This blog post accompanies the SDPB Monday Macro segment that aired Monday, June 7, 2021. Click here to listen to the segment, which begins at minute 26:30 into the broadcast.)

This weekend, more than 10,000 people met—up close and in person—in Miami for Bitcoin 2021, the largest conference of its kind. According to the New York Times, “the [conference] was another sign that the often absurd world of digital currencies was inching its way toward mainstream acceptance, or at least mainstream curiosity.” Meanwhile, the market value of bitcoins in circulation has swung wildly. In the last sixty days, the value of a bitcoin has fallen from roughly $64,000 (set April 13, 2021) to roughly $36,000 (now)—a fall of roughly 44 percent. Perhaps not surprisingly, this weekend’s conference attendees saw this fall as an opportunity to buy the dip.

In any case, is Bitcoin money?

Economists define money, in principle, as anything that everyone generally accepts as a means of payment—including the payment of debt. Or, somewhat less formally, money is what money does; and here economists refer to the functions of money—a hierarchy of roles, which assets in general may or may not perform, that money performs by definition, namely: store of value, medium of exchange, and unit of account. An asset—again, money or otherwise—performs the store of value function if the asset’s value—think, purchasing power—relative to all other goods and services is stable over time. For example, the store-of-value function of money allows you to set aside $5 (today’s price of your favorite coffee drink, say) to buy your favorite coffee drink tomorrow. Thus, a monetary store of value allows you to smooth consumption optimally through time: it allows you to buy (and consume) your favorite coffee drink at a time of your choosing. (Why any of us pays $5 for a coffee drink is another matter entirely.)

An asset performs the medium-of-exchange function if at least two of us are willing to exchange the asset—and, thus, to believe the asset performs its store-of-value function—at some moment in time. Concretely, exchanging $5 for your favorite coffee drink requires you to reason the purchasing power of money will not soon rise dramatically (in which case you may not surrender the money now); and it requires the coffee vender to reason the purchasing power of money will not soon fall dramatically (in which case the vender may not accept the money now). Finally, an asset performs the unit-of-account function if we measure, in terms of the asset, the relative values of all goods and services over time. For example, the dollar performs the unit-of-account function if we measure the value of your favorite coffee drink in terms of dollars instead of gallons of unleaded gasoline or blueberries, for example.

In the United States, we currently identify money, in practice, as (sovereign) currency in circulation—think, Federal Reserve notes and coin; the latter is a liability of the United States Treasury, as opposed to the Federal Reserve—and (private) short-term intermediated and highly liquid checking- and savings-account deposits. Thus, in practice, money is M1, if we measure money narrowly, or M2, if we measure money broadly. (For more on empirical measures of the U.S. money stock, see Monday Macro segment, “Great (Inflation) Expectations.”)

Generally speaking, money takes one of two forms: namely, commodity or fiat. Commodity money has intrinsic value in terms of the relative value of the underlying commodity outside of its use as money; the commodity, gold, has a value in the marketplace independently of whether or not we use gold as (commodity) money, for example. In contrast, fiat money has no intrinsic value; rather it has value only because we agree it has value. Today, the U.S. dollar and most other currencies throughout the world are fiat monies.

Ultimately, of course, money is a social construct. Money is if we collectively believe it is.

So is Bitcoin money? Well, at the very least, Bitcoin is a crypto asset.

A brief somewhat-technical detour may be in order; if you disagree, skip to the next paragraph. Cryptography is, as Gary Gensler (current chair of the Securities and Exchange Commission and former chair of the Commodity Futures Trading Commission) defines it, communications in the presence of adversaries. A crypto asset, a term Mark Carney, former governor of the Banks of Canada and England favors, is the product of a peer-to-peer (decentralized) distributed ledger technology. The ledger digitally records and, importantly, validates (or proves) absent a third-party clearing intermediary—think, a bank—the authenticity of pseudonymous (as opposed to anonymous) transactions denominated in some crypto asset: in the case of Bitcoin, for example, so-called bitcoins and satoshis—1 bitcoin equals 100,000,000 satoshis. (The pseudonym for the creator of Bitcoin is Satoshi Nakamoto.) The transactions are aggregated over time into blocks, and the authenticity of each block is dependent on the authenticity of every other block; in this way, the sequence of bitcoin-denominated transactions form blockchains. Authenticating each block is the work of so-called miners, who earn newly minted crypto assets—bitcoins in this case—in return for their efforts, which amount to finding, via trial-and-error computerized iterations, solutions to mathematical puzzles. For the very-technical reader: the puzzle requires finding the random number—the nonce (or number used once)—that returns, in combination with other data that identify the block, hash-function output that begins with a specified number of zeros. This number of zeros determines the difficulty of the trial-and-error iterative-solution process and, thus, the difficulty, in terms of time spent searching, of earning newly minted bitcoins. The difficulty level is adjusted as necessary so as to require a ten-minute search on average.

