This blog post accompanies the SDPB Monday Macro segment that airs on Tuesday, February 7, 2023. Click to here to listen to the segment. And for more macroeconomic analysis, follow @NSMEdirector.

Congress and the White House are battling over raising the so-called debt ceiling, what the US Treasury defines as “the total amount of money that the United States government is authorized to borrow to meet its existing legal obligations, including Social Security and Medicare benefits, military salaries, interest on the national debt, tax refunds, and other payments.” The ceiling is currently set at $31.4 trillion. When the amount of the national debt outstanding reaches the debt ceiling, Congress must act to raise the ceiling, or the federal government must default in some way: it must fail to honor its financial obligations—debt payments or otherwise, the distinction is immaterial as far as financial markets (and most economists) are concerned. Because the national debt has increased more-or-less continuously for the last several decades, Congress has raised the ceiling many times. For example, according to the U.S. Treasury, since 1960, Congress has raised the ceiling 78 times, under presidents of both parties: 49 times under Republican presidents and 29 times under Democratic presidents. Importantly, raising the debt ceiling does not change the flows of tax revenues, transfer payments, or government expenditures. Rather, raising the debt ceiling simply authorizes the U.S. Treasury to borrow funds when tax revenues net transfer payments are less than government expenditures, including payments of interest and principal associated with the national debt.

Thus, if the national debt reaches the debt ceiling, then the U.S. Treasury cannot borrow to meet the federal government’s existing obligations, and borrow it must if tax revenues net transfer payments continue to fall short of government expenditures; this shortfall has occurred reliably for the last several decades. Of course, Congress, and not the U.S. Treasury, determine the federal government’s existing obligations. This is to say, the U.S. Treasury must issue debt precisely because Congress allows tax revenues net transfer payments to fall short of government expenditures. In any case, conventional wisdom teaches that failure to raise the debt ceiling would invite financial Armageddon. According to the U.S. Treasury, for example, “Failing to increase the debt [ceiling] would have catastrophic economic consequences.” This wisdom is based, in part, on the relationship between the national debt and the U.S. bond market, in which U.S Treasury securities play an outsized role.

The U.S. Treasury issues the national debt largely in the form of marketable U.S. Treasury securities: namely, U.S. Treasury bills, notes, and bonds, currently (face) valued at roughly $31 trillion—the size of the U.S. national debt, not coincidentally. Bills, notes, and bonds are fixed-income debt securities the U.S. Treasury sells—the sale price is the amount the U.S. Treasury borrows at the point of sale—with the promise to pay the holder of the security a fixed U.S.-dollar-denominated face value—think, $100—at a specified future date; the arrangement may also include periodic interest (aka, coupon) payments. Finally, the timespan between the initial sale of the security—the bill, the note, or the bond—and the specified future date on which the U.S. Treasury pays the holder of the security its face value is the security’s maturity: bills mature in a year or less, notes mature between 1 and 10 years, and bonds mature in 10 years or more. Put differently, then, the U.S. Treasury does not take out loans in the conventional way that you and I do. Rather the U.S. Treasury sells I.O.U.s in its name, something only large, well-known borrowers get to do.

