This blog post accompanies the SDPB Monday Macro segment that airs on Monday, February 7, 2022. Click here to listen to the segment.

Automation, an outcome of the technological growth to which macroeconomists attribute the sustained rise in living standards in the U.S. and elsewhere for the last few hundred years or so, is not new. And neither is the fear that robots—sometimes portrayed as evil anthropomorphic embodiments of automation—are coming for our jobs. Thanks to the pandemic, and its concomitant shock to labor markets, how automation affects employment and the welfare of workers more generally are questions everyone seems now to ask. To the blissful satisfaction of Flaming Lips fans everywhere, Yoshimi battles the pink robots; but have they come to take her job? Maybe, but some labor-market participants may wish the robots dead in any case. Read on.

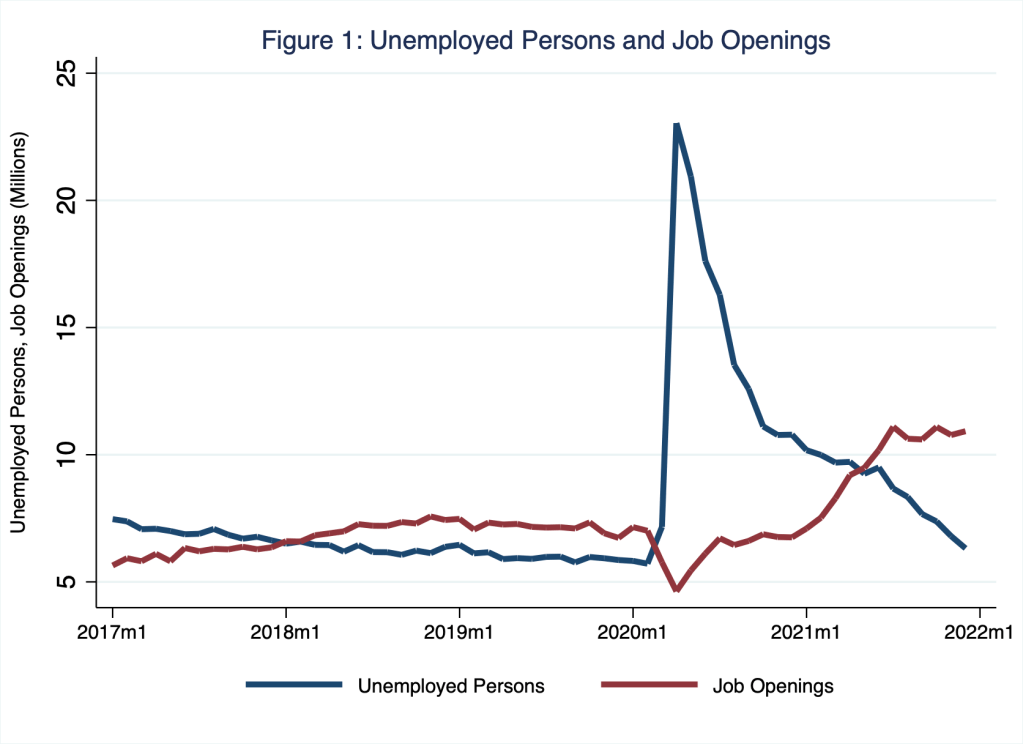

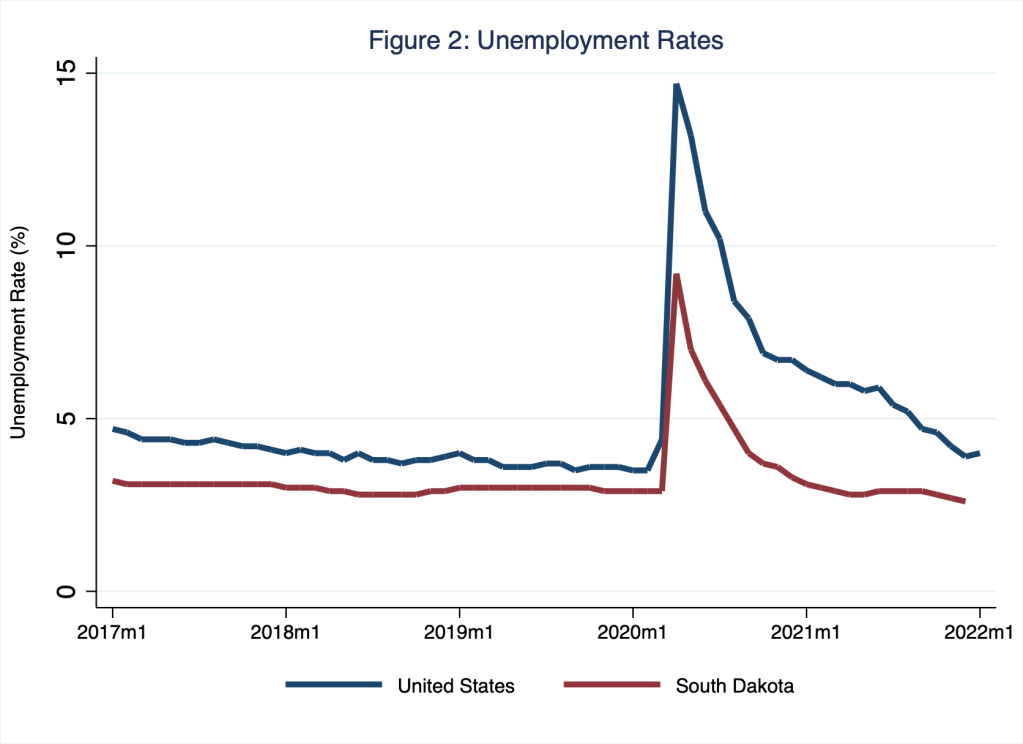

To be sure, since long before the pandemic, economists have studied the effects of automation on labor markets. Ironically, we would be forgiven for thinking the pandemic initially quelled rather than stirred interest in this topic; lockdowns and repressed demand for goods and services rendered labor plentiful: no need for robots when labor is desperately seeking work. As I illustrate in Figure 1, in the early months of the pandemic in the U.S., the number of unemployed persons rose dramatically by roughly 20 million, while the number of job openings fell. Consequently, as I illustrate in Figure 2, the unemployment rate rose dramatically in the nation and in South Dakota—home to Schooled and Monday Macro.

