This blog post accompanies the SDPB Monday Macro segment that airs on Tuesday, January 3, 2023. Click here to listen to the segment, which appears under the heading, “Modeling with the stars.” And for more macroeconomic analysis, follow @NSMEdirector.

Macroeconomists study the economy as a whole. As such, we are most interested in the general features of the economy—those measures of aggregate quantities and average values that pertain to the central tendencies of aggregate economic activities; think, for example, total output (measured as real gross domestic product, say) and the unemployment rate, which are measures of aggregate quantities, or the interest rate and the average price level, which are measures of average time and transaction values of money, respectively. Moreover, we think about these general features of the economy as outcomes shaped by two, interrelated forces: namely, market forces, such as a supply-chain shock, and macroeconomic-policy forces, such as a fiscal-stimulus shock. And finally, we evaluate these outcomes—the current unemployment rate or the current inflation rate, say—against their respective social-welfare-optimizing levels, counterfactual outcomes that characterize the macroeconomy when it lives its best life.

This is where things get particularly interesting.

A standard, canonical model of a macroeconomy characterizes—or, in the mathematical parlance of macroeconomics, pins down—three measures of the economy as a whole: namely, with common notation in parentheses, output (), the real interest rate (), and the average price level (). Other models characterize many other measures as well, of course. For the purposes of this blog post, I’ll focus on these three measures. Where the model economy achieves a so-called competitive equilibrium—where markets for all goods, services, and risks simultaneously clear in all time periods and without externalities—the equilibrium levels of output (), the real interest rate (), and the average price level () are socially optimal; at these equilibrium levels, which we denote , , and , respectively, the macroeconomy lives its best life. Incidentally, because we refer to the superscripted asterisks as stars, we pronounce, say, the variable as y star.

So what does this matter? Well, macroeconomic policymakers are either steeped in macroeconomic theory or they are advised and counseled by macroeconomists who are steeped in macroeconomic theory. Thus, when policymakers navigate a path for macroeconomic policy, they look to the stars; that is, they target , , and —known unknowns, empirically speaking at least.

So let’s look to the stars: namely , , and .

The optimal level of output,, at a moment in time is the product of labor productivity, labor hours per employee, the employment rate, the labor-force participation rate, and the population. Meanwhile, the annual percentage change in over time describes economic growth, which is necessarily a dynamic process. As a practical matter, labor productivity is the principal source of economic growth. The other factors that determine —namely, labor hours per employee, the employment rate, the labor-force participation rate, and the population—are largely shaped by the institutional structure of labor markets—the forty-hour workweek and the degree of labor mobility, for example—and demography; these are important social forces that nevertheless change slowly relative to economic growth.

