This blog post accompanies the SDPB Monday Macro segment that airs Monday, May 17. Click here to listen to the segment, which begins at minute 23:30 into the broadcast.)

On May 12th, the nonpartisan United States Bureau of Labor Statistics (BLS) released its measure of the consumer price index (CPI) for April 2021. According to the release, the CPI rose year-over-year—from April 2020 to April 2021—by 4.2 percent, the largest year-over-year increase since September 2008, when this measure recorded a 4.9 percent increase. The CPI is a widely popular measure of the average price level of goods and services purchased by typical U.S. households. And, so, the year-over-year change in the CPI—the 4.2 percent the BLS reported for April 2021—is a widely popular measure of the rate of inflation, the rate at which the purchasing power of money falls. Immediately after the BLS released its report, financial markets found reason to panic; the rate of inflation has been a topic of conversation among economists and, it seems, everyone else ever since. In Figure 1, I illustrate the year-over-year CPI-derived rate of inflation; the last data point in the far right of the figure is the 4.2 percent the BLS reported last Wednesday.

According to Figure 1, a 4.2 percent year-over-year rate of inflation is relatively high, though not unprecedentedly so. To be sure, market observers and policymakers alike expected a relatively high year-over-year increase in the average price level, if only because the average price level in April 2020 was extraordinarily low, thanks to the COVID-related lockdown. Nevertheless, most estimates of this so-called base effect—the difference between an extraordinary year-over-year inflation rate and the long-run (pre-pandemic) average inflation rate—fall in the neighborhood of roughly 1 percent. The additional rate of inflation of roughly 3.2 percent (4.2 percent minus the roughly 1 percent base effect) was higher than most anyone expected.

Still, given the COVID-related lockdown last spring, the sources of this relatively high rate of inflation for April 2021 are not surprising or, it would seem, likely to persist for more than a few months. In Table 1, I report, for select items in the CPI basket, the year-over-year percentage change in the average price level of those items (column 2) and their contribution to the 4.2 percent CPI inflation rate the BLS reported for April 2021 (in column 3); I rank these items in order of their respective contributions (column 3).

Table 1: CPI Select Items, April 2021 (Source: Bureau of Labor Statistics)

| Select Items | Year-over-Year Percentage Change | Contribution to 4.2% |

| Gasoline (all types) | 49.6% | 1.2% |

| Rent of Shelter | 2.1% | 0.7% |

| Used Cars and Trucks | 21.0% | 0.5% |

| Transportation Services | 5.6% | 0.3% |

| Food Away from Home | 3.8% | 0.2% |

| Medical-Care Services | 2.2% | 0.2% |

| Edu. and Comm. Services | 2.0% | 0.1% |

| Food at Home | 1.2% | 0.1% |

| New Vehicles | 2.0% | 0.1% |

| Furniture and Bedding | 7.8% | 0.1% |

| Recreational Vehicles | 1.8% | 0.1% |

| Other Personal Services | 3.0% | 0.1% |

| Total of Select Items | 3.7% | |

| Total of All Items | 4.2% |

Take, for example, Used Cars and Trucks. The year-over-year percentage change in the average price level of these items registered 21.0 percent (column 2)—and, yes, that’s a lot. Given the share (not reported in Table 1) of household expenditures directed to used cars and trucks in April 2021, the year-over-year percentage change in the average price level of these items contributed 0.5 percentage points (column 3) to the 4.2 percent CPI inflation rate that the BLS reported for April 2021. The list of twelve categories of select items in Table 1 is not exhaustive, of course. Nevertheless, together, these items contributed 3.7 percentage points of the 4.2 percent CPI inflation rate. In the next few months, as COVID-related disruptions to supply chains and labor markets fade and the CPI rises to reflect one-time effects of resuming normal economic activity, the rate of inflation should return to something closer to normal—say, about 2 percent. Right?

Enter the inflation hawks—for whom the recent spike of inflation is not temporary.

