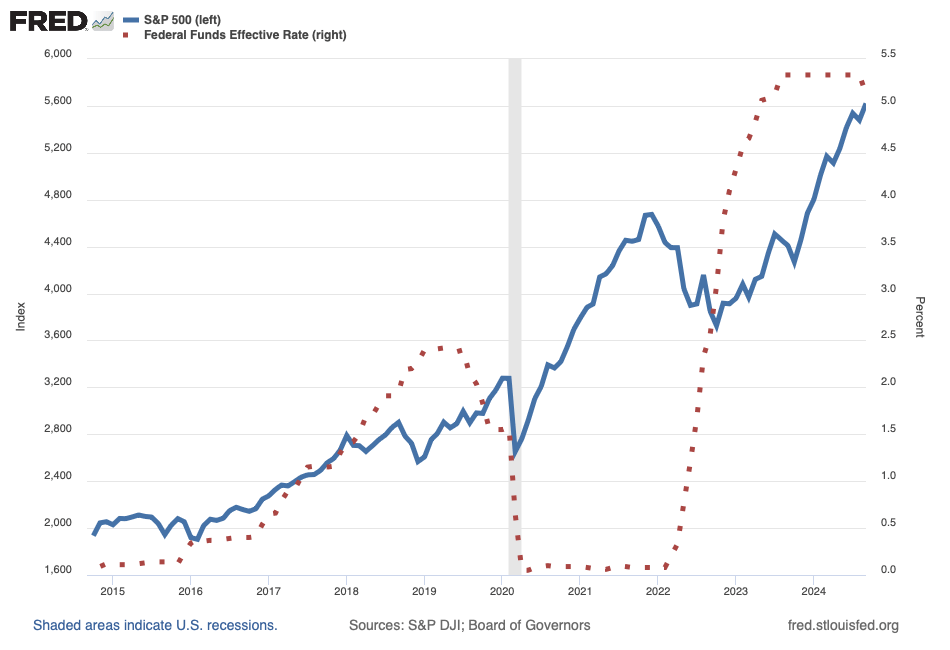

Thanks to the time value of money, the relationship between market valuations of equities—think, stock prices—and interest rates is reliably inverse: all else equal, when rates fall [rise], stock prices rise [fall]. In Figure 7, I illustrate the pattern using the S&P 500 stock index as a measure of stock prices and the federal funds rate as a measure of interest rates.

In my view, the informational and transactional technologies leading to the gamification of investing in the stock market have gamified monetary policy, as well. The culture’s preoccupation with the Federal Reserve target for the federal funds rate is less about whether the central bank has, say, reached the (counterfactual) neutral rate of interest—the so-called r-star at which the economy neither expands nor contracts from its long-run, steady-state, dynamic equilibrium—and more about whether the stock market will rise or fall in response to information we reason informs the central bank’s policy stance, reflected operationally in the bank’s target for the federal funds rate.

Given how the stock market responded to recent indications from the Federal Reserve that it intends to lower its target of the federal funds rate, I suspect Player One reasons lower interest rates are just what the economy needs. Imagine that.