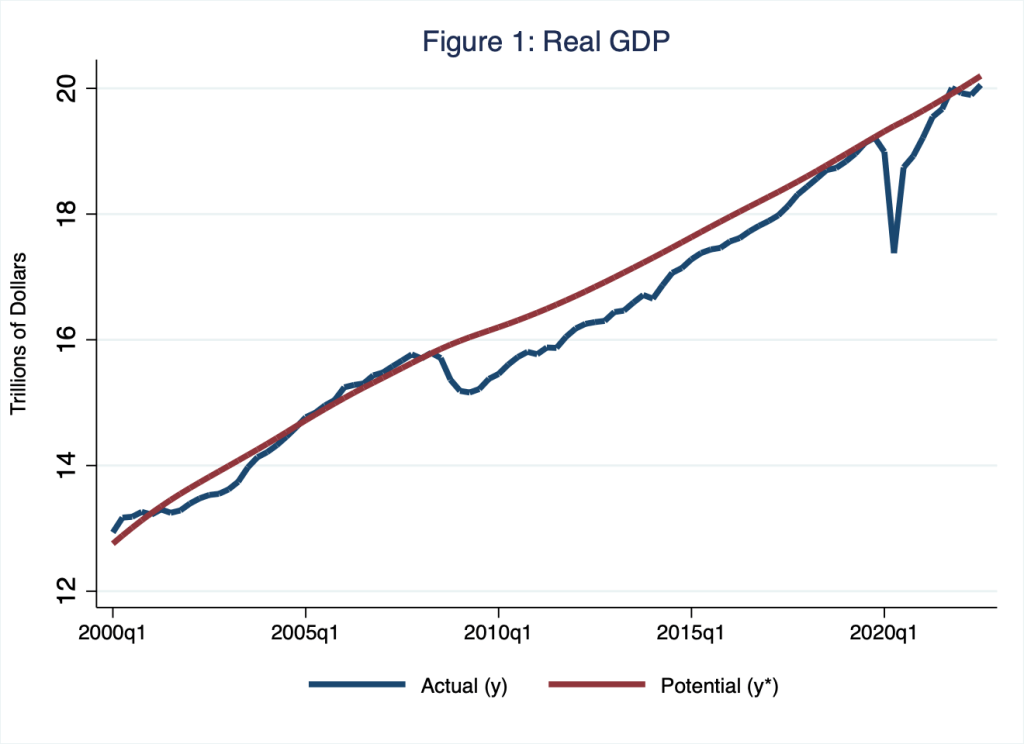

The most effective way to sustain economic growth, which we denote , through labor-productivity growth is to improve technology—the recipe, as it were, that transforms inputs, such as labor and capital, into outputs. Most economists reason that technological improvement is a largely endogenous process, an outcome of competitive interactions of firms maximizing shareholder value and operating in an economic environment that incentivizes activities that increase private and social returns. Not surprisingly, then, productivity is most likely to grow in an economic system of sensibly regulated market capitalism, complete with specialization and exchange (including international trade), where free enterprise and property rights are ensured. Based on this underlying theory, the U.S. Congressional Budget Office estimates , from which we could calculate . In Figure 1, I illustrate actual and its counterfactual optimum, .

Source: Federal Reserve Bank of St. Louis (FRED) series GDPC1 and GDPPOT.