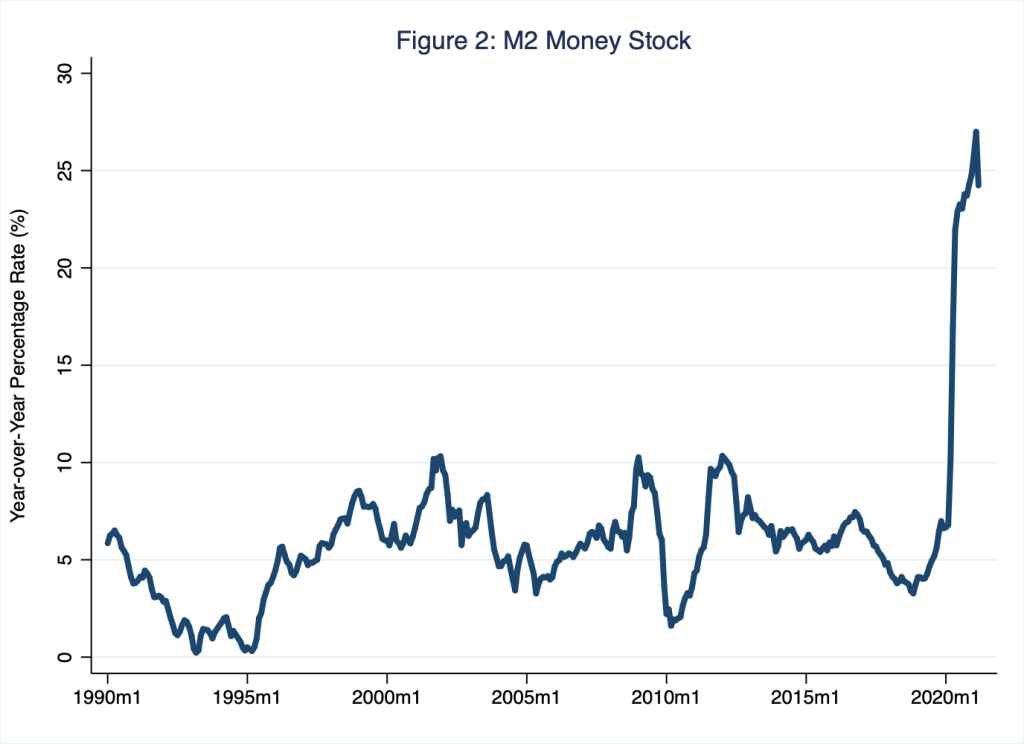

For most us, the rate of inflation—the rate at which the purchasing power of money falls—brings to mind the money supply. After all, the value of money must be related in some way to its supply. In Figure 2, I illustrate the year-over-year growth of the M2 money stock, the sum of currency and checking- and savings-account deposits.

Essentially, the M2 money stock comprises the dollar-denominated sum of all generally accepted financial assets that you or I could easily use to pay for a cup of coffee, for example. According to Figure 2, the M2 money stock has recently grown substantially. As of March 2021, the year-over-year growth of the money stock registered 24.2 percent. As Schooled readers may recall, a useful way to think about the relationship between the quantity of money (Figure 2) and its purchasing power (Figure 1) is with the so-called income version of the quantity equation (or, quantity equation, for short), which we specify in the following way.

M × V = P × Y

In this equation, M represents the quantity of money—think, M2 (represented in terms of growth rates in Figure 2); P represents the overall price level—think, CPI (represented in terms of growth rates in Figure 1); Y represents real income, which economists empirically measure with real GDP; and V represents the income velocity of money, which economists define as the average number of times the quantity of money (M) is exchanged for nominal GDP (P×Y). For example, suppose the quantity of money in the economy is $15 (M = $15); and, suppose that during one year 30 pencils are produced, purchased, and valued at a price of $1 each (P × Y = $30). In this example, the income velocity of money equals 2: $15 of money facilitates $30 of nominal GDP per year, because each dollar changes hands, on average, 2 times per year in order to purchase $30 of nominal GDP.

The quantity equation is an identity: it is true given how we define M, V, P, and Y. It does not belong to a particular school of economic thought. Nor does it specify how the quantity of money (M) affects the overall price level (P). (Fundamentally, this lack of specificity exists, in part, because the equation includes three unrestricted variables, assuming the government sets M.) In order to pin down how the quantity of money affects the overall price level, we need at least a theory for why individuals hold—or, in the parlance of economics, demand—money as opposed to so-called illiquid assets such as homes or ownership shares in corporations. A useful simplifying assumption, and a favorite working assumption of inflation hawks, is that individuals hold amounts of money in roughly fixed proportion to their nominal income, so that the velocity of money is roughly constant over time. In this case, then, the quantity equation implies that the growth in the money supply (M) equals the growth of nominal GDP (P × Y). Thus, if we assume the velocity of money is constant, the consequence of a 24 percent increase in the (M2) money supply is a 24 percent increase in nominal GDP (P × Y)—profound, to say the least!

