This blog post accompanies the SDPB Monday Macro segment that airs on Monday, December 6, 2021. Click here to listen to the segment, which begins at minute 22:20 into the broadcast. Please note, a technical difficulty interrupted the latter part of the segment.

We have a chairman!

On Monday, November 22, 2021, U.S. President Joe Biden announced he would nominate Jerome (Jay) Powell to a second term as chair of the Board of Governors of the Federal Reserve System. Additionally, the president announced he would nominate Governor Lael Brainard to a term as vice chair of the board. In the weeks leading up to these announcements, financial markets viewed Jay Powell, a Republican, and Lael Brainard, a Democrat, as leading contenders for the chair position. And, because most observers reason that Powell and Brainard hold very similar views on the appropriate stance of U.S. monetary policy, financial markets thought—and, likely, fretted—that if the president, a Democrat, had nominated Lael Brainard and, thus, unseated Jay Powell as chair, the nomination could politicize—further?—U.S. monetary policy. This is to say in a rather oversimplified way, the optics of a Democratic president replacing the Republican chair with his Democratic equivalent could seem politically motivated or, at the very least, highly irregular.

Since 1936, the start of the modern era of Federal Reserve governance, a U.S. president chose not to appoint a sitting and eligible chair—governors serve nonrenewable fourteen-year terms—in only three instances. In Table 1, in which I list Federal Reserve chairs and the presidents who appointed them, I indicate in italicized, blue font these three instances; the most recent occurred three years ago, when then-President Donald Trump, a Republican, appointed Jay Powell and thus, unseated Janet Yellen, a Democrat.

Table 1: Federal Reserve Chairs and Appointing U.S. Presidents

| Term | Chair | President |

|---|---|---|

| 1936 – 1940 | Marriner Eccles (R) | Franklin Roosevelt (D) |

| 1940 – 1944 | Marriner Eccles (R) | Franklin Roosevelt (D) |

| 1944 – 1948 | Marriner Eccles (R) | Franklin Roosevelt (D) |

| 1948 – 1951 | Thomas McGabe (R) | Harry Truman (D) |

| 1951 – 1954 | William M. Martin Jr. (D) | Harry Truman (D) |

| 1954 – 1958 | William M. Martin Jr. (D) | Dwight Eisenhower (R) |

| 1958 – 1962 | William M. Martin Jr. (D) | Dwight Eisenhower (R) |

| 1962 – 1966 | William M. Martin Jr. (D) | John Kennedy (D) |

| 1966 – 1970 | William M. Martin Jr. (D) | Lyndon Johnson (D) |

| 1970 – 1974 | Arthur Burns (R) | Richard Nixon (R) |

| 1974 – 1978 | Arthur Burns (R) | Richard Nixon (R) |

| 1978 – 1979 | G. William Miller (D) | Jimmy Carter (D) |

| 1979 – 1983 | Paul Volcker (D) | Jimmy Carter (D) |

| 1983 – 1987 | Paul Volcker (D) | Ronald Reagan (R) |

| 1987 – 1990 | Alan Greenspan (R) | Ronald Reagan (R) |

| 1990 – 1994 | Alan Greenspan (R) | George H. W. Bush (R) |

| 1994 – 1998 | Alan Greenspan (R) | Bill Clinton (D) |

| 1998 – 2002 | Alan Greenspan (R) | Bill Clinton (D) |

| 2002 – 2006 | Alan Greenspan (R) | George W. Bush (R) |

| 2006 – 2010 | Ben Bernanke (R) | George W. Bush (R) |

| 2010 – 2014 | Ben Bernanke (R) | Barack Obama (D) |

| 2014 – 2018 | Janet Yellen (D) | Barack Obama (D) |

| 2018 – 2022 | Jerome Powell (R) | Donald Trump (R) |

| 2022 – | Jerome Powell (R) | Joe Biden (D) |

Political forces make for time-inconsistent monetary policy.