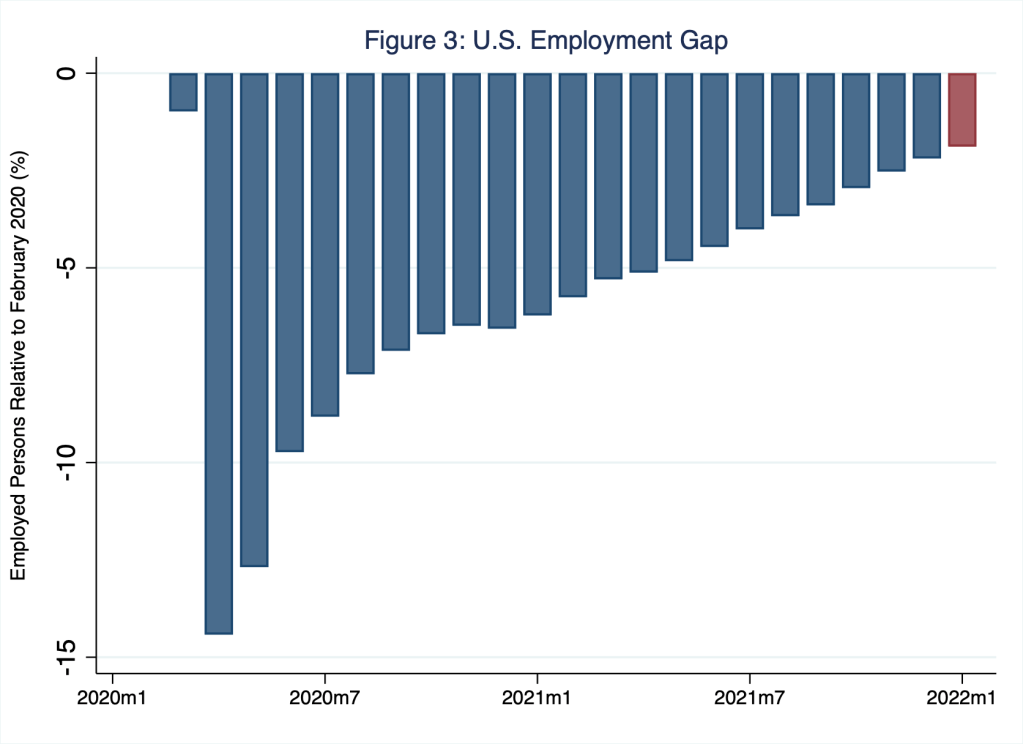

Thus, the pandemic initially idled a relatively large share of the labor force, leaving a plentiful (excess) supply of human resources that might have discouraged firms from investing in labor-saving automation had such conditions persisted. However, such conditions did not persist, of course. Rather, as I also illustrate in Figures 1 and 2, U.S. labor markets tightened relatively quickly. By early 2021, conditions of excess supply turned to conditions of excess demand: the number of unemployed persons fell below the number of job openings (Figure 1), while the unemployment rate soon satisfied any reasonable macroeconomic definition of full employment (Figure 2). As of January 2022, jobs outnumbered available workers and the labor force was effectively fully employed, even though the number of persons employed in the U.S. remained below the number of persons employed in