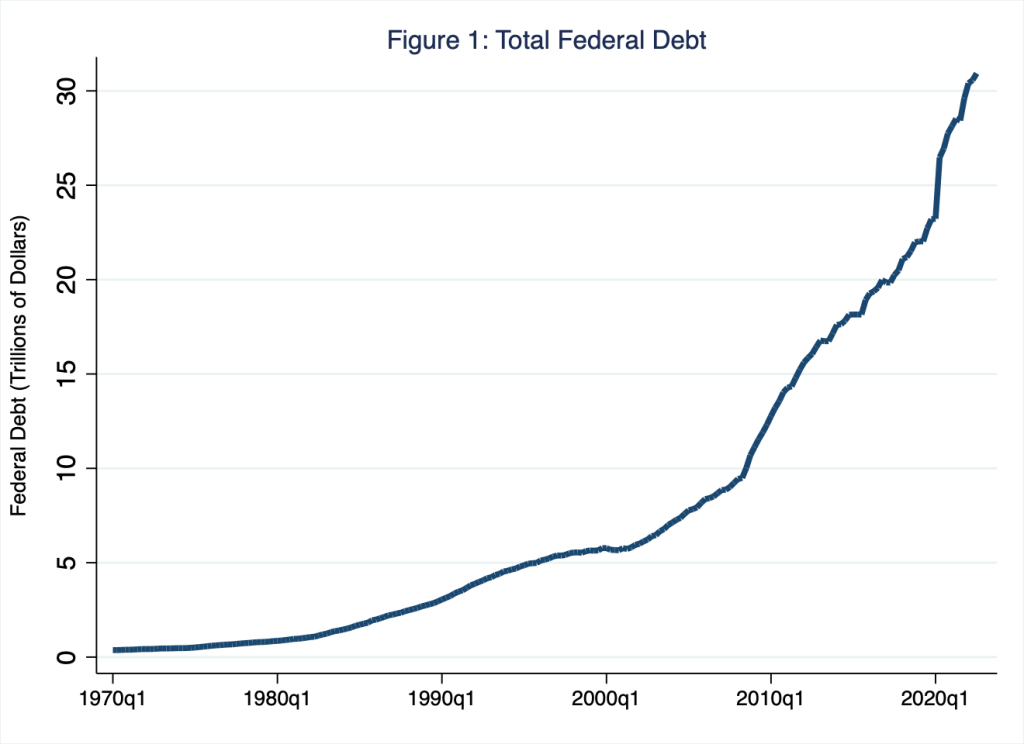

In Figure 1, I illustrate the total amount of U.S. national debt outstanding; according to the vertical axis in this figure, as of late 2022, the national debt essentially reached the debt ceiling of roughly $31 trillion.

