This blog post accompanies the SDPB Monday Macro segment that airs on Monday, May 1, 2023. Click here to listen to the segment. For more macroeconomic analysis, follow J. M. Santos on Twitter @NSMEdirector.

On Friday, April 28th, Michael Barr, Vice Chair for Supervision for the Federal Reserve Board of Governors, released the central bank’s 100-page report of its internal investigation into the closure, on March 10, 2023, of Silicon Valley Bank. Importantly, the investigation centered on how, if at all, the central bank’s supervision and regulation of SVB (and its parent holding company, Silicon Valley Bank Financial Group [SVBFG]) contributed to the closure. As you may recall, the collapse of SVB was unprecedented for its speed and conventional nature: the proximate cause of the closure was a 21st-century version of a 1930s-styled run on the bank, which experienced a $40 billion deposit outflow on March 9th; and the bank’s management team expected a $100 billion deposit outflow on March 10th, thus the bank’s closure by the California Department of Financial Protection and Innovation. Within the Federal Reserve System, SVB—an FDIC-insured, state-chartered, Fed-member commercial bank—and SVBFG fell within the regulatory purview of the Federal Reserve Bank of San Francisco.

The authors of the report identified four key takeaways from their investigation: the first blames SVB for its closure, the second, third, and fourth blame the Federal Reserve System. The first key takeaway pertains to SVB’s board of directors and management, which failed to appreciate and manage risks to which SVB was exposed. For example, directors and managers mismanaged interest-rate risk, an inherent feature of the process of maturity transformation—borrowing short and lending long—that generates profit for a bank. Apparently, directors and managers reasoned that a rise in interest rates would increase returns on assets while leaving the cost of securing deposits unchanged: higher interest rates implied higher profits.

Yeah, that’s not how any of this works. On the contrary, the intermediation business model is vulnerable to a sudden, large rise in interest rates. This is because when interest rates rise, a bank must soon increase the interest rate it pays to keep its necessarily short-term deposits, which depositors could otherwise withdraw; meanwhile, the bank cannot soon increase the interest rate it earns on its loans, because borrowers who took out those loans generally locked in a rate for a relatively long time. Put differently, when interest rates rise, the cost of a bank’s sources of funds generally rises while the return on a bank’s uses of funds generally does not: net interest margin falls. As the authors of the report put the matter:

SVBFG management was focused on the short-run impact on profits. SVBFG’s internal risk appetite metrics, which were set by its board, provided limited visibility into its vulnerabilities. In fact, SVBFG had breached its long-term [interest-rate risk] limits on and off since 2017 because of the structural mismatch between long-duration securities and short-duration deposits. In April 2022, SVBFG made counterintuitive modeling assumptions about the duration of deposits to address the limit breach rather than managing the actual risk. Over the same period, SVBFG also removed interest rate hedges that would have protected against rising interest rates. In sum, when rising interest rates threatened profits and reduced the value of its securities, SVBFG management took steps to maintain short-term profits rather than effectively manage the underlying balance sheet risks.

Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank (2023)

As Schooled readers know well, since the pandemic, the rate of inflation has risen several percentage points above the rate of two percent the Federal Reserve prefers. The monetary policy playbook is unambiguous about what to do in such a case of high and variable inflation: tighten monetary policy by raising short-term interest rates. And so the Federal Open Market Committee raised the target range for the federal funds rate from 0.00 to 0.25 percent in February 2022 to 4.75 to 5.00 percent now. SVB’s directors and managers had to see this tightening coming. Moreover, they had to realize that when the central bank rather suddenly and significantly raises the fed funds rate, short-term maturity interest rates more generally, including those paid on deposits, rise as well: thus, the cost of a bank’s short-term sources of funds rises relative to the return on a bank’s long-term uses of funds. Prudent risk management in this case consists of preemptively shortening the duration of assets (think, bank loans), lengthening the duration of liabilities (think, bank deposits), and paying depositors higher interest rates accordingly. To say SVBFG made counterintuitive modeling assumptions is an understatement, to say the least.

The second, third, and fourth key takeaways from the investigation blame the Federal Reserve System (and the U.S. banking regulatory framework more generally) for the closure of SVB. Essentially, aside from SVB’s lack of internal controls, the ultimate cause of SVB’s failure rests at the intersection of SVB’s extraordinary growth and a change in the U.S. banking regulatory framework—and, consequently, regulatory culture.