February 2020, around the time the pandemic was officially detected in the U.S. In Figure 3, I illustrate this pattern: as of January 2022, the employment gap, relative to the number of persons employed in February 2020, remained at negative 1.9 percent, or roughly 2.9 million (missing) persons.

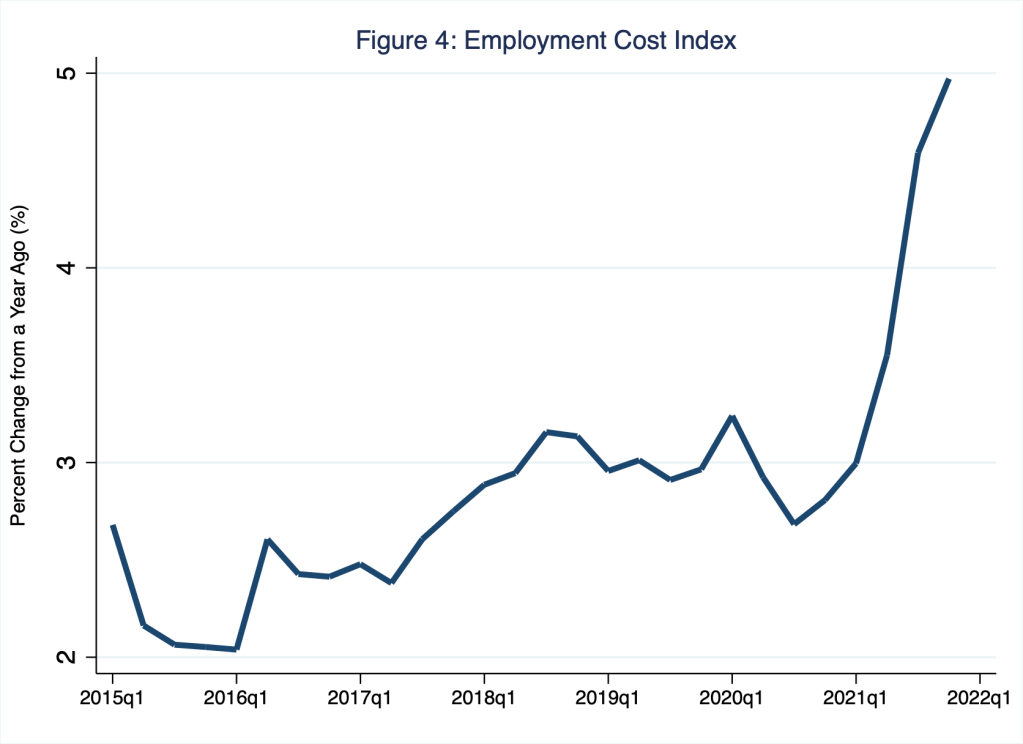

One implication of a tight labor market is clear: wages rise, because to fill a labor shortage, employers bid the wage—the price of labor services—higher. Recently, this pattern of growing nominal wages amid tight labor markets is unambiguous and somewhat dramatic. As I illustrate in Figure 4, according to the employment-cost index (for wages and salaries of private-industry workers), in the fourth quarter of 2021, year-over-year growth of employment costs—think, equilibrium nominal wages—rose by 5 percent, the largest annual growth rate in this measure since its inception in 2002.