Macroeconomists fret about politicizing monetary policy because most reason that the primary goal of monetary policy should be low and stable inflation—think, around two percent annually. And to maintain low and stable inflation, the central bank’s commitment to doing so must be credible. In the parlance of macroeconomic—and, specifically, monetary—theory, the plan to maintain low and stable inflation must be time consistent: the plan must be one the central bank will follow. Macroeconomists reason that because politicizing monetary policy introduces conflicts of interest to the policy-making process—and these conflicts could cause policy makers to deviate from their otherwise-time-consistent plans—politicizing monetary policy renders it time inconsistent.

Time-inconsistent monetary policy is a problem because if we determine that policy makers will not follow their (time-inconsistent) plans, neither will we: if we determine the central bank will succumb to political pressures to allow high and variable inflation, we will demand and contract for higher wages, rents, interest payments, and profits, for example. By doing so, we potentially drive high and variable inflation—a self-fulfilling prophecy of a most-inconvenient sort for the central bank and everyone who prefers a stable purchasing power of money. A troubling example of politically motivated time-inconsistent monetary policy is currently on display in Turkey.

The macroeconomic reason why a central bank might be motivated, politically or otherwise, to deviate from its plan is that, in the short run, a primary goal of low and stable inflation could conflict with other arguably reasonable macroeconomic goals, such as full employment or sustained economic growth: in effect, maintaining price stability could mean surrendering jobs in the short run, for example. This policy tension between price stability and output or employment is greatest when the central bank endeavors to offset the effects of aggregate-supply (as opposed to aggregate-demand) shocks—think, pandemic-induced supply-chain disruptions, for example.

Aggregate-supply shocks move inflation and output in opposite directions—prices rise [fall] while output and employment fall [rise]. Because monetary policy operates through aggregate demand, aggregate-supply shocks impose a monetary-policy trade-off: minimize either inflation or output/employment variability, but not both. In this case, the opportunity cost of reducing inflation [output] variability is increasing output [inflation] variability; to control one, the central bank surrenders control of the other. Monetary theory implies that a time-consistent monetary policy minimizes this opportunity cost. Practically speaking, a time-consistent monetary policy could return output and employment to pre-pandemic levels, while rendering the concomitant rise in inflation transitory—sound familiar? (For more on monetary policy in the context of aggregate demand and aggregate supply, see Monday Macro segment, Three Wishes.)