In principle, exchanging a crypto asset for goods and services mimics, in the cryptographic sense, exchanging cash for goods and services. Imagine the digital equivalent of, “I pay a guy $150 bucks to fix my garage door.” In this case, two private parties or peers—me and a guy—record and verify absent a third-party clearing intermediary the authenticity of the exchange of $150 bucks; this is to say, a guy fixes my door and I hand that guy $150 bucks. Done. Turns out, this very simple transaction is devilishly difficult to replicate, absent a third-party clearing intermediary, reliably in cyberspace, where I might be able to pay a guy $150 and simultaneously pay another guy the same $150. The innovation of peer-to-peer decentralized ledger technology in the form of Bitcoin (and other such crypto assets) is the mining effort—and, thus, the authentication or proof-of-work consensus process—incentivized by payments of newly minted bitcoins.

Okay so, again, is Bitcoin money?

Let’s answer this question through the lens of the three functions of money. And let’s work backwards, beginning with the unit of account. Currently, the marketplace measures bitcoins and dollars relative to each other; that is, for the most part, the marketplace does not measure the value of goods and services directly in terms of bitcoins. To be fair (to Bitcoin), this shift in the convention we use to measure value would take some time, to say the least, for even the most worthy of potential monetary assets. Nevertheless, in the context of the unit-of-account function of money, Bitcoin is not money, at least not yet. Meanwhile, exchanging bitcoins (as a medium of monetary exchange for goods and services) remains in the fringes of the financial system. This need not be the case forever; but it is the case at the moment. Thus, in the context of the medium-of-exchange function of money, Bitcoin is not money, at least not yet. And so finally, what about the store of value function? Proponents of the Bitcoin-as-money proposition often claim that Bitcoin’s performance as a store of value is evidence bitcoins are—or soon could be—a form of money, embryonic or otherwise.

This claim is not without its irony. Read on.