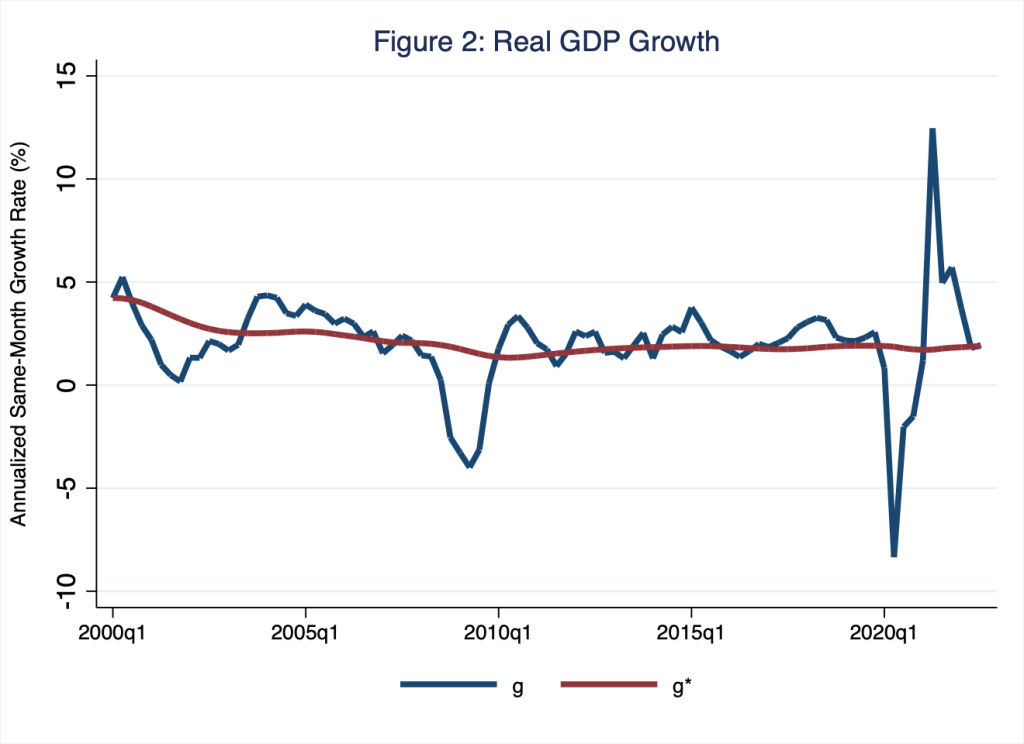

According to Figure 1, the U.S. economy has very nearly achieved a level of output consistent with ; this is to say, actual output (blue line; ) has nearly achieved its potential level (red line; ). Though, in the first three quarters of 2022, fell below , the likely consequence of macroeconomic-policy tightening on the part of the U.S. Federal Reserve. Thus, based on this evaluation of versus , the U.S. economy is operating at a level of output below its potential. And perhaps more importantly, the growth rates of and — and , respectively—have converged. In Figure 2, I illustrate these growth rates, each of which reached 1.9 percent in the third quarter of 2022—the last quarter for which data are currently available.

Source: Federal Reserve Bank of St. Louis (FRED) series GDPC1 and GDPPOT.

Thus, according to Figure 2, the good news is that U.S. economic growth has reached its potential: this is to say, , because, in the context of Figure 2, as of the third quarter of 2022 the blue and red lines intersect. Nevertheless, the bad news is twofold: first, actual economic growth () is noisy from one quarter to the next; the actual growth rate is unlikely to remain equal to its potential rate. To be sure, given the current macroeconomic-policy tightening on the part of the U.S. Federal Reserve, economic growth is likely to average below for at least the next few quarters. Second, even if economic growth consistently registers a rate in the neighborhood of , the output gap I illustrate in Figure 1 would not close, because in this case and grow at the same rate—think, the blue and red lines in Figure 1 remain parallel.

The optimal real interest rate, , is the “real [inflation-adjusted] short-term interest rate consistent with output equaling its natural rate and constant inflation” (Holston, Laubach, and Williams, 2016). Or, less formally, macroeconomists often think about as the appropriate real short-term interest rate for a so-called Goldilocks macroeconomy—one that is neither too hot nor too cold but rather just right.

But what underlying forces drive ? Seems to me the most-sensible way to think about is based on a standard, canonical model of a macroeconomy. (For the hardcore Monday Macro fans: I have in mind a standard, non-stochastic Ramsey model with finite households, infinitely lived agents, logarithmic CRRA utility, and Cobb-Douglas production.) In such a model, the following simple relationship holds.

Where is the so-called discount rate and is, as I defined it earlier, the annual percentage change in —think, long-run productivity growth. The discount rate () reflects our time preference. Suppose, for example, that measured on an annual basis, , so that our discount rate is 2 percent. This means that in order for me to surrender to you otherwise-current consumption of, say, 100 coconuts, I demand in return in a year from now future consumption of 102 coconuts. The greater is , the greater is my preference for current consumption, and so the higher is the real interest rate () all else equal: the greater is , the more coconuts I demand in return for surrendering current consumption for future consumption. Intuitively speaking, a poor saver has a relatively high : a poor saver requires a relatively high incentive to save. Meanwhile, since around the Great Recession, has hovered around 2 percent. Thus, according to the relationship above, my naive assumption that , and the fact that has hovered around 2 percent, would equal around 4 percent, for example.

Okay, so economic theory strongly implies that is driven by fundamental features of the economy, including our time preference for consumption ()—and, thus, our time preference for saving—and the growth rate of labor productivity (). According to empirical measures of , which I analyze in detail in the Monday Macro segment, R Star Is Born, has fallen throughout much of the late twentieth century; in the early 1960s, the rate hovered around 5 percent, whereas in the late 1990s, the rate hovered around 2.75 percent. Sometime around the Great Recession beginning in 2009, seems to have fallen dramatically; estimates of Holston, Laubach, and Williams (2016) placed it around 0.49 percent just prior to the pandemic.