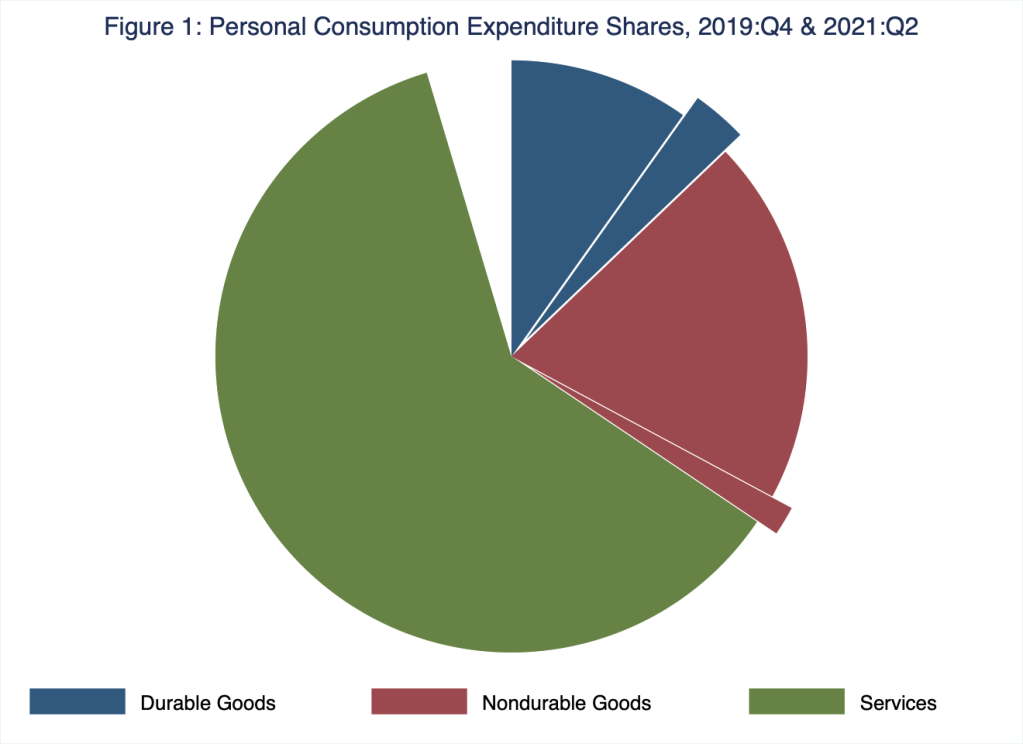

Today, this issue of whether Federal Reserve policy is time consistent is highly relevant, because the macroeconomic challenges the central bank confronts are aggregate-supply-shock induced. This pattern is evident, if only indirectly, in Figure 1, in which I compare the personal consumption expenditure shares of U.S. GDP in the fourth quarter of 2019 to those shares in the second quarter of 2021; consumption expenditures comprise over two thirds of U.S. GDP.