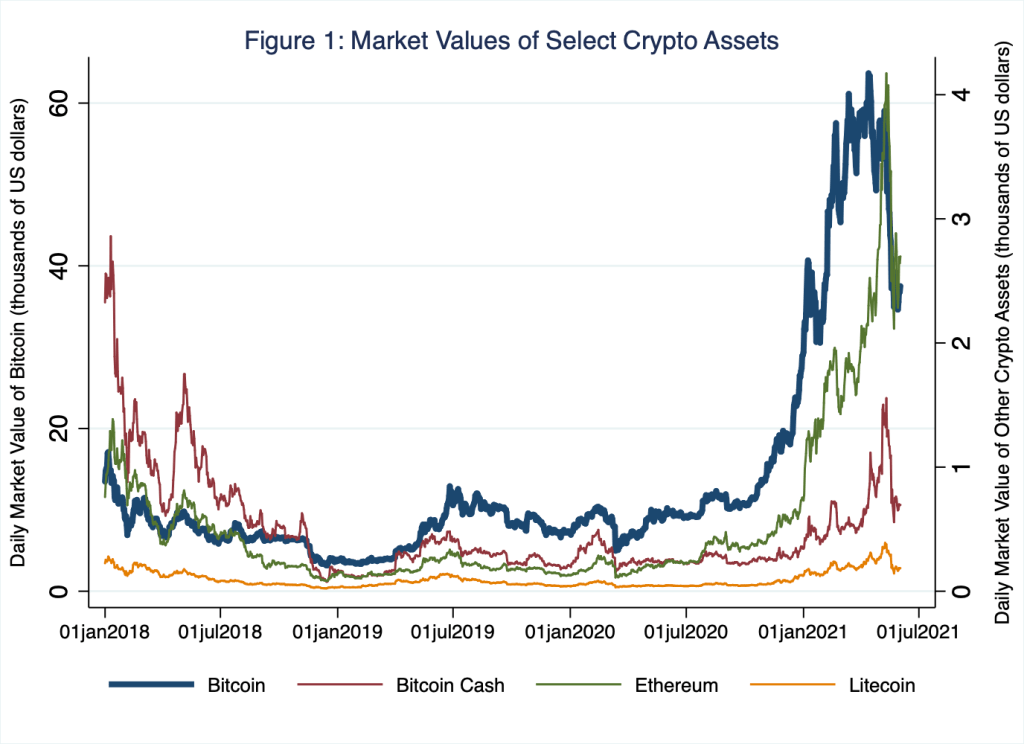

To be sure, crypto assets are having a moment. In Figure 1, I illustrate the daily market values of bitcoins and three other popular crypto-asset denominations in circulation; there are thousands of crypto-asset denominations in circulation.

Source: Federal Reserve of St. Louis (FRED) series CBBTCUSD, CBBCHUSD, CBETHUSD, CBLTCUSD.

According to Figure 1, the value of, say, a bitcoin in 2021 rose from roughly $29,000 on January 1 to roughly $64,000 on April 13, a rise of roughly 121 percent; its value has since fallen to roughly $36,000, a fall of roughly 44 percent (in about sixty days). The other crypto assets I illustrate in Figure 1 have been quite volatile as well. No doubt, bitcoins are valuable; but are they a suitable store of value in the monetary sense?

On the basis of Figure 1, at the moment, bitcoins poorly function as a store of value. The crypto asset’s value—think, purchasing power—relative to all other goods and services has not been stable over time. Based on Figure 1, would you and your favorite coffee-drink vender exchange some amount of bitcoins for your favorite coffee drink? Maybe; but I could image the volatility of the crypto asset’s market value compromising its exchangeability in general. And this volatility is the least of Bitcoin’s store-of-value challenges. The greatest store-of-value challenge to Bitcoin as money is Bitcoin monetary policy.

Cue the quantity theory of money—again, I know; it’s a recurring feature of Schooled.

Imagine an economy in which Bitcoin is indeed money. As Schooled readers know well, a useful way to think about the relationship between the quantity of money—think the quantity of bitcoins—and money’s purchasing power is the so-called income version of the quantity equation (or, quantity equation, for short), which we specify in the following way.

M × V = P × Y

As usual, M represents the quantity of money—again, think, quantity of bitcoins; P represents the overall price level—think, the price level in terms of bitcoins; Y represents real income, which economists empirically measure with real GDP; and V represents the income velocity of money, which economists define as the average number of times the quantity of money (M) is exchanged for nominal GDP (P×Y). For example, suppose the quantity of bitcoins in the economy is BTC 15 (M = BTC 15); and, suppose during one year 30 pencils are produced, purchased, and valued at a price of BTC 1 each (P × Y = BTC 30). In this example, the income velocity of money equals 2: BTC 15 of money facilitates BTC 30 of nominal GDP per year, because each bitcoin changes hands, on average, 2 times per year in order to purchase BTC 30 of nominal GDP.

