This blog post accompanies the SDPB Monday Macro segment that airs on Monday, June 6, 2022. Click here to listen to the segment.

On July 12, 1987, the New York Times Book Review published a piece by Nobel Laureate, Robert Solow, who reviewed, Manufacturing Matters: The Myth of the Post-Industrial Economy, by Stephen S. Cohen and John Zysman (Basic Books, 1988). In his review, Solow noted that, like everyone—including himself—the authors could not explain why labor-productivity growth was falling during an ostensible technological (then-computer-driven) revolution. Labor productivity is a measure of the average level of output—think, stuff—produced per hour of labor input. The amount of capital, like the machines and tools with which we equip labor, and the production technology, the recipes with which we combine labor and capital, determine labor productivity. Over time, increases in the amount of capital and improvements in technology, including the computer-related capital and technology of the 1980s, grow labor productivity, at least in principle.

In 1987, when Solow published his essay in the New York Times Book Review, the U.S. economy was mired in a so-called productivity slowdown, so called because the annual growth rate of labor productivity had fallen persistently. The slowdown began around 1973 and ended, for a time, around 1995. In his review, Solow famously quipped, “You can see the computer age everywhere but in the productivity statistics.” Or, put differently, the productivity statistics—the data—seemed unaffected by the proliferation of a computer technology that everyone expected would increase labor productivity.

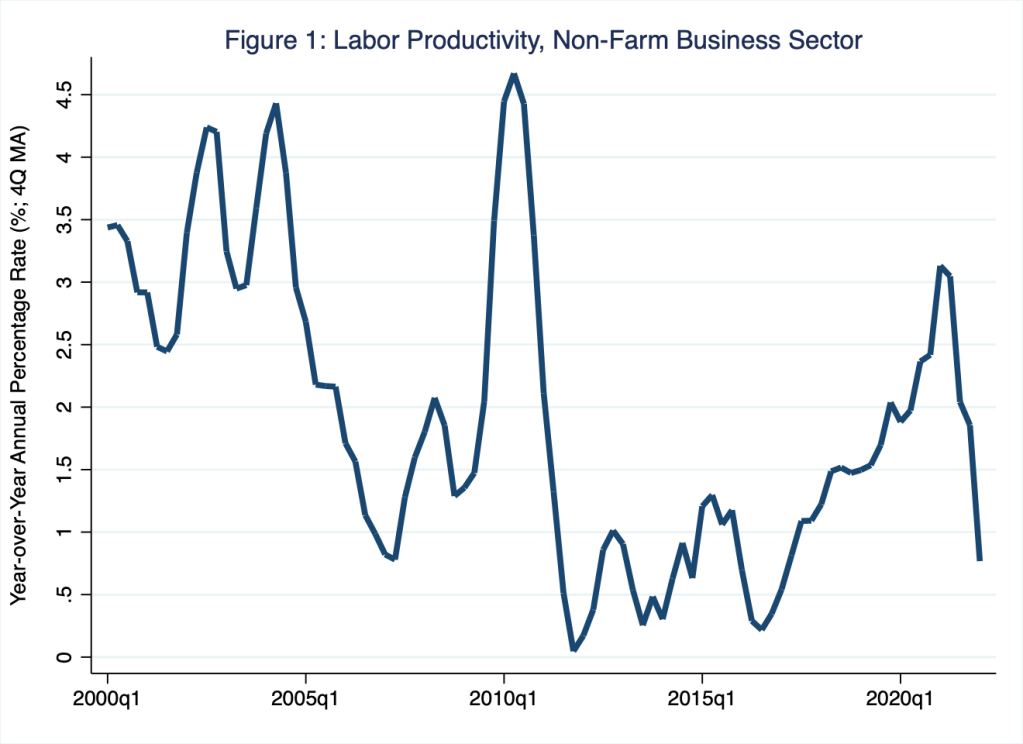

History may not repeat itself, but it tends to rhyme. For the last several years, and largely before COVID, it seems the U.S. economy has been once again mired in a labor-productivity slowdown of sorts, at least based on how we empirically measure labor productivity, a devilishly difficult economic statistic to measure. And COVID seems not to have made a difference, at least not yet. This is to say, for all the talk of how labor shortages and supply-chain crises inspired labor-saving and, thus, labor-productivity-augmenting innovations, recently the growth of labor productivity seems to be falling instead of rising. This pattern is visible in Figure 1, in which I illustrate the year-over-year annual rate of growth of labor productivity. (For more on the effects of automation, COVID-inspired and otherwise, on labor markets see Monday Macro segment “Yoshimi’s Lament“.)

According to Figure 1, the annual rate of growth of labor productivity fell around, though not necessarily because of, the financial crisis in 2008. The spike around 2010 had mostly to do with arithmetic: high unemployment tends to temporarily raise output per (employed) labor input. The rate remained relatively low for several years thereafter, increasing only in the lead up to the COVID pandemic. Since then, the rate has declined—whether persistently or otherwise is too soon to know. It’s as if you can see a technological new age—of artificial intelligence, robotics, autonomous vehicles, civilian space exploration, and so on—everywhere but in the productivity data! Sound familiar?