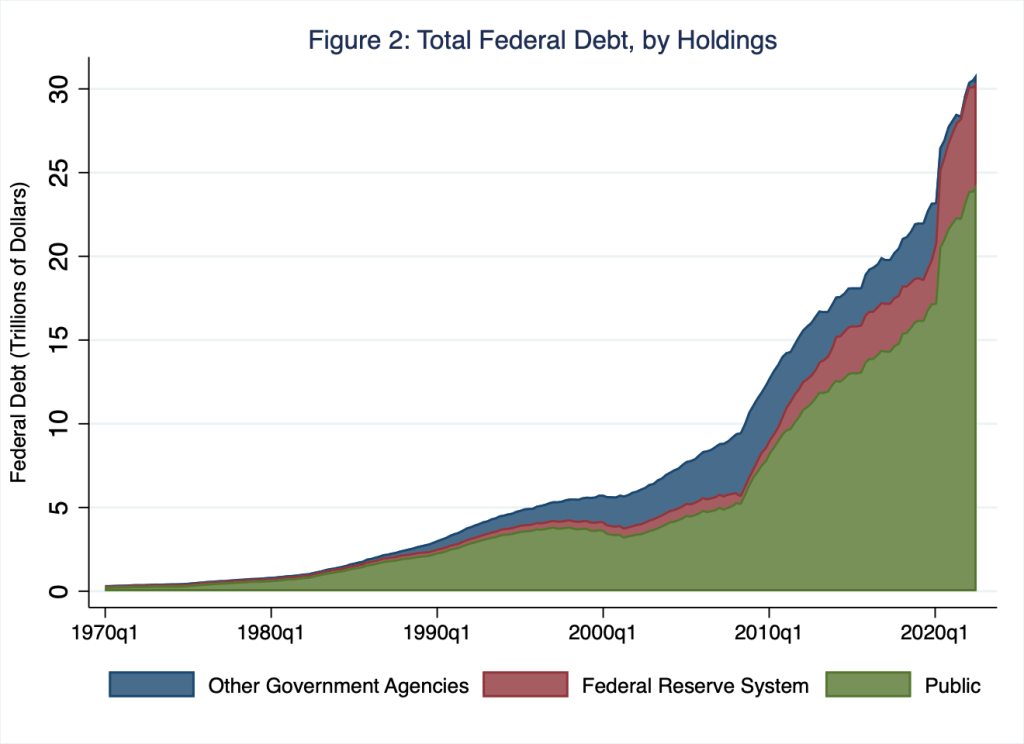

Treasury securities that comprise the national debt are owned by the (non-U.S. governmental) public—domestic and foreign—and U.S. national government agencies. In Figure 2, I illustrate the broad composition of such debt holders, which I identify as either the (non-U.S. governmental) public, the Federal Reserve System, or other government agencies.

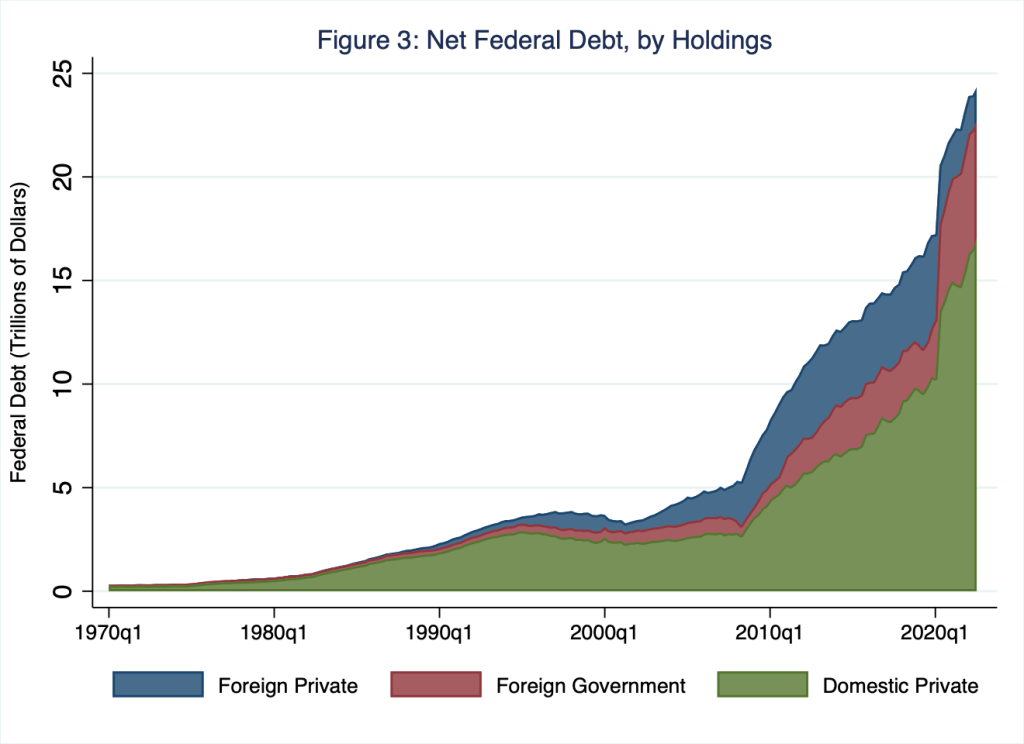

For any quarter in Figure 2, the sum of green, red, and blue areas equals the national debt—again, roughly $31 trillion in the third quarter of 2022, for example. In general, the Federal Reserve System (red area) purchases and sells U.S. Treasury securities to implement the central bank’s monetary policy. Other government agencies (blue area)—think, for example, the Social Security Administration, which invests its surpluses in U.S. Treasury securities—hold U.S. Treasury securities as well. Finally, the public (green area)—that is, non-U.S. governmental entities, domestic or foreign—hold the very-large remainder of U.S. Treasury securities. As a practical matter, these $31 trillion of publicly traded U.S. Treasury securities constitute the current secondary market for U.S. sovereign debt. As I illustrate in Figure 3, in the third quarter of 2022, the public holders of these securities—green area in Figure 2—included mostly domestic private investors (green area; roughly $17 trillion), as well as foreign governments (red area; roughly $6 trillion) and foreign private investors (blue area; roughly $2 trillion).