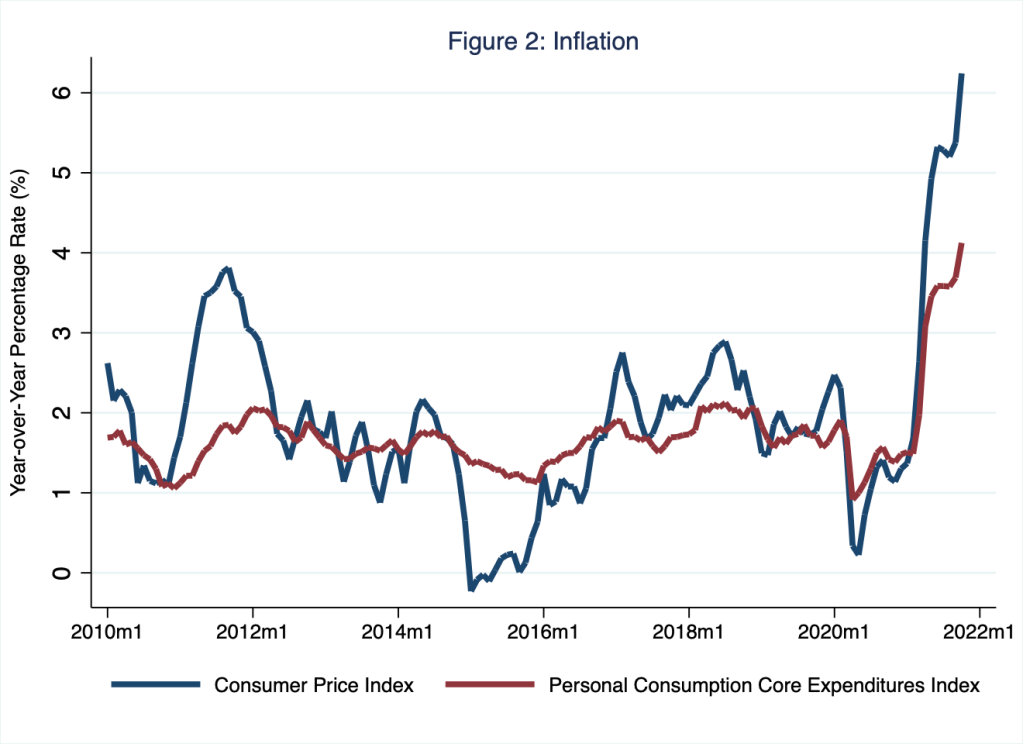

According to Figure 1, in a matter of a few months after the pandemic struck the United States, the services share of consumption expenditures contracted (by the area of the white-space void in the pie chart) and, consequently, the durable goods and non-durable goods shares of consumption expenditures expanded (by the areas of the offset blue and red wedges, respectively). Put differently, a few months after the pandemic struck the United States, consumers decreased their expenditures on services such as haircuts and, instead, increased their expenditures on durable goods such as couches and non-durable goods such as toilet tissue. This sudden shift in consumer preferences would have strained supply chains in the best of times; amid a pandemic, the outcome effectively amounted to an aggregate-supply shock (to durable and non-durable goods). And, correspondingly, aggregate-supply driven inflationary pressures, the greatest macroeconomic challenge the U.S. economy—and, thus, its central bank—confronts now. In Figure 2, I illustrate these inflationary pressures according to two broad measures: the consumer price index (CPI) and the personal consumption expenditures (PCE) index; the Federal Reserve prefers the latter measure of the rate of inflation.

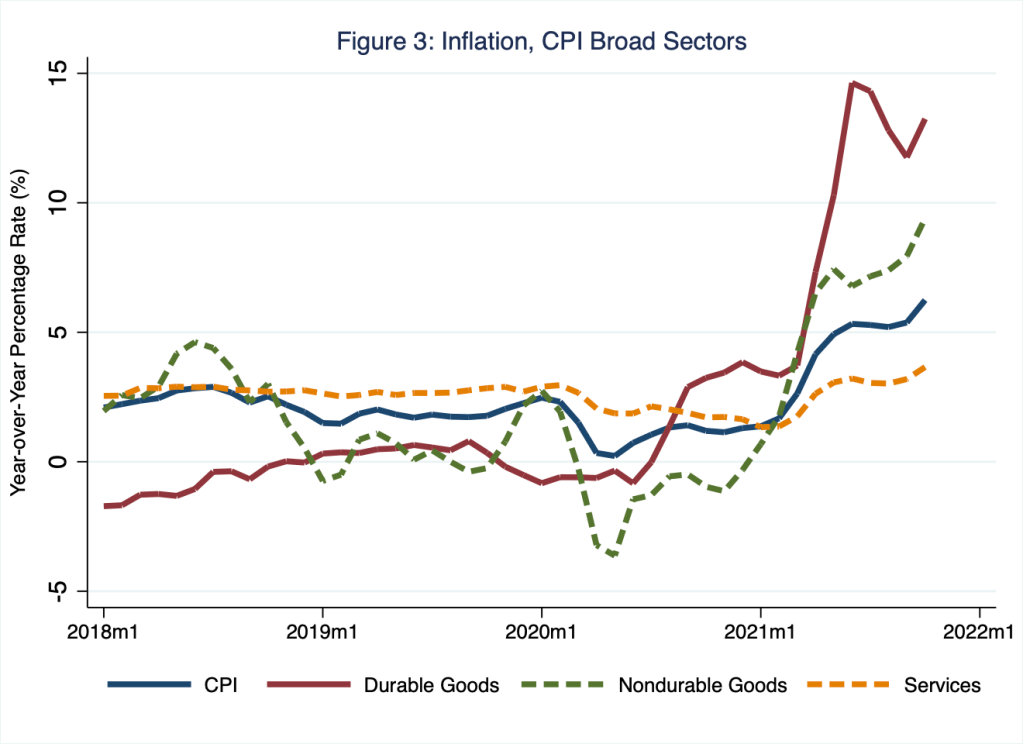

According to Figure 2, as of late, rates of inflation have landed well outside and above the central bank’s—or anyone else’s—comfort zone. As of October 2021, CPI inflation registered 6.24 percent, while PCE inflation registered 4.12 percent. In contrast, the Federal Reserve prefers a sustained annual rate of inflation around 2 percent. Moreover, as I illustrate in Figure 3 in the context of the CPI, the greatest inflationary pressures correspond to goods sectors, as opposed to service sectors, of the U.S. economy.