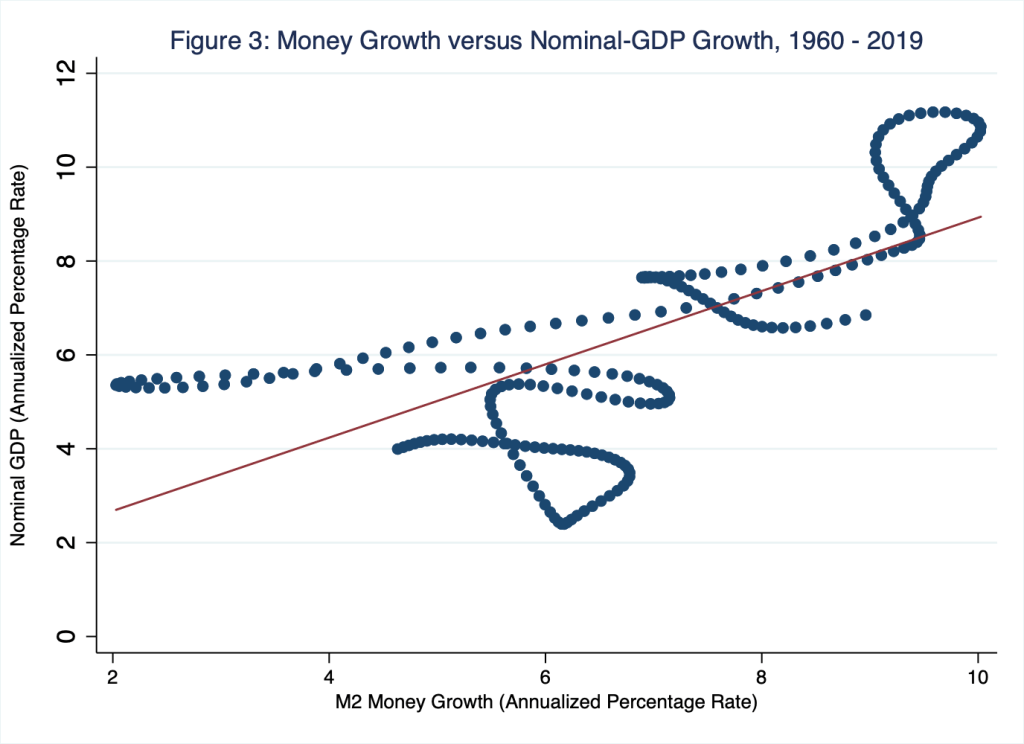

In Figure 3, I use a simple scatterplot to illustrate the (long-run) relationship between trend growth of the M2 money stock (M) and trend growth of nominal GDP (P × Y); I include the red fitted line as a visual aid in order to emphasize the tendency for these variables to move in tandem on trend.