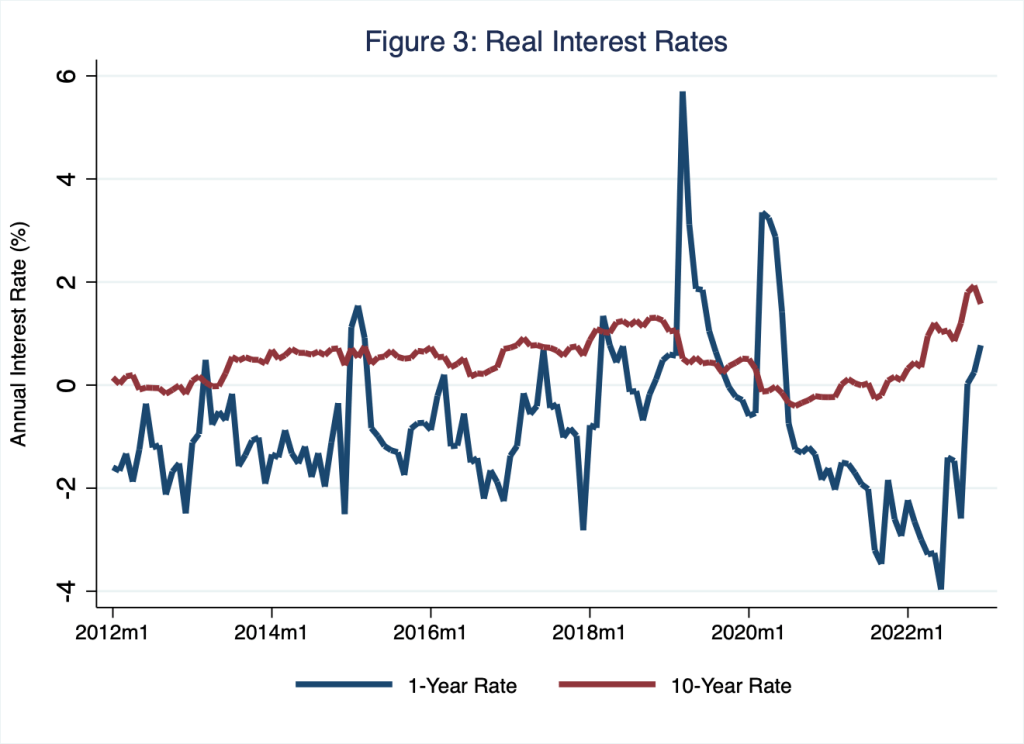

In my view, the implications of registering less than half a percent are quite astounding, given that has hovered around 2 percent: if the admittedly simple relationship above informs how we think about , and I think it should, then must be negative. How else could if equals 0.50 percent and equals 2 percent? But if is negative, on balance we prefer future consumption over present consumption. I know of no one whose consumption behavior is adequately described by a negative . Put simply, then, our working estimates of seem to me to be too low and, thus, misaligned with an economy that achieves its best life, characterized here by (and ) and . Monetary policymakers should consider targeting a level of that is higher than these working estimates. In Figure 3, I illustrate empirical measures of actual (as opposed to ) at one-year and 10-year horizons.

Source: Federal Reserve Bank of St. Louis (FRED) series REAINTRATREARAT1YE and REAINTRATREARAT10Y.

According to Figure 3, as of December 2022, the actual one-year real interest rate registered 0.77 percent—higher than the deeply negative levels this rate registered in the aftermath of the pandemic, but still too low in my view. Again, do you know a saver who is content with an annual real return on savings of far less than one percent? I don’t.

