This blog post accompanies the SDPB Monday Macro segment that airs on Monday, November 1, 2021. Click here to listen to the segment, which begins at minute 21:00 into the broadcast.

Most central banks make one or two wishes: maintain low inflation or maintain low inflation and maintain low unemployment. For example, in the case of the U.S Federal Reserve System, the (de jure) goals of monetary policy—since a 1977 amendment to the Federal Reserve Act—are to achieve a dual Congressional mandate of stable prices (or, practically speaking, low inflation) and maximum employment (or, put differently, low unemployment). In any case, increasingly, central banks and their observers are making—or, at the very least, thinking about making—a third wish: reduce income and/or wealth inequality. For example, on August 27, 2020, when the Federal Reserve amended its Statement on Long-Run Goals and Monetary Policy Strategy, the central bank explicitly recognized:

“The role of monetary policy is to support a strong, stable economy that benefits all Americans. The characterization of our maximum employment goal as broad-based and inclusive clarifies that the Federal Reserve seeks to foster economic conditions that benefit everyone. It also stresses the importance of understanding how various communities are experiencing the labor market when assessing the degree to which employment in the economy as a whole is falling short of its maximum level.”

In a related way, earlier this year, the Economist magazine identified the pandemic as a source of worldwide widening of wealth gaps, which widened as interest rates fell and the value of publicly traded companies rose, and asked whether central banks were to blame. To be sure, the Banco Central De La República Argentina explicitly identifies social equality (along with economic development) as an “ultimate objective.”

Attending explicitly to matters of income or wealth inequality is largely uncharted territory for most central banks, including the Federal Reserve. This is because conventional monetary policy effectively homogenizes otherwise deeper, heterogeneous features of the economy. For example, inflation is a fall in the purchasing power of money, independent of the goods and services money buys or who holds, lends, or borrows money (and, thus, who buys the goods and services). Likewise, the unemployment rate is a broad measure of labor utilization and, by association, economic output, independent of how jobs and the levels of income earned from producing economic output are distributed across heterogeneous individuals (who differ, in part, according to the income they earn or the wealth they own, for example). All this is not to say macroeconomic theory is indifferent to heterogeneity; on the contrary, macroeconomists are increasingly writing models rich with variation across individuals, households, firms, and countries. Nevertheless, monetary policy has traditionally focused, for the most part, on the economy’s general features, independent of (micro) economic heterogeneity.

How might an economist quantify inequality?

Before addressing the role monetary policy could or should play in addressing inequality, I begin by broadly characterizing it, and I focus on income inequality. My objective is not to make the case that inequality exists—it does—but rather to offer a sense of how economists might quantify it for the purpose of exposition. To be sure, the distributions of income (a flow earned over some interval of time) and wealth (a stock accumulation of assets minus debts owned at a moment in time) are unequal in the United States. Characterizing the extent of inequality in an economy is not easy, in part because many ways of interpreting and empirically measuring inequality exist. One relatively familiar characterization is based on income—as opposed to, say, wealth—and derives from the Lorenz curve, which I illustrate in Figure 1.