In principle, bidding wars that effectively raise wages return the labor market to equilibrium for two reasons. (For more on the effects of labor demand and labor supply on wages during the pandemic, see Monday Macro segment “Wagering on Recovery.”) One reason is that, as wages rise, the quantity of labor supplied rises, because as the price of labor services rises, newly employed persons join the labor market; higher wages draw persons into employment whether from within or from outside the labor force. Perhaps this tendency explains, in part, why the employment gap (Figure 3) has shrunk consistently since the start of the pandemic. A second reason, and more importantly for the purposes of this blog post, is that the quantity of labor demanded falls, because as the price of labor services rises, some employers can no longer justify hiring more labor. Thus, some would-be employers of labor automate instead. For example, early on in the pandemic, Chernoff and Warman (2020) identified jobs held by women with mid-to-low wages and levels of education as those most likely automated by employers responding specifically to the pandemic.

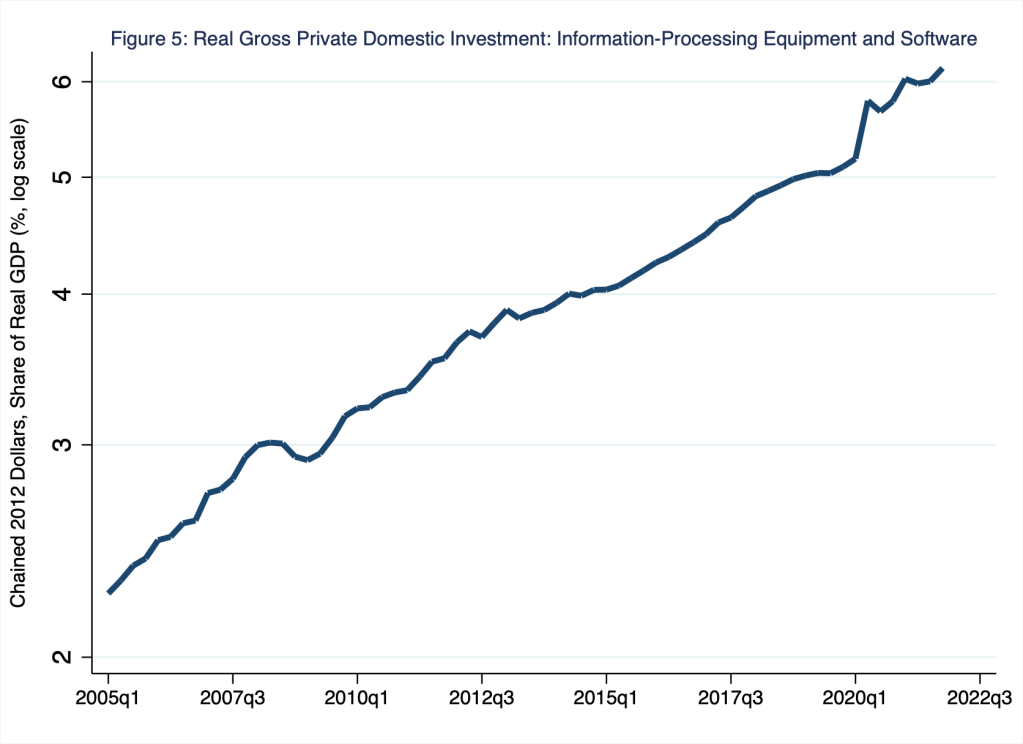

Though it is too early to tell how specifically investment in automation—labor saving or otherwise—has accelerated since the pandemic, evidence that such investment has surged in the aggregate seems apparent. As I illustrate in Figure 5, the share of real U.S. gross domestic product comprised of real investment in information-processing equipment and software—a loose proxy for investment in the technologies related to automation, say—rose discontinuously during the pandemic (even if we account for the fall in GDP in the first half of 2020, which I do indirectly in Figure 5 by dividing real investment by real GDP).

To be sure, while the pandemic may have spurred investments in automation, the trend toward automation—and investment expenditures in technology more broadly—would have persisted in any case: the pandemic simply emphasized an ongoing trend in the U.S. economy and elsewhere, where the defining feature of long-term economic growth remains technological innovation and, along with it, labor-market churn: shifts in the demand for labor and corresponding changes in the composition of jobs. For example, the World Economic Forum estimates in its Future of Jobs Report 2020 that in just the next few years the demand for jobs in data analysis, artificial intelligence (AI), and process automation will substantially increase (Table 1), while the demand for jobs in data entry, manufacturing assembly, and machine repair will substantially decrease (Table 2).