Investors throughout the global financial system unanimously perceive U.S. Treasury securities as a default-risk-free financial asset, as near to a sovereign-issued monetary store of value as one could get absent the U.S. monetary base—Federal Reserve notes in circulation and bank reserves held at the Federal Reserve. U.S. Treasury securities embody the presumably immutable full faith and credit of the U.S. Treasury. Moreover, the U.S. Treasury securities market is exceptionally liquid: thanks to many buyers and many sellers, market participants can easily trade the securities; trading-transaction costs are reliably low and prices are relatively stable. Thus, technically speaking, deep liquidity renders U.S. Treasury securities information insensitive: news that propagates potentially destabilizing one-sided trading—all buyers or all sellers—and, in doing so, generally distorts the prices of most other financial assets, leaves the prices of U.S. Treasury securities relatively unaffected.

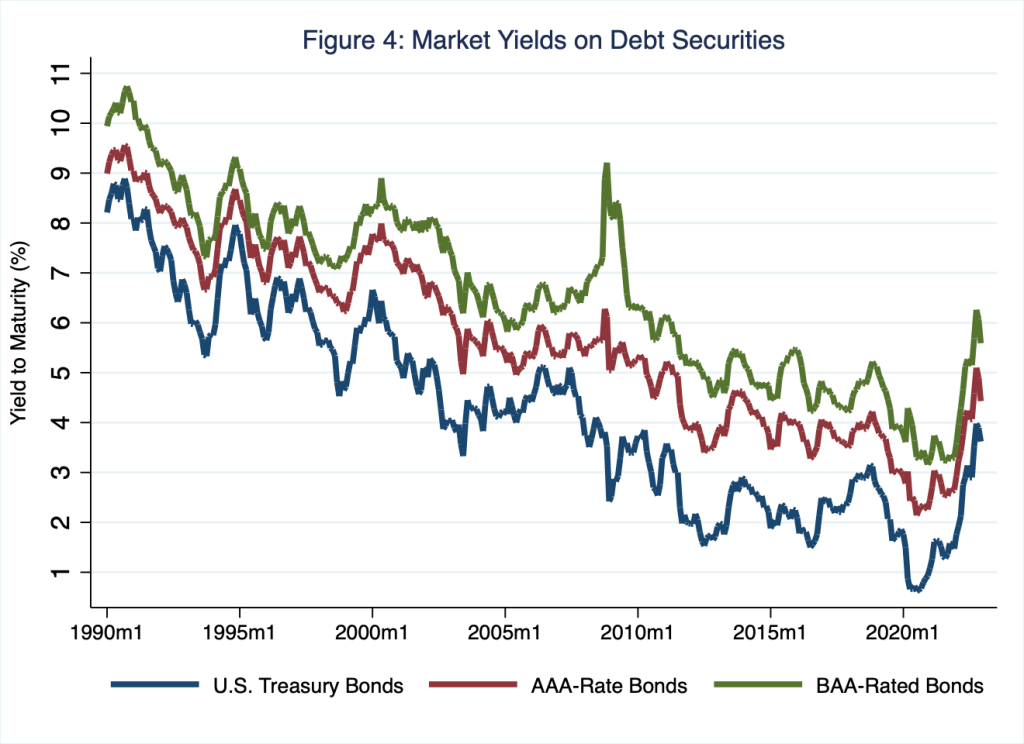

In this way, the global financial system relies on U.S. Treasury securities to stem systemic fragilities—to absorb crises, as it were. When all breaks loose, investors run to U.S. Treasury securities. To be sure, its preferred status as a risk-free borrower affords the U.S. Treasury an extraordinary privilege to borrow at relatively low rates of interest; the nominal yields to maturity the Treasury pays on its securities are consistently among the lowest in the world. Moreover, these interest rates are the benchmark rates borrowers and lenders use to determine the cost of financing throughout the global financial system; a typical 30-year mortgage rate is often benchmarked to a Treasury bond rate, for example. I illustrate this pattern in Figure 4, in which I chart the yields to maturity on long-term U.S. Treasury bonds, AAA-rated corporate bonds, and BAA-rated corporate bonds.

According to Figure 4, yields to maturity—think, rewards to the lender for owning the bond—trace a very clear pattern: the yields on U.S. Treasury bonds are below the yields on AAA-rated corporate bonds, which, in turn, are below the yields on BAA-rated corporate bonds: because investors are generally risk averse, investors take risks only if they are rewarded for doing so. And because investors reason the default risk on Treasury bonds is essentially zero, investors demand a higher yield to maturity on bonds issued by borrowers who present default risks—all borrowers other than the U.S. federal government, presumably. (BAA-rated corporate bonds expose lenders to greater default risk than AAA-rated corporate bonds do.)