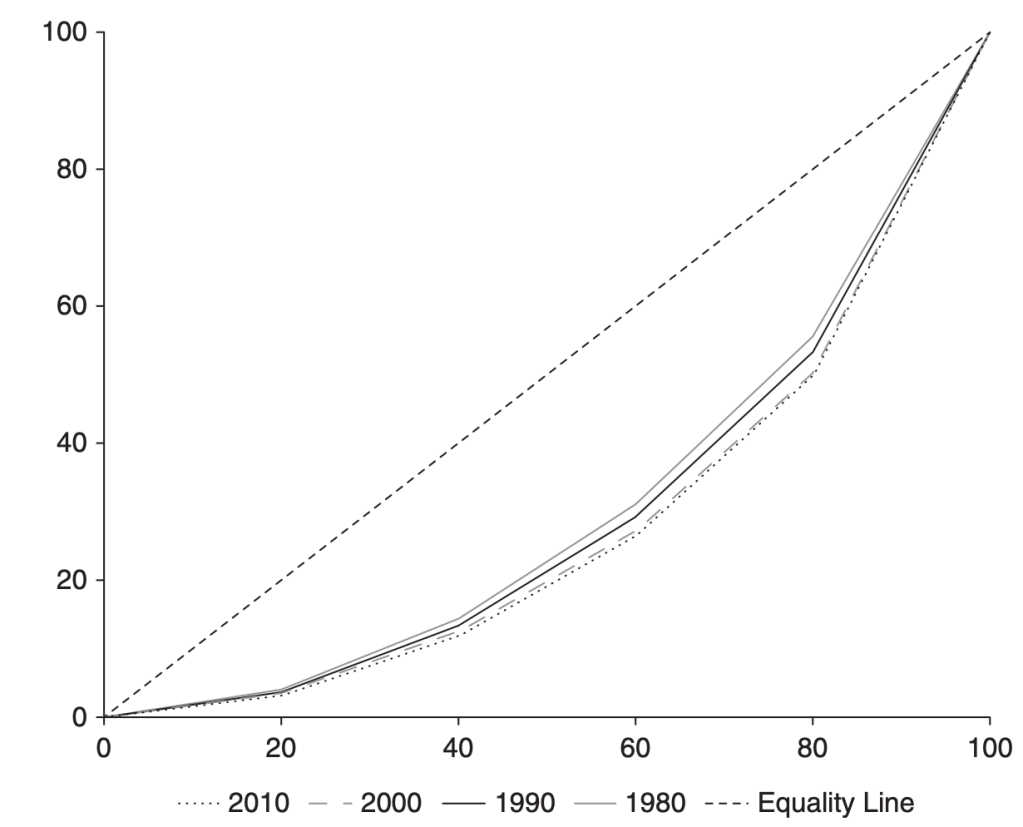

Figure 1: Lorenz Curve, United States Households, 1980 to 2010

In Figure 1, the horizontal axis measures, for a given decade, fractiles of the United States population sorted from the lowest income earner (at 0 on the leftmost side of the axis) to the highest income earner (at 100 on the rightmost side of the axis); the vertical axis measures cumulative shares of total income earned by some corresponding fractile of the population. The interpretation of the curve will be familiar to most readers; consider, for example, the 40th fractile along the horizontal axis. In this example, the vertical-axis value corresponding to the 40th fractile is the cumulative share of total income earned by the first 40 percent of the population (ranked by income); according to Figure 1, this cumulative share registered about 10 percent in 2010. On the so-called equality line, the cumulative share of total income earned by the first 40 percent of the population is 40 percent; if this pattern holds for all fractiles, the distribution of income is equal according to this characterization. The equality line is a baseline, of course. Actual Lorenz curves bow away from the equality line. The more a Lorenz curve bows away from the equality line, the more unequal the income distribution. Thus, according to Figure 1, the unequal distribution of income in the United States has grown more unequal over time.