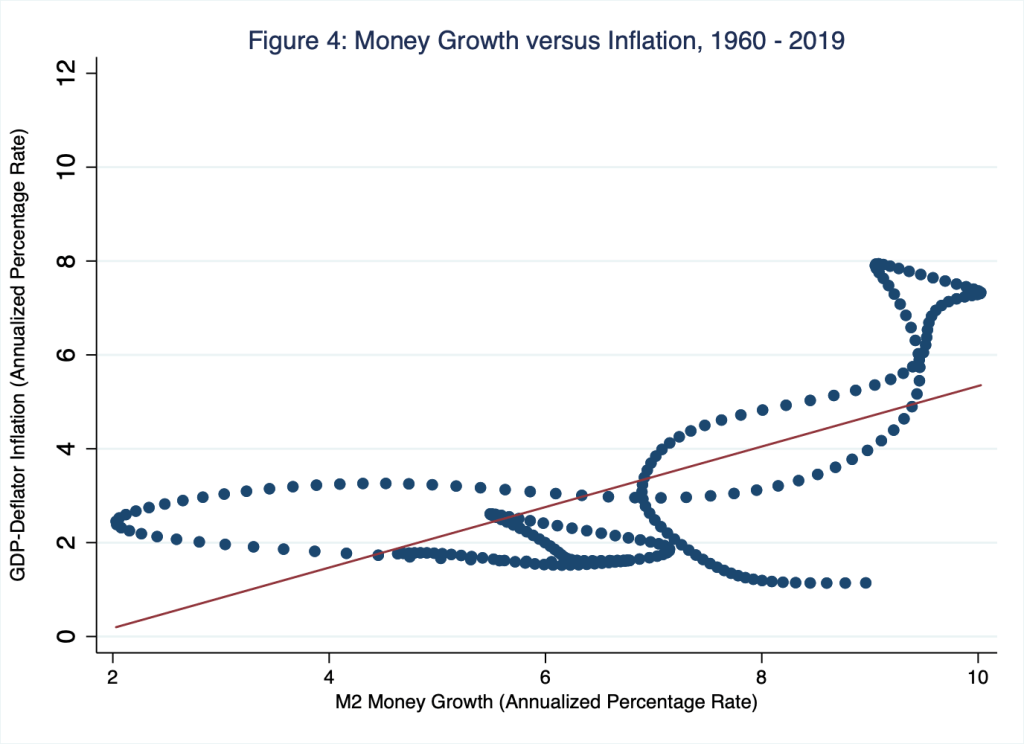

The key takeaway from Figure 3 is that, in the long run, trend growth in nominal GDP (P × Y; vertical axis) accompanies trend growth in the money stock (M; horizontal axis) almost one for one; thus, in the long run, velocity is rather stable. Of course, two forces necessarily shape trend growth of nominal GDP: namely, trend growth of the average price level (P) and trend growth of real GDP (Y). Thus, no doubt, some of the growth in nominal GDP that accompanies the growth in the money stock (Figure 3) over the long run is driven by real economic activity, not inflation. Long-run real economic activity is driven, in turn, by non-monetary forces such as investments in physical and human capital and increases in innovation. Controlling for the effects of real economic activity on nominal GDP—and, thus, isolating the effects of the money stock on the price level—affords a clearer empirical picture of how growth in the money stock drives inflation in the long run. So, in Figure 4, I again use a simple scatterplot, this time to illustrate the relationship between trend growth of the M2 money stock (M) and trend growth of the average price level (P); and again I include the red fitted line as a visual aid in order to emphasize the tendency for these variables to move on trend in tandem.

The key takeaway from Figure 4 is that, in the long run, trend growth in the average price level (P; vertical axis) generally accompanies trend growth in the money supply (M; horizontal axis), though somewhat imprecisely and, in any case, less than one for one. If we assume growth in the money stock is a policy variable controlled independently by, say, the central bank, then Figure 4 implies that, in the long run, relative growth in the money stock causes inflation. Informed by the quantity equation, inflation hawks are inclined to draw this implication from Figures 1 through 4: the year-over-year rate of inflation registered in April 2021 (Figure 1) is not a transitory, one-off outcome related only to a resumption of normal economic activity; rather it is a persistent acceleration of inflation resulting from substantial growth of the money stock (Figure 2).

Keynes would think inflation hawks are for the birds.