Table 1: Top 10 Jobs — Increasing Demand across Industries

| Rank | Job Title |

| 1 | Data Analysts and Scientists |

| 2 | AI and Machine Learning Specialists |

| 3 | Big Data Specialists |

| 4 | Digital Marketing and Strategy Specialists |

| 5 | Process Automation Specialists |

| 6 | Business Development Professionals |

| 7 | Digital Transformation Specialists |

| 8 | Information Security Analysts |

| 9 | Software and Applications Developers |

| 10 | Internet of Things Specialists |

Table 2: Top 10 Jobs — Decreasing Demand across Industries

| Rank | Job Title |

| 1 | Data Entry Clerk |

| 2 | Administrative and Executive Secretaries |

| 3 | Accounting, Bookkeeping and Payroll Clerks |

| 4 | Accountants and Auditors |

| 5 | Assembly and Factory Workers |

| 6 | Business Services and Administration Managers |

| 7 | Client Information and Customer Service Workers |

| 8 | General and Operations Managers |

| 9 | Mechanics and Machinery Repairers |

| 10 | Material-Recording and Stock-Keeping Clerks |

In effect, jobs of the sort listed in Table 1 will replace—and, in part, work to innovate the technologies necessary to replace—jobs of the sort listed in Table 2.

Cue up the automation-kills-jobs narrative—justifiably or otherwise.

The effects of technological innovations on the labor market are complicated. Nevertheless, some patterns are rather clear, and supported by rigorously reasoned microeconomic theory. Importantly, technological innovations augment and, thus, raise labor productivity—think, output per labor hour of input. And, as it turns out, labor productivity is a principal driver of economic growth—think, output (or GDP) per capita. All else equal (specifically, average labor hours worked per employee, the employment rate, and the labor-force participation rate), economic growth equals labor-productivity growth. Thus, in the long run, if we increase labor-productivity growth, we increase economic growth. And, generally speaking, the way we increase labor-productivity growth is to increase the growth of technological innovation and, to a lesser extent, the growth of capital formation, both effectively equip labor, making it more productive than otherwise. And, of course, in the long run, labor-productivity growth uniquely drives real-wage growth. (For more on the relationship between labor productivity and economic growth—and why the Soviet Union did not bury the U.S., see Monday Macro segment “(Iron) Curtain Call.”)

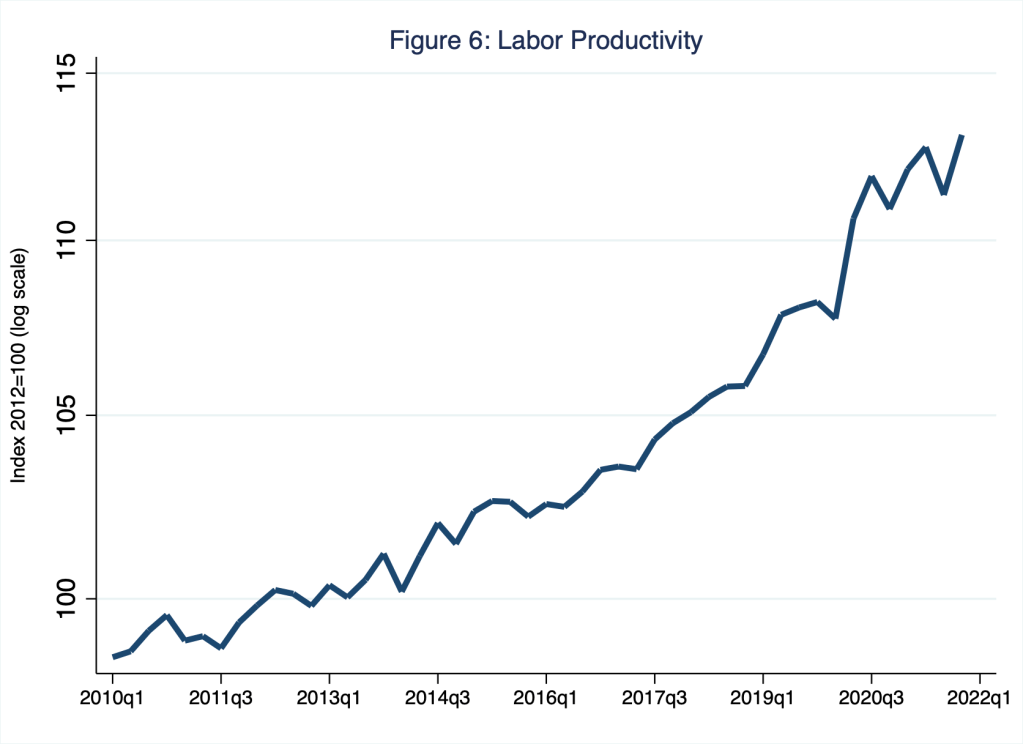

A corollary of this analysis is that even if technological innovation were to destroy jobs on net—and it very likely does not—such innovation would nevertheless necessarily increase labor productivity. This general pattern is apparent in Figure 6, in which I illustrate labor productivity (as an index normed in 2012) during the pandemic, when labor’s share of capital and technology effectively rose and, with it, labor productivity effectively rose as well.