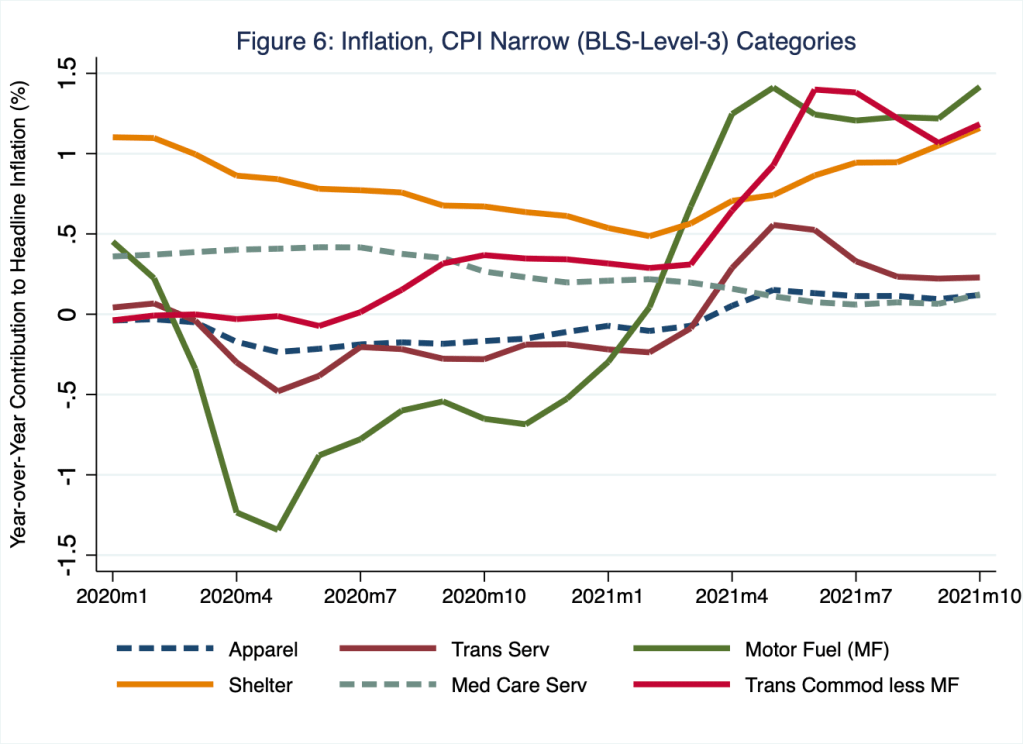

Indeed, more granularly, the greatest inflationary pressures at the moment correspond to those sectors most conspicuously constrained by supply-chain disruptions: essentially, automobiles, fuel, and shelter. These patterns are evident in Figure 4, in which I illustrate the contributions to headline annual CPI inflation of select sector categories. Inflationary pressures in transportation commodities excluding motor fuel (a category that includes automobiles), motor fuel, and shelter have far outpaced those in apparel and medical-care services, for example.

Of course, the same aggregate-supply shocks that induced these inflationary pressures also disrupted and, for a time, reduced output and employment. The Federal Reserve—and, to an exceptional degree, the Congress—have maintained expansionary policies to stimulate output and employment, effectively increasing aggregate demand. Put another way, the Federal Reserve temporarily deemphasized its inflation goal to emphasize its output goal, a short-term trade-off entirely consistent with best practices in monetary theory, so long as the central bank enjoys credibility, so that its deviation—which it intends to be temporary—from its objective of low and stable inflation does not stoke (a self-fulfilling prophecy of) permanently higher inflation.

Why isn’t the Federal Reserve more politically resilient?

To some extent, a central bank’s framework for monetary policy and the political forces to which that policy exposes the central bank tend to be path dependent; the Federal Reserve System is no exception in this regard: its early history and evolution explains quite a bit about its current monetary-policy framework.