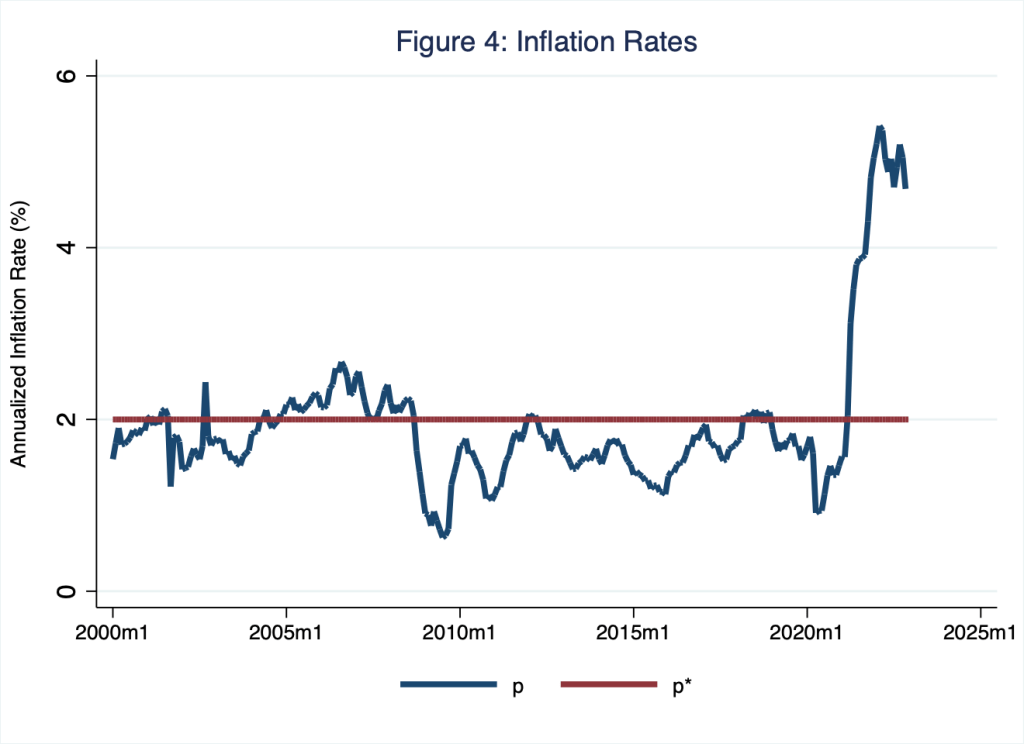

The optimal average price level,, is a measure of the purchasing power of money, independently of the goods and services for which the money is exchanged. Meanwhile, the annual percentage change in over time describes the optimal rate of inflation, which is necessarily a dynamic process. Unlike and , which derive their theoretical measures from microeconomic foundations, the annual percentage change in is determined somewhat arbitrarily by central banks. Today, most central banks, including the Federal Reserve System, set the annual percentage change in equal to around 2 percent on average. This is to say, most central banks target an inflation rate of around 2 percent. In Figure 4, I illustrate the inflation rate based on the measure the Federal Reserve prefers: namely, the core personal consumption expenditures chain-weighted price index; additionally, I illustrate the 2-percent target (red line).

Source: Federal Reserve Bank of St. Louis (FRED) series PCEPILFE.

According to Figure 4, the rate of inflation—the annual percentage change in —remains well above the 2-percent target—the annual percentage change in . The purchasing power of money is falling too quickly relative to the central bank’s preference for low and stable inflation.

Currently, the stars do not align.

This basic assessment of the general features of a standard, canonical model of a macroeconomy suggests all is not right with the U.S. economy. Moreover, this basic assessment suggests why. The annual percentage change in , the annual rate of inflation, exceeds its target by more than three percentage points; technically speaking, the annual percentage change in is greater than the annual percentage change in . Meanwhile, the economy is producing a level of output that is just below the economy’s potential; . I reason the suboptimal inflation outcome persists because the real interest rate remains too low; . Put differently, monetary policy remains too loose; the Federal Reserve must continue to raise its target for the federal funds rate.

This reasoning is somewhat controversial, because many observers of the macroeconomy argue that, in the aggregate, the discount rate () has fallen substantially, driving to near zero and, thus, requiring the central bank to tighten—think, raise the real interest rate—by less than it would otherwise. I disagree. In any case, I guess we will know sooner or later whether the real interest rate is sufficiently high. I would prefer we know sooner rather than later; time preference is a powerful thing.

References

Holston, Kathryn, Thomas Laubach, John C. Williams. 2016. “Measuring the Natural Rate of Interest: International Trends and Determinants.” Federal Reserve Bank of San Francisco Working Paper 2016-11.

One thought on “stargazing”