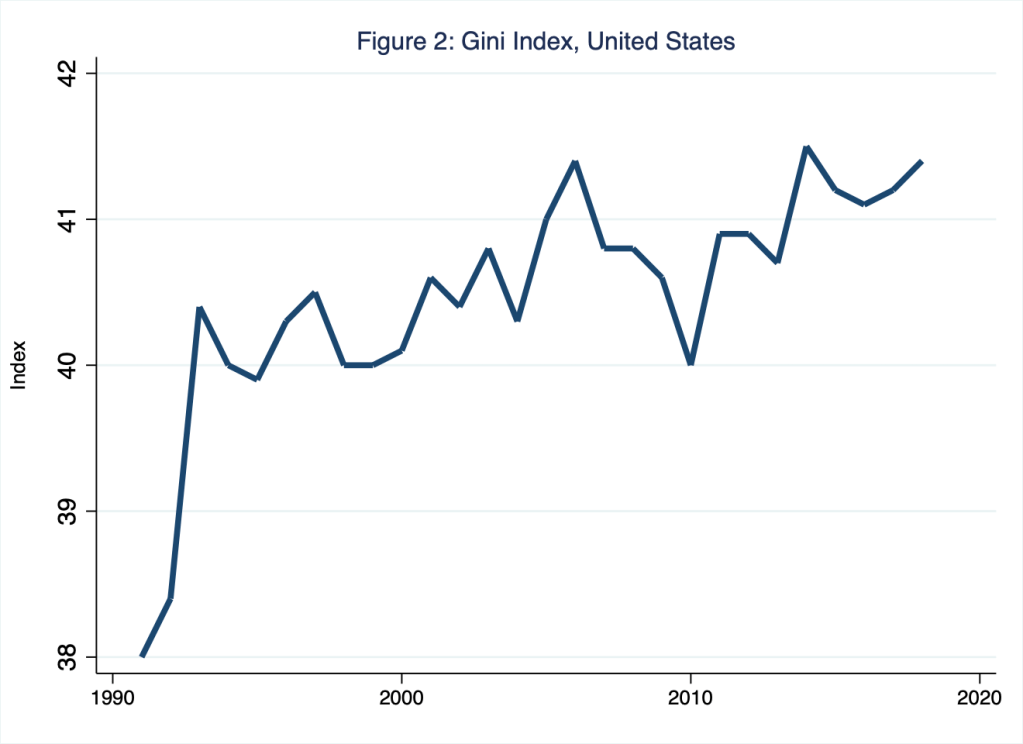

More specifically, if the distribution of income is perfectly equal, the area between the equality line and the Lorenz curve is zero (because in this case the equality line and the Lorenz curve are identical). Likewise, if the distribution of income is absolutely unequal, the area between the equality line and the Lorenz curve—in this case, a lower triangle in Figure 1—is one half the area of the entire x-y-coordinate plane illustrated in Figure 1. Thus, based on the Lorenz curve, the distribution of income varies from absolute equality (a surface area of 0) to absolute inequality (a surface area of 0.5). Based on the Lorenz curve, one way to quantify empirically the extent of income inequality in an economy is with a single summary statistic called the Gini index, which equals twice the area between the equality line and the Lorenz curve in the style of Figure 1. Thus, the Gini index—or, often, Gini coefficient—varies from 0 (2 x 0 surface area; absolute equality) to 1 (2 x 0.5 surface area; absolute inequality). In Figure 2, I illustrate the Gini index for the annual distributions of income earned in the United States from 1991 to 2018, the latest year for which such data in this series are available for the United States.

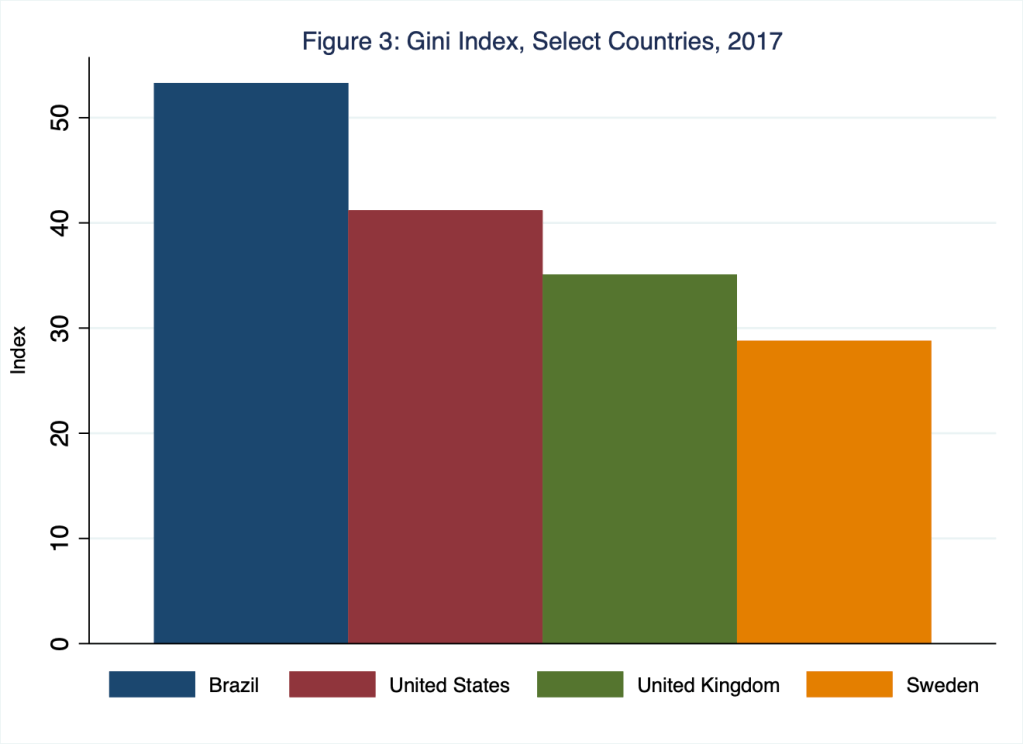

According to Figure 2, the distribution of income earned in the United States has generally grown more unequal over time. In 2018, the Gini index registered 41.4, or roughly 9 percent more than the value of 38 that the index registered in 1992. To gain a sense of what these Gini index values imply about the extent of income inequality in the United States, in Figure 3 I illustrate Gini index values for the United States along with three other countries: Brazil, the United Kingdom, and Sweden; 2017 is the latest year for which data in this series are available for all four countries.