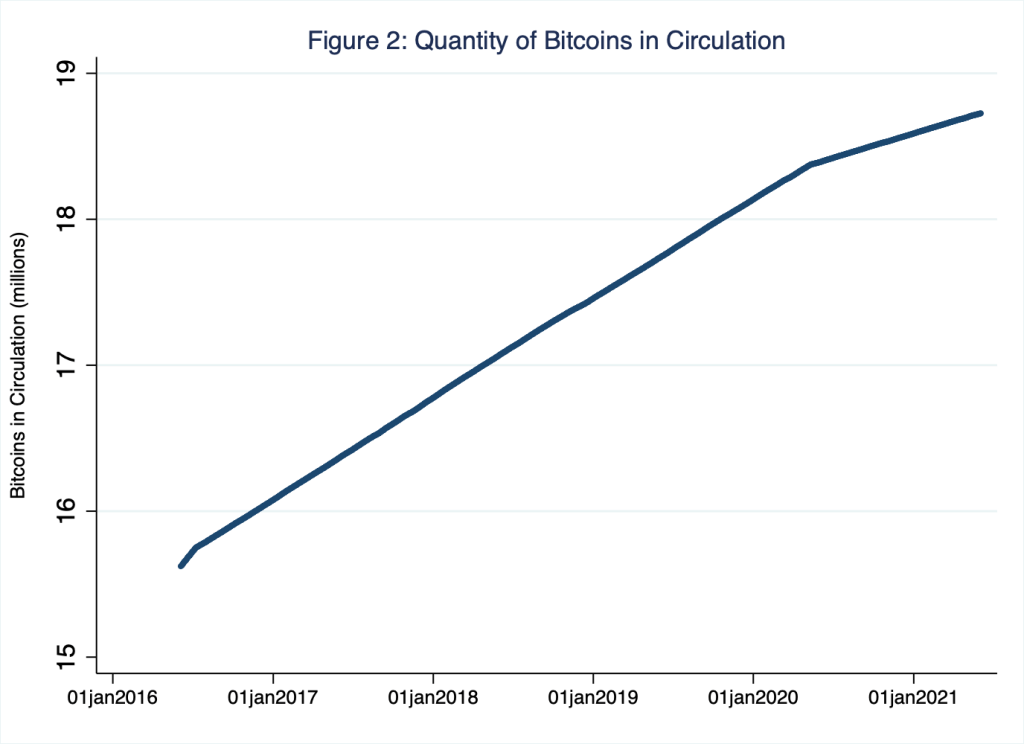

Let’s assume for simplicity that individuals hold amounts of money in roughly fixed proportion to their nominal income, so that the velocity of money (V in the quantity equation above) is roughly constant over time. In this case, then, the quantity equation implies the growth of the money supply (M) equals the growth of nominal GDP (P × Y). And because over the long run the growth of real economic activity (Y) is independent of the rate of inflation (the growth of P), let’s assume real economic activity grows at some constant rate, say 0 for arithmetic simplicity. Thus, if we assume the velocity of (Bitcoin) money is constant and real economic activity (Y) is constant, the growth of M determines—and, in this specific thought experiment, is equal to—the growth of P: the growth of the quantity of bitcoins in circulation determines the rate of inflation in terms of bitcoins. In Figure 2, I illustrate the path of the quantity of bitcoins in circulation over time.

Source: Satoshi.info.

The smooth path in Figure 2 is not some statistical approximation; it’s the actual path of the quantity of bitcoins in circulation. In Figure 2, this path includes three (diminishing) growth rates—think, slopes in Figure 2—punctuated by two discrete changes in growth rates—think, kinks between the slopes in Figure 2. This deterministic pattern is the result of the mining process and protocols I described in the technical detour above: within the Bitcoin structure—its monetary policy, if you will—the difficulty of earning newly minted bitcoins changes over time so that earning a set amount of newly minted bitcoins—a set amount that halves every 210,000 authenticated blocks—requires a ten-minute search on average. For any fixed-slope segment in Figure 2, the amount of bitcoins earned (the rise of the slope) and the amount of time required to earn those bitcoins (the run of the slope) are fixed. Moreover, Bitcoin monetary policy dictates that the quantity of bitcoins in circulation is capped at 21 million (at which point the blue line in Figure 2 would appear perfectly flat).

Thus, Bitcoin monetary policy requires the growth of the (Bitcoin) money supply to shrink to zero. According to the quantity equation and our working assumptions that velocity and economic activity are fixed, this means Bitcoin monetary policy implies the rate of inflation must approach zero. And, if, instead, economic activity grows over time, which it most likely will as it has for centuries, then Bitcoin monetary policy implies the rate of inflation must become negative—deflation rarely works well in practice (though there are potentially strong cases for why a certain level of deflation could work in principle). Put differently, Bitcoin monetary policy is designed to violate the store of value function by allowing the purchasing power of bitcoin to rise over time, assuming economic activity grows over time.

Finally, and quite importantly, the deterministic evolution of bitcoins in circulation (see Figure 2) implies no role for activist monetary policy in any case. Thus, in addition to Bitcoin failing to perform the basic functions of money, Bitcoin monetary policy prohibits discretionary changes—think, one-off increases or decreases—in the money supply of the sort the world witnessed in the aftermaths of the COVID pandemic and the Great Recession, for example. Broadly speaking, then, Bitcoin monetary policy leaves no role for a central monetary authority, such as the Federal Reserve, to play. But then again, perhaps that’s the whole point.

One thought on “tales from the crypt”