According to the report, the central bank’s regulators did not appreciate SVB’s vulnerabilities as the bank grew and its business model became more complex; regulators did not act quickly enough to ensure SVB addressed vulnerabilities regulators did appreciate and identify; and finally, regulators responded inadequately to the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA; 2018). Lawmakers ostensibly passed EGRRCPA to ease the regulatory burden the Dodd-Frank Wall Street Reform and Consumer Protection Act (hereafter, Dodd-Frank Act) imposed on banks in general and community banks—those with assets valued at less than $10 billion—in particular. For example, the act permits community banks to meet a simple community bank leverage ratio—tier-1 capital over average consolidated assets—instead of conventional ratios based on the risk composition of assets; and the act exempts these institutions from the Volcker Rule—which prohibits banks from trading, investing in, or sponsoring, with their proprietary accounts, hedge funds or private equity funds—and reduces the reporting requirements and examinations these relatively small institutions otherwise face.

Importantly, though, the act also intends to relieve regulatory burdens on relatively large institutions otherwise subjected to so-called enhanced prudential regulation (EPR). Specifically, Title IV of the act offers regulatory relief to relatively large institutions—those with assets valued between $50 and $250 billion—otherwise subject to EPR. The title exempts banks with assets valued between $50 and $100 billion from most enhanced regulation; meanwhile, though banks with assets valued between $100 and $250 billion remain subject to stress testing, these institutions are subject to enhanced regulation only at the discretion of the Federal Reserve System.

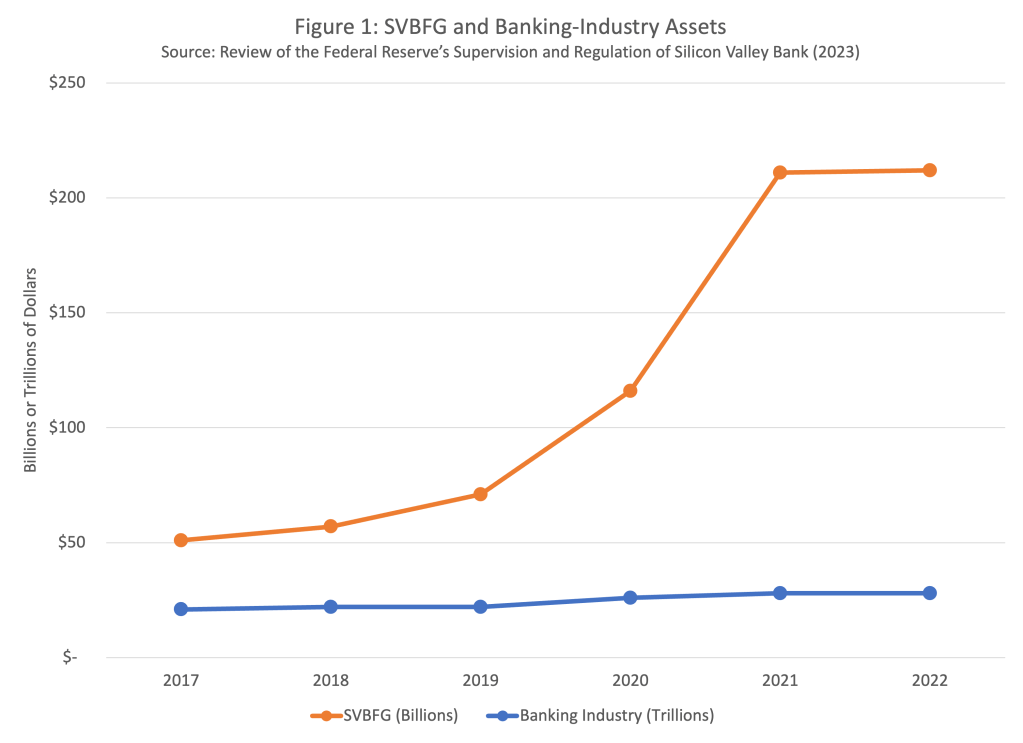

While regulators modified their practices to align with EGRRCPA, SVB grew extraordinarily, as I illustrate in Figure 1, in which I include the trillion-dollar values of assets in the banking industry (blue line) and the billion-dollar assets of SVBFG (orange line).

According to Figure 1, from 2017 to 2022, SVB grew from a $50 billion bank to a $212 billion bank. Thus, for more than a year after EGRRCPA became law, SVB’s assets fell within the $50 and $100 billion range and, as such, the bank was exempt from most enhanced regulation. Then, thanks to extraordinary growth in tech-sector initial public offerings, acquisitions, and other such fund-raising efforts, SVB’s deposits, whose owners disproportionately represented the tech sector, grew extraordinarily as well. From a regulatory perspective, SVB rather suddenly became an institution subject to enhanced regulation at the discretion of the Federal Reserve System.