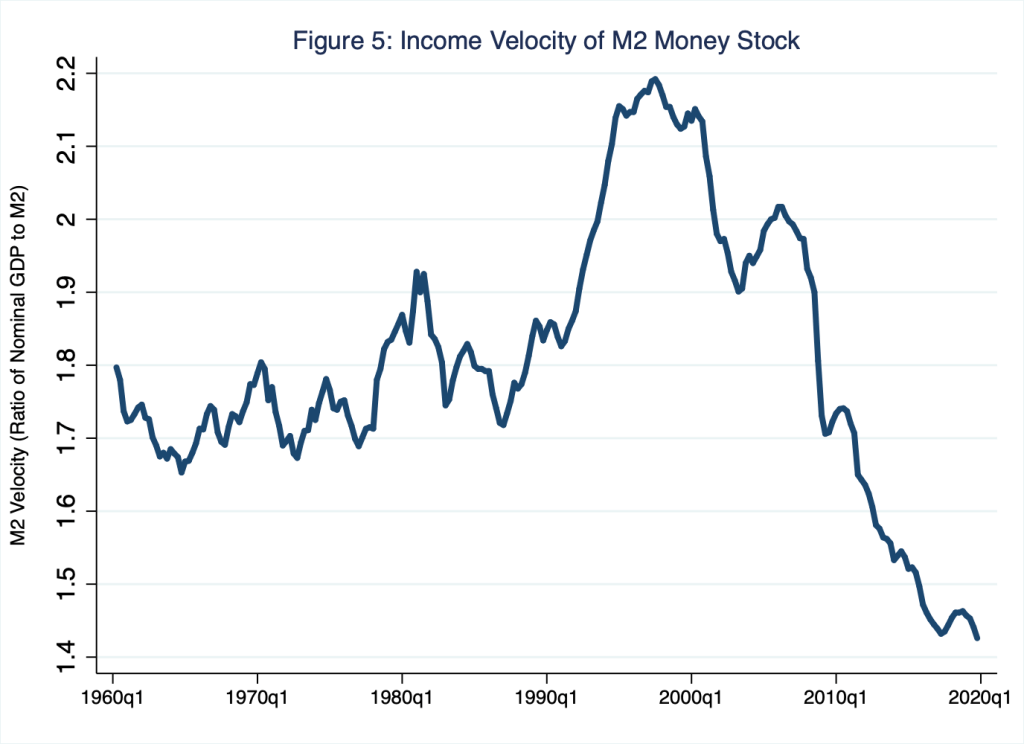

The velocity of money is determined by our demand for money, and our demand for money does strange things at exceptionally low interest rates. The interest rate represents the opportunity cost of holding (necessarily non-interest-earning) money. Keynes referred to a situation of exceptionally low interest rates as a liquidity trap: that circumstance in an economy where, because the opportunity cost of holding money is exceptionally low (and because holding money is convenient and useful in any case), the demand for money essentially accommodates the supply of money: we willingly hold—think, demand—money, no matter how much of it circulates. Put differently, in a liquidity trap, the velocity of money falls, a lot. This is a really big deal, because, as you may recall, our earlier hawkish interpretation of the quantity equation rests on a stable—and, in principle, constant—income velocity of money; but what if the velocity of money behaves otherwise? In Figure 5, I illustrate the income velocity of the M2 money stock; thus, in the context of the quantity equation, the line in Figure 5 illustrates the measure, (P × Y)/M.