In one respect, the question of why the Federal Reserve is not more politically resilient is ironic: the central bank was born of political compromise. The reasons for establishing this quasi-public institution—a federal agency owned by its member commercial banks—are complicated. Proponents sought a central monetary authority that could accommodate seasonal demands for currency and prevent or stem financial crises. In this way, the institution would “furnish an elastic currency” and serve as lender of last resort (Friedman and Schwartz 1963, 189). The Federal Reserve Act, which Congress passed in December 1913, did not include a “broad statement of purpose or policy objective” (Meltzer 2003, 65). Nowhere in the act did Congress mention price stability—or, more practically, low and stable inflation—as a primary goal of monetary policy. To be sure, at the founding of the Federal Reserve, “[t]he effects of money on prices were not unknown to Congress” (Meltzer 2003, 72). However, in 1913, the United States held to the gold standard. As such, the framework for monetary policy was to observe the so-called rules of the game: the central bank allowed changes in the money supply to reflect changes in gold flows, thus rendering monetary policy non-discretionary and passive. Price stability was a consequence rather than a goal of gold-standard-era monetary policy (Meltzer 2003, 125).

By the passage of the Bank Act of 1935, during the Great Depression, Congress had restructured the Federal Reserve System into a true central bank, complete with a powerful (relative to the system of twelve independent regional reserve banks) and potentially more-independent seven-member board of governors, then chaired by Mariner Eccles (Table 1). Still, the act did not identify a framework for monetary policy, which remained largely tethered to the Treasury’s debt-serving needs until after World War II, during which the central bank bought or sold government bonds to cap the cost to the Treasury of financing the war effort. Finally, a mandate, though not an explicit framework, for monetary policy emerged in 1977, when Congress amended the Federal Reserve Act to instruct the central bank to “promote effectively the goals of maximum employment, stable prices, and moderate long term interest rates” (Meltzer 2009, 986). This so-called dual mandate—maximum employment and stable prices—informs Federal Reserve monetary policy to this day. Though, since 1977, the Federal Reserve has done what it could do to sharpen its focus on—if not its legislative mandate to achieve—price stability.

On January 29, 2012, the central bank’s Federal Open Market Committee released independently of Congress a “Statement on Long-Run Goals and Monetary Policy Strategy,” in which the central bank identified a single numerical inflation-target value of 2 percent based on the personal consumption core expenditures (PCE) price index (Figure 2). This objective, which the central bank amended somewhat in the midst of the pandemic, is sufficiently flexible so as to be consistent with the dual mandate. And that, some monetary economists might argue, is the problem: because, in principle, the Federal Reserve’s dual mandate affords the central bank the flexibility to, say, emphasize interminably the employment portion of the mandate at the cost of deemphasizing the price-stability portion of the mandate, the dual-mandate leaves the central bank vulnerable to politicization and, thus, the time-inconsistency trap.

As Sarah Binder and Mark Spindel (2017) write in, In The Myth of Independence, the Fed has never been independent from politics. Though Congress and, to a far lesser extent, the central bank has intermittently increased the central bank’s authority, the legislature has long asserted its ultimate control of the Federal Reserve and, thus, U.S. monetary policy. And so the inflationary threats posed by time inconsistent monetary policy remain—at a time when we could least afford them.

References

Binder, Sarah and Mark Spindel. 2017. The Myth of Independence: How Congress Governs the Federal Reserve (Princeton: Princeton University Press)

Friedman, M. and Anna J. Schwartz. 1963. A Monetary History of the United States, 1867-1960 (Princeton, New Jersey: Princeton University Press)

Meltzer, Allan H. 2003. A History of the Federal Reserve, Volume 1: 1913 – 1951 (Chicago: The University of Chicago Press)

Meltzer, Allan H. 2009. A History of the Federal Reserve, Volume 2, Book 2: 1970 – 1986 (Chicago: The University of Chicago Press)

One thought on “habemus praefectus!”