According to the central bank’s own investigation, the central bank did not prudently exercise this discretion. To understand why, consider that the Federal Reserve organizes its supervisory practices according to bank asset size: aside from globally systemically important banks, which the central bank supervises in very bespoke ways, banks with assets valued at $100 billion or more are supervised within the central bank’s Large and Foreign Banking Organization (LFBO); banks with assets valued between $10 and $100 billion are supervised within the central bank’s Regional Banking Organization (RBO); and banks with assets valued at $10 billion or less are supervised within the central bank’s Community Banking Organization (CBO). Because of the speed with which SVB grew into a bank warranting LFBO supervision, as a practical matter, until February 2021, SVBFG was supervised within the RBO and, “examination staffing generally came from pools of RBO and CBO examiners, who may have had less experience with the governance and risk-management practices required for a more sizable and complex institution like SVBFG” (Review 2023, 5). In February 2021, SVBFG transitioned to LFBO supervision; nevertheless, “the regulations provided for a long transition period, or runway, for SVBFG to meet those higher standards [associated with LFBO]” (Review 2023, 8).

And then there is the matter of regulatory culture. In the decade after the Dodd-Frank Act passed into law on July 21, 2010, many lawmakers, some regulators, and others who operated in the financial industry or otherwise depended on intermediated credit sought to ease the act’s regulatory burden on banks in general and community banks in particular. EGRRCPA stands out as the most intentional and comprehensive effort in this regard. According to the authors of the report, this shift in regulatory preferences—less burden instead of more burden—instilled a sense among supervisory staff that they should be mindful of, and perhaps even prioritize reducing, the regulatory burden they impose on banks. In this way, an intellectual norm or mindset within the supervision and regulation circles shifted. According to the report:

In the interviews for this report, staff repeatedly mentioned changes in expectations and practices, including pressure to reduce burden on firms, meet a higher burden of proof for a supervisory conclusion, and demonstrate due process when considering supervisory actions. There was no formal or specific policy that required this, but staff felt a shift in culture and expectations from internal discussions and observed behavior that changed how supervision was executed. As a result, staff approached supervisory messages, particularly supervisory findings and enforcement actions, with a need to accumulate more evidence than in the past, which contributed to delays and, in some cases, led staff not to take action.

Review (2023, 36)

That this cultural shift contributed to the demise of SVB is an unprovable, counterfactual proposition, of course. Nevertheless, the authors of the report reason the shift likely played some unmeasurable role.

Finally, the academic literature offers some indirect evidence that EGRRCPA provided banks some regulatory relief, for better or worse. For example, Le and Santos (2023) conclude the effect of the act on non-interest expense is significant and negative: for the industry as a whole, the implementation of EGRRCPA decreases non-interest expense by roughly $23.6 billion annually, about one third the non-interest expense the Dodd-Frank Act imposed; conditional on bank size, the effect of EGRRCPA on non-interest expense is significant and negative for mid-sized community banks only. And quite interestingly, the effect of EGRRCPA on return on assets—a measure of profitability—is positive and significant for all except the smallest banks. For example, for mid-sized community banks, the implementation of EGRRCPA increases return on assets by roughly 23 basis points annually. Moreover, this relief rises with bank size: for relatively large community banks, the relief rises to roughly 48 basis points annually; and for the largest banks, the relief rises to roughly 85 basis points annually.

Of course, one way to generate profit in banking is to widen net interest margin as much and for as long as possible. Thus, the investigation’s finding that supervisors at the Federal Reserve imprudently allowed SVB to borrow short (at relatively low interest rates) and lend long (at relatively high interest rates) for too long after EGRRCPA was passed is broadly consistent with the increase in returns on assets that Le and Santos (2023) find for the U.S. banking system more generally.

In any case, the Federal Reserve’s internal investigation clearly identifies shortcomings in the central bank’s policies and processes around enhanced prudential regulation, which, in fairness to the central bank, is inherently difficult to execute. After all, banks specialize in the acquisition and analysis of (proprietary) information. No one, not even regulators, know a bank as well as a bank knows itself. To be sure, this informational asymmetry is the bank’s competitive advantage from which it generates profit, its raison d’etre. Meanwhile, regulatory burden is real; a bank’s cost of complying with regulations is not trivial. Thus, the challenge for bank regulators is to balance the benefits to the economy as a whole of prudential regulation with its costs. The central bank’s unvarnished internal investigation into the collapse of SVB is a necessary first step to striking this balance in the future.

References

Le, Hoanh and Joseph M. Santos. 2023. “To Dodd-Frank and Back: Regulatory Burden and the Economic Growth, Regulatory Relief, and Consumer Protection Act.” The American Economist, forthcoming. https://doi.org/10.1177/05694345221148210