According to Figure 3, the distribution of income in the United States (41.2) is unequal relative to the distributions in the United Kingdom (35.1) and Sweden (28.8). Those who advocate economic policies designed to reduce inequality in the United States prefer the distribution of income be shaped more like that of Sweden than Brazil.

What do central banks do if not worry about inequality?

A central bank implements monetary policy to make its wish(es) come true. Monetary policy is a type of economic policy that we intend to shape the economy’s general (macroeconomic) features, including, among others, inflation and unemployment. Generally speaking, economic policy consists of allocation policy, redistribution policy, and stabilization policy. These policies and their outcomes—intended or otherwise—are, at times, interrelated, of course. But, strictly speaking, allocation policy shapes (long-run) features of economic growth and labor productivity; redistribution policy reshapes the (extant) distribution of income and wealth across households; and, stabilization policy shapes the (short-run) features of the business cycle, those irregular fluctuations in aggregate economic activity—expansions and recessions, for example—we closely associate with inflation and unemployment. Conventional monetary policy is stabilization policy.

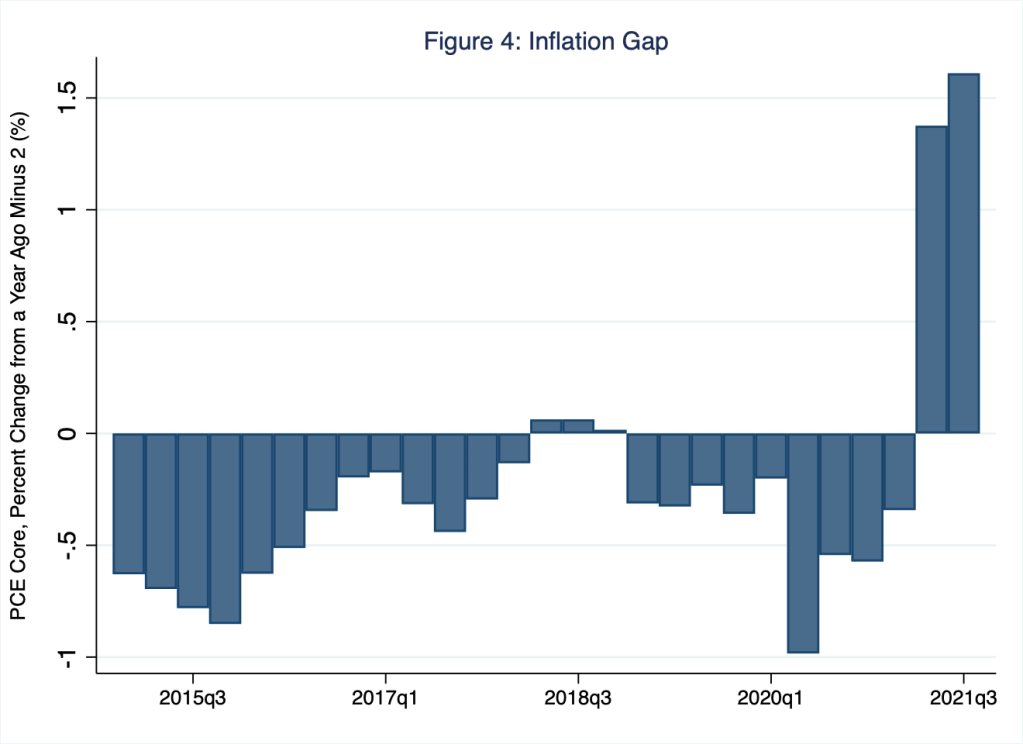

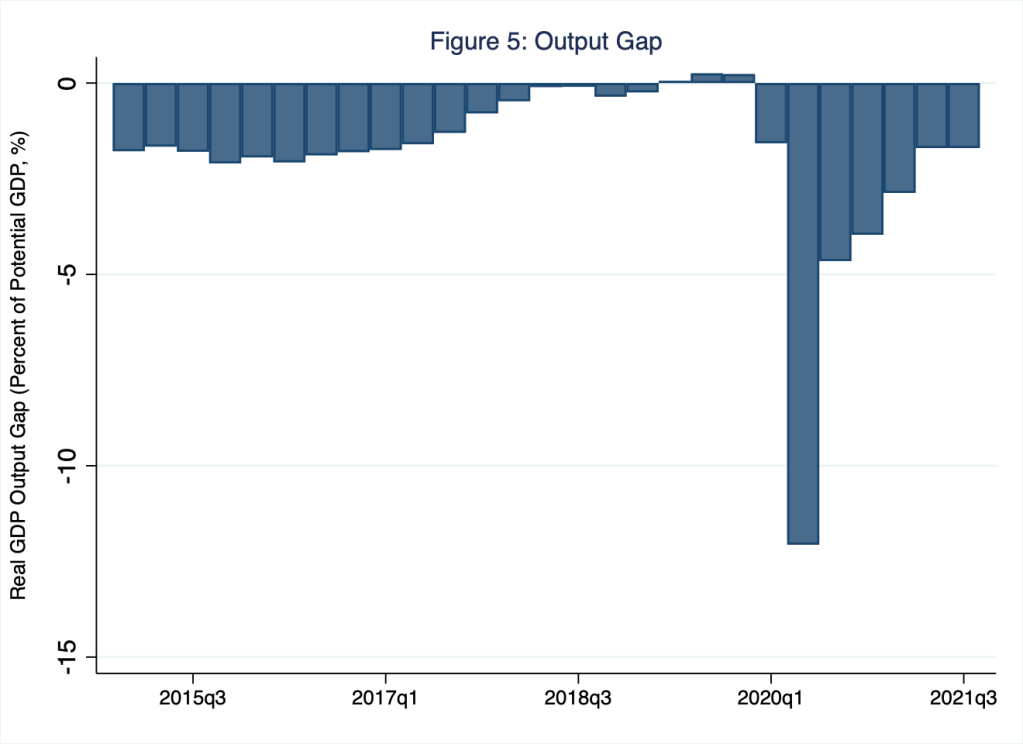

In the case of the Federal Reserve System, the goals—aka, wishes—of monetary policy are essentially to minimize the inflation and output gaps. (For more on these gaps, see Monday Macro segment, Mind the Gaps.) Briefly, the inflation gap is the difference between the actual inflation rate and the target inflation rate—of about 2 percent on average in the case of the Federal Reserve, for example. The output gap is the difference between actual output and potential output—the level of output the economy would achieve if it were operating at full capacity. Minimizing the output gap is closely aligned with maximizing employment, one piece of the Federal Reserve’s dual mandate. In Figures 4 and 5, I illustrate the inflation and output gaps for the United States.