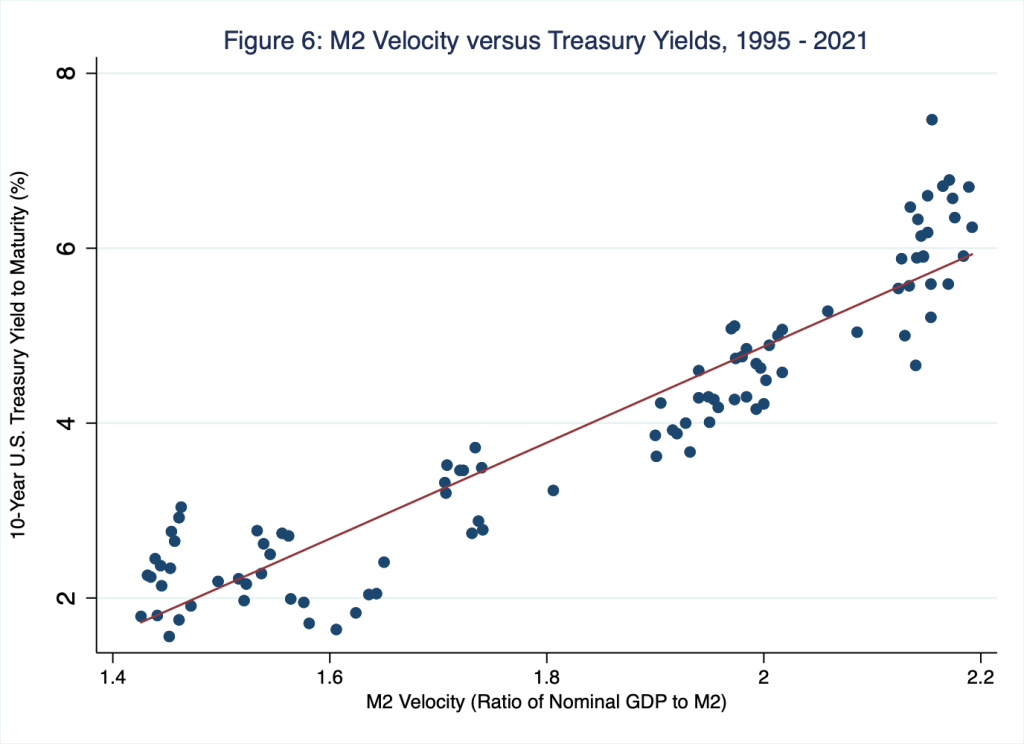

According to Figure 5, the income velocity of money has fallen dramatically since the financial crisis in 2008; and it has remained low throughout the pandemic. Essentially, because the opportunity cost of holding money is exceptionally low (and, incidentally, the safety of so-called “cash” is highly sought after by many), the demand for money is exceptionally high. In Figure 6, I illustrate this relationship between the velocity of money (along the horizontal axis) and the interest rate (along the vertical axis); and yet again, I include the red fitted line as a visual aid in order to emphasize the tendency for these variables to move in tandem: when interest rates are low, so too is the income velocity of money.

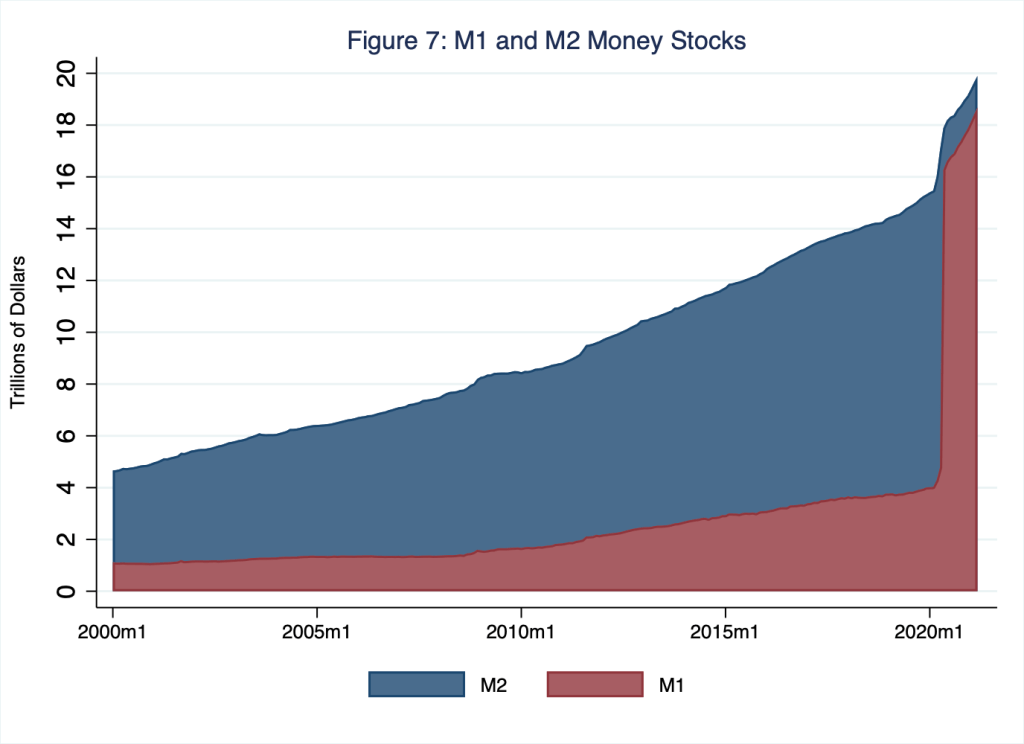

Evidence of the liquidity trap that Keynes proffered presents in the very-far-left, bottom corner of Figure 6, where both interest rates and the velocity of money are exceptionally low. Yet another way to see the current preference for money is by deconstructing M2 into the highly liquid M1—currency plus checking-account deposits—and the remaining components of M2, including, for example, savings-account deposits. In the liquidity hierarchy of the U.S. money stock, currency is more liquid than the remaining components of M1 and M1 is more liquid than the remaining components of M2. I illustrate this decomposition of the money stock in Figure 7, in which the extraordinary rise in M2 (which we saw in Figure 2) and the extraordinary compositional shift into the M1 share of M2 are visible: we not only hold relatively large quantities of money (blue in Figure 7), we hold the most-liquid forms of money (red in Figure 7).