Who cares?

Macroeconomists care, and so too should everyone else, if only they could stop talking about inflation; in the long run, labor-productivity growth is as important as price stability. This is because, as it turns out, labor productivity is a principal source of economic growth, which we measure as the average annual growth rate of output (or income) per person over several decades. You could think of economic growth as the growth in the average standard of living in the long run. And, as Monday Macro devotees know well, the consequences of economic growth are profound. For example, an economy that sustains an economic growth rate of 1 percent annually would double output per person about every 70 years; whereas an economy that sustains an economic growth rate of 2 percent annually would double output per person about every 35 years. Because most individuals would prefer, all else equal, to live in an economy in which the average standard of living doubles, say, twice in a lifetime instead of once in a lifetime, understanding the principal sources of economic growth is very important. And, as I demonstrate next, over time the annual rate of economic growth is roughly equal to the annual rate of labor-productivity growth. As Nobel laureate Paul Krugman once quipped, “Productivity isn’t everything, but, in the long run, it is almost everything.”

To see this tight connection between economic growth and labor productivity, consider a very useful economic-growth decomposition—a Monday-Macro favorite. By definition, economic growth is a dynamic process, because changes in output per person occur over time. At a moment in time, output per person (γ) is the product of labor productivity, labor hours per employee, the employment rate, and the labor-force participation rate, as follows.

γ = ρ × η × ε × λ

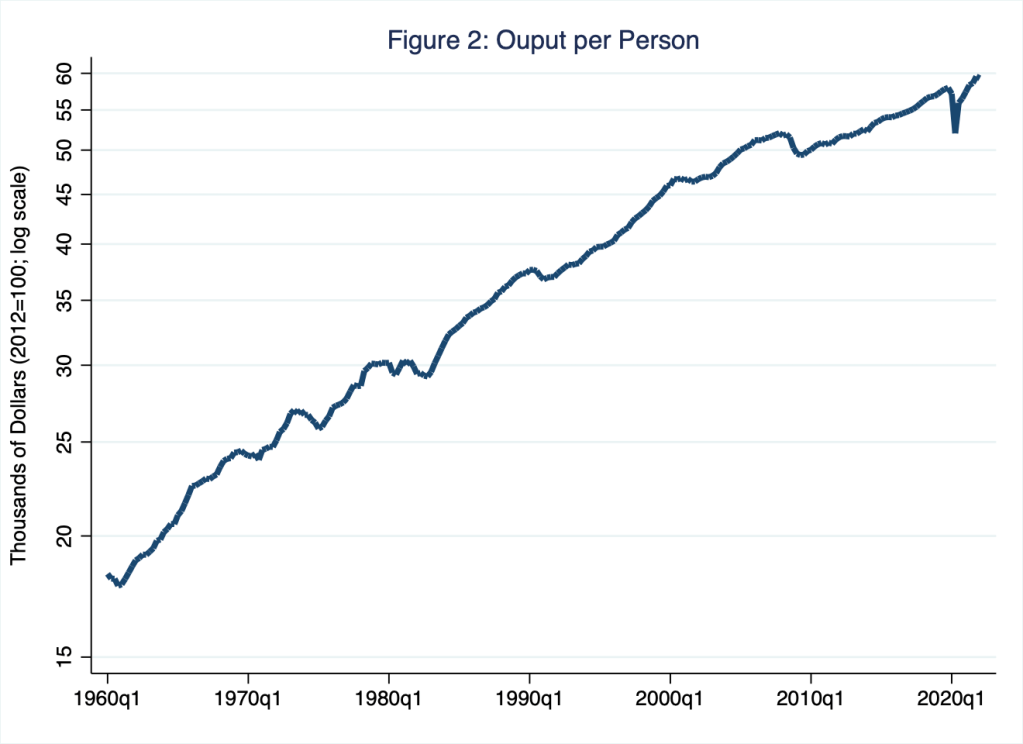

Where ρ is labor productivity (output per labor-input hour), η is labor hours per employee, ε is the employment rate (employees per labor force), and λ is the labor-force participation rate (labor force per population). This decomposition must be true based on how we define γ, ρ, η, ε, and λ. By definition, then, output per person (γ) must equal the product of the four terms on the right-hand side of the expression. In Figure 2, I illustrate output per person, which I measure as real GDP per person, since 1960. In terms of the expression above, Figure 2 illustrates a measure of the natural logarithm of γ; thus, changes in this measure—revealed by the slope of a line tangent to any given point along the plot illustrated in Figure 2—represent rates of economic growth: relatively steep [flat] slopes represent relatively high [low] rates of economic growth.

According to Figure 2, output per person in, say, the first quarter of 2022, was $59,297 in year-2012 dollars. Perhaps more importantly, from 1960 to 2021, output per person grew on average at an annual rate of about 2 percent; at this rate, the average standard of living in the United States—measured, in this case, by output per person—doubles every 35 years. A simple, visual inspection of Figure 2 reveals that output per person includes a cyclical component that varies irregularly around a long-run trend; thus, output per person occasionally exhibits growth effects—persistent changes in the rate of growth (around trend growth of about 2.0 percent annually in this case). During the six decades captured in Figure 2, annual growth in output per person varied, at times substantially. For example, in the decade since the Great Recession that began in 2008, output per person in the United States grew at an average annual rate of about 1 percent; at this rate, the average standard of living doubles every 70 years.