When the national debt reaches the debt ceiling imposed by Congress, and government expenditures continue to exceed tax revenues net transfer payments, the federal government cannot borrow to honor its obligations; suddenly, the federal government presents a default risk. Although this default risk would be associated with all federal government obligations, because technically speaking the federal government could default on Social Security payments, for example, financial-market participants would associate this default risk with federal government obligations in relation to U.S. Treasury securities in any case. Indeed, were the federal government to default on, say, obligations related to Social Security and honor obligations related to Treasury securities, financial markets would perceive this so-called selective default as a technical default on Treasury securities no matter.

Not surprisingly, perhaps, introducing default risk to the U.S. Treasury securities market would disrupt the now-natural order of things: if U.S. Treasury securities carry default risk, then they become information sensitive: news that now propagates potentially destabilizing one-sided trading in privately issued debt would do the same for U.S. sovereign debt. In this case, the global financial system could no longer rely on U.S. Treasury securities to absorb the panic instigated by financial crisis, including a traditional banking crisis—think, “It’s a Wonderful Life”—because the U.S. Treasury undergirds the Federal Deposit Insurance Corporation. Terrifying, I know. The loss of an information-insensitive financial asset could only destabilize the global financial system. The extent of this destabilization is a known unknown: the modern global financial system has never operated without the U.S. Treasury market acting as a safe haven; the absence of that safe haven could only amplify the damage that financial crises impose on the economy. This damage is particularly tragic because the debt ceiling is an arbitrary construction of Congress; this is to say, the debt ceiling is not really a thing. Global financial markets would gladly permit the U.S. Treasury to borrow more than $31.4 trillion dollars, for example, if only Congress would allow the Treasury to do so.

Finally, the standard argument for not raising the debt ceiling is that the ceiling imposes fiscal discipline on the federal government. Fiscal discipline is a worthy objective to be sure. However, the ceiling does no such thing, because the ceiling is, in effect, backward looking: the ceiling limits the extent to which the federal government could borrow to honor its existing obligations—those the federal government incurred in the past. I suppose the threat of inviting financial Armageddon could incentive lawmakers to limit government expenditures or raise taxes net transfer payments going forward, so as not to reach the debt ceiling, but, in my view, such an approach to imposing fiscal discipline is neither sensible nor persuasive. If Congress seeks fiscal discipline, it should implement tax, transfer, and expenditure policies accordingly. Besides, because default risk raises yields to maturity on U.S. Treasury securities, failing to raise the debt ceiling raises the cost to the federal government—and, so, the cost to taxpayers—of servicing the national debt. Thus, failing to raise the debt ceiling is contrary to imposing fiscal discipline.