Thus, according to Figure 5, the demand for money has grown to accommodate its large stock; meanwhile, according to Figure 7, that demand for money has taken the form of a demand for the most-liquid components of the stock of money. So long as everyone demands the extraordinarily large money supply, the purchasing power of money need not fall; thus, persistently high inflation need not result. Unless, of course, we expect persistently high inflation.

Expect it and it will come.

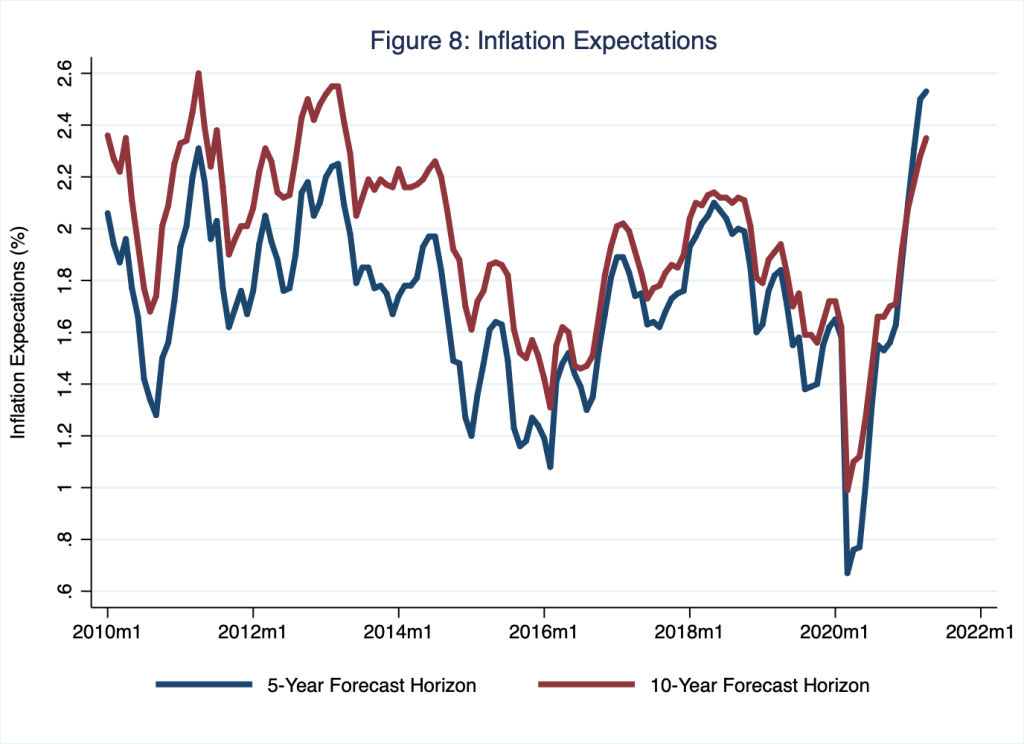

Funny thing about expectations of inflation, they can be self fulfilling. This is because when we expect, say, high inflation, we take steps to protect ourselves; for example, we raise the prices of goods and services that we provide and we reduce our demand for money (thus causing velocity to rise). In the aggregate, when we all take these steps en masse, the average price level rises, regardless of the size of the current stock of money. Put differently, if we expect persistently high inflation—because of the recent exceptional rise of the stock of money or because of the relatively high inflation rate the BLS recently reported or because of something else—then persistently high inflation is just what we might get. In Figure 8, I illustrate inflation expectations (measured as breakeven yields to maturity on nominal and real U.S. Treasury bonds) at the five-year and ten-year forecast horizons.

According to Figure 8, expectations of inflation have risen since the start of the pandemic. Based on this measure, the rate of inflation expected five years from today is roughly 2.5 percent, higher than the rate of inflation (of roughly 2.4 percent) expected ten years from today. So, although at neither forecast horizon is the expected rate of inflation alarmingly high, these expectations of inflation are, for the moment at least, above the Federal Reserve’s long-run target of 2 percent. Fundamentally, this difference between 2 percent and the relatively long-run expectations at five- and ten-year forecast horizons may signal a weakening of the central bank’s credibility to deliver low and stable inflation around 2 percent. And this matters, because weakened central-bank credibility—as opposed to any single month’s actual year-over-year inflation rate—is the greatest threat to price stability the U.S. economy now faces.

3 thoughts on “great (inflation) expectations”