If, according to the expression above, output per person (γ) is the product of labor productivity (ρ), labor hours per employee (η), the employment rate (ε), and the labor-force participation rate (λ), then arithmetic—not macroeconomics—tells us that the growth rate of output per person—our measure of economic growth—is, to a very close approximation, the sum of the growth rates of these terms, as follows.

growth rate of γ = growth rate of ρ + growth rate of η + growth rate of ε + growth rate of λ

So, the principal sources of economic growth—notationally, the growth rate of γ on the left-hand side of the expression—are the growth rates of labor productivity (ρ), labor hours per employee (η), the employment rate (ε), and the labor-force participation rate (λ) on the right-hand side of the expression. In Table 1, I report the average annual growth rates of γ, ρ, ε, and λ for various sample periods. (In the table, I do not report the annual growth rate of labor hours per employee [η] because it varies relatively little; for example, for the last forty years, η has measured about 1800 hours, or about 52 weeks times about 35 hours per week.)

Table 1: Average Annual Growth in Output per Person (γ) and Its Principal Sources

| γ | ρ | ε | λ | |

| 1960 – 2021 | 1.9 | 2.0 | 0.0 | 0.1 |

| 1960 – 1972 | 2.8 | 2.8 | 0.0 | 0.1 |

| 1973 – 1995 | 1.9 | 1.5 | 0.0 | 0.4 |

| 1996 – 2007 | 2.2 | 2.7 | 0.1 | (0.1) |

| 2008 – 2021 | 0.9 | 1.5 | 0.0 | (0.5) |

Across each row in Table 1, the average annual growth rate of output per person (γ) equals, to a close approximation, the sum of the average annual growth rates of labor productivity (ρ), the employment rate (ε), and the labor-force participation rate (λ). For example, consider the row associated with the sample period 2008 to 2021: the average annual growth rate of output per person (γ) is a relatively abysmal 0.9 percent, which equals to a close approximation the average annual growth rate of labor productivity (ρ; 1.5 percent) plus the average annual growth rate of the employment rate (ε; 0.0 percent) plus the average annual growth rate of the labor-force participation rate (λ; – 0.5 percent). To be sure, because of how we empirically define and measure these terms, this additive relationship is not perfect—consider, for example, the row associated with the sample period 1996 to 2007. Nevertheless, from the perspective of a macroeconomist, the rows in Table 1 exemplify the closest thing we have to precision!

Notice how closely the average annual growth rate of output per person (γ) and the average annual growth rate of labor productivity (ρ)—columns two and three in Table 1—align over time. For example, for the entire sample period of 1960 to 2021, each of these measures registers roughly 2.0 percent. This alignment generally occurs because, in the long run, labor-market forces reflected in, say, the rates of job search and separation determine the (natural) employment rate (ε), while demographic forces largely determine the labor-force participation rate (λ). Because labor-market and demographic forces change relatively slowly over time, these forces do not explain much of economic growth. Rather, labor-productivity growth explains nearly all economic growth.

According to Table 1, the sample period 1960 to 1972 was a high-water mark for economic growth and, thus, labor productivity; output per capita (γ) and labor productivity (ρ) each grew on average 2.8 percent annually. In contrast, the sample period 1973 to 1995, during which Solow quipped about the mystery of weak productivity growth in the “computer age,” was a low-water mark; during that period, output per capita (γ) and labor productivity (ρ) grew on average 1.9 percent and 1.5 percent annually (while the labor-force participation rate grew on average 0.4 percent annually, so that 1.9 percent equalled 1.5 percent plus 0.4 percent).

Interestingly, the sample period 2008 to 2021 appears to be another low-water mark for output per person (γ) and labor productivity (ρ). Over this sample period, the alarmingly low average annual economic growth rate of 0.9 percent is explained by an alarmingly low average annual productivity-growth rate of 1.5 percent—the same rate the economy registered during the infamous productivity slowdown to which Solow referred in 1987—compounded by a fall of 0.5 percent in the labor-force participation rate due, in part, to COVID. Of course, the U.S. economy might turn this labor-productivity trend around, though some evidence suggests post-pandemic productivity growth tends to underperform. Optimism at this point derives to a large extent from the so-called productivity J-curve: initially, adopting new technologies shifts resources toward intangible investments—think, new recipes—more than it raises output, causing productivity growth to decline; optimists reason that this downward-sloping segment of the productivity J-curve describes our current situation. These intangible investments pay off with a lag, causing output to rise later, without a simultaneous increase in labor or capital inputs; the net effect is a rise in productivity growth reflected by the upward-sloping segment of the productivity J-curve. Put differently, perhaps the abysmally weak productivity growth we have experienced more or less since around the time of the Great Recession is transitory; where have I heard that term before?