In the prior paragraph, I write effectively rose because, in this perverse pandemic-induced instance, illnesses and lockdowns, as opposed to, say, labor-saving automation, reduced the number of employed persons relative to the levels of capital and technology. Nevertheless, the pattern I illustrate in Figure 6 is instructive: the arithmetic that drove labor productivity higher around the pandemic is the same arithmetic that would drive labor productivity higher if technological innovation destroys jobs on net—and, again, it very likely does not. Put simply and perhaps a bit crudely, those who work alongside labor-saving technology are generally advantaged with higher labor productivity and higher real wages. Meanwhile, of course, those who do not work alongside labor-saving technology, but are instead replaced by labor-saving technology, are unambiguously disadvantaged in the short run, when neither time nor opportunity allows them to retrain and, thus, invest in their human capital (so they could work alongside otherwise-labor-saving technology). Incidentally, affording those displaced by labor-saving technology the time and opportunities to invest in their human capital and regain meaningful, remunerative employment are roles public policies could play.

Maybe, just maybe, automation creates jobs.

And then there is the intriguing possibility that automation creates jobs on net. As the Economist recently observed, “Two years on [from the start of the pandemic], …the evidence for automation-induced unemployment is scant, even as global investment spending is surging.” In a recent, unpublished paper out of the Department of Economics at Harvard University, Aghion, Antonin, Bunel, and Jaravel (2021) identify, based on the authors’ review of the recent literature, two views of how automation affects employment. According to the first view, the direct effect of automation is to eliminate firms’ demands for some workers; the indirect effect is to increase firms’ quantities demanded of other workers for which the equilibrium wage has fallen amid a glut of willing (and otherwise-idle) labor. No, labor does not fare well according to the first view. Meanwhile, according to the second view, the direct effect of automation is to increase firms’ productivity, competitive (pricing) advantage, and scale of production, thus increasing firms’ demand for workers, who may draw from the firms’ automation-deprived competitors—what the authors identify as an indirect “business-stealing” effect. Yes, labor fares better according to the second view. Moreover, based on firm-level data for France, the authors empirically test for evidence of each view and find support for the second view: “automation has a positive direct effect on employment at the firm level” (p. 1).

Importantly, though, neither the theory nor the empirical evidence on the subject seems to say very much about the nature of the jobs created and, thus, the extent to which those jobs rightly reward, fulfill, or otherwise satisfy labor. And in any case, it seems likely that technological innovation most advantages the highest-skilled workers, those employed in, say, non-routine, cognitive occupations (which typically pay well because technologically enhanced labor productivity is relatively high) as opposed to those employed in, say, routine, manual occupations (which typically pay poorly because technologically enhanced labor productivity is relatively low). Thus, in addition to reducing the quality of life for some workers for some time, automation could fuel income inequality. This pattern aligns with the findings of Sedik and Yoo (2021), who conclude in a recent IMF working paper that pandemic events fuel robot adoption and labor productivity, while also fueling labor inequality.

Flaming Lips fans have long debated why Yoshimi battles the pink robots; a growing body of economic research suggests the reason may not be that the robots are job killers; though, in some cases, the robots may be dream killers who fuel income inequality.

References

Aghion, Philippe, Céline Antonin, Simon Bunel, and Xavier Jaravel. 2021. “The Direct and Indirect Effects of Automation on Employment: A Survey of the Recent Literature.” Department of Economics, Harvard University, unpublished manuscript: 1-24.

Chernoff Alex W. and Casey Warman. 2020. “COVID-19 and Implications for Automation.” NBER Working Paper Series, Working Paper No. w27249: 1-28.

Sedik, Tahsin Saadi and Jiae Yoo. 2021. “Pandemics and Automation: Will the Lost Jobs Come Back?” IMF Working Paper, Working Paper No. 2021/011106: 1-26.

One thought on “yoshimi’s lament”