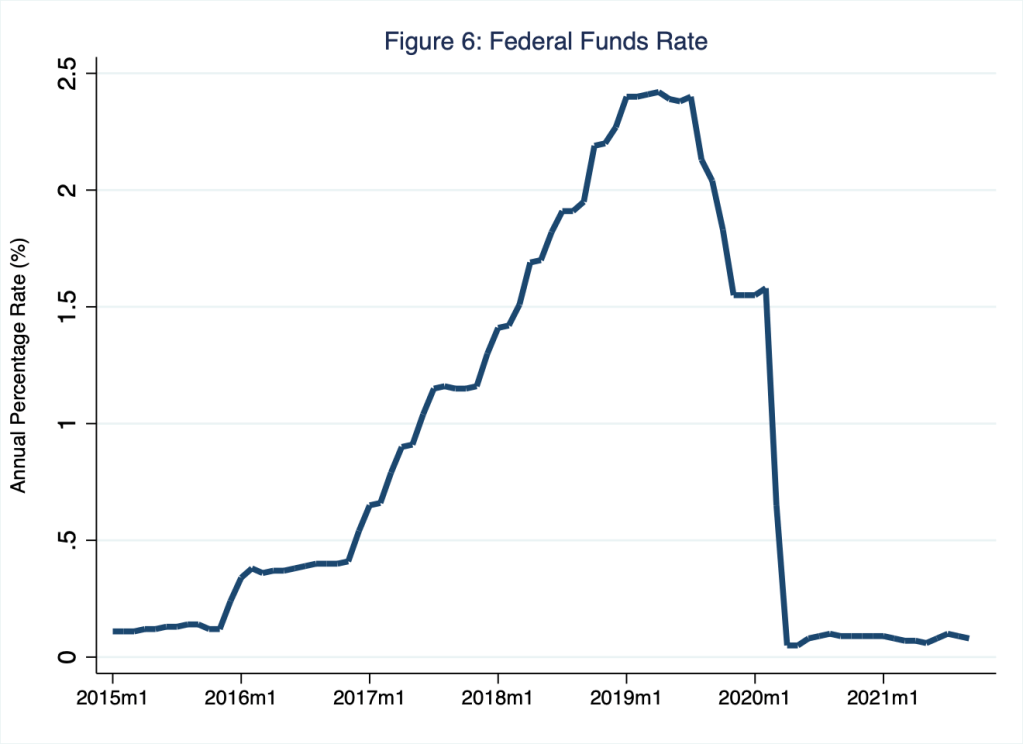

According to Figure 4, currently the inflation gap is positive; meanwhile, according to Figure 5, the output gap is negative. In any case, to achieve these goals, the Federal Reserve, like most central banks, has a single tool, or instrument in the parlance of economic policy. For the Federal Reserve, the primary instrument of conventional monetary policy is the federal funds rate, an interbank rate banks charge each other for bank reserves—inventories, essentially, that banks manage in order to generate earnings (by lending reserves to borrowers) and to maintain liquidity (by storing reserves for cash-seeking depositors). Think about this interbank market for reserves like a market for automobile parts: automobile-producing firms that have more [fewer] parts than they need, lend [borrow] the parts to [from] other automobile-producing firms. In Figure 6, I illustrate the federal funds rate.

A quick glance at Figures 4, 5, and 6 reveals the Federal Reserve’s approach to conventional monetary policy. The Federal Reserve targets the federal funds rate (Figure 6) in order to achieve the central bank’s dual Congressional mandate of stable prices (or, practically speaking, low inflation; Figure 4) and maximum employment (and, thus, maximum output; Figure 5). The Fed lowers [raises] its target for the federal funds rate when either the output gap or the inflation gap is negative [positive]. This is because a negative [positive] output gap reflects an economy that is operating below [above] its potential. Similarly, a negative [positive] inflation gap reflects an economy in which the average price level is rising too slowly [quickly] relative to the Fed’s target inflation rate. Currently, the inflation and output gaps are sending the Federal Reserve mixed signals: expand because the output gap is negative and contract because the inflation gap is positive. Central banking is no picnic. Thus far, the Federal Reserve has emphasized minimizing the output gap over minimizing the inflation gap. (For more on the Federal Reserve System, its Federal Open Market Committee [FOMC], and how the Fed’s trading desk manipulates the monetary base, at the direction of the FOMC, in order to keep the federal funds rate within the target range see the Morning Macro segment, “Fed Up.”)

Should central banks be dreaming of Gini?

Currently, the Federal Reserve has one instrument—the federal funds rate—to aim simultaneously at two targets—the inflation gap and the output gap. Making income equality—a Gini-index gap, say—a third goal of monetary policy would impose an additional constraint on the central bank’s policy problem; this is to say, the central bank would need to consider at once how the interest rate drives inflation (constraint #1), output (constraint #2), and income inequality (constraint #3). Here I assume such a third constraint exists and, thus, monetary policy affects inequality; this assumption may be false, but assume for now that it is true.

How monetary policy affects inequality is not clear. Consider, for concreteness, expansionary monetary policy, which, in theory, reduces interest rates, raises employment, and ultimately raises inflation. Relatively low interest rates could increase the values of publicly traded firms, thereby advantaging those individuals who own publicly traded stocks; such individuals tend to earn relatively high incomes and own relatively large amounts of wealth. Thus, in this instance, the expansionary monetary policy potentially increases inequality. Meanwhile, the same relatively low interest rates raise employment and, if the last decade-long expansion is any guide, ultimately reattach the most economically fragile individuals to gainful employment; such individuals tend to earn relatively low incomes and own relatively small amounts of wealth. Thus, in this instance, the expansionary monetary policy potentially decreases inequality. Moreover, the effects on inequality of inflation that expansionary monetary policy ultimately causes is ambiguous too: inflation tends to advantage borrowers and effectively tax lenders and individuals who hold cash; how these advantages and tax burdens fall across income and wealth distributions is not obvious. In a recent study, Coibion, et al. (2017) conclude, if anything, contractionary monetary policy seems to drive U.S. inequality. And then there is the intriguing possibility that inequality—and not expansionary monetary policy—reduces interest rates; in this case, monetary policy is simply along for the ride (Mian, et al. 2021).

Even if the effects of monetary policy on inequality were clear and economically substantial, the operational challenges of hitting yet another target with a single instrument would prove exceptionally difficult for a central bank. Meanwhile, the difficulty we would face interpreting how a single instrument drives three independent monetary policy goal variables would reduce the transparency, accountability, and, thus, credibility of monetary policy. And none of these trade offs would be worth making, not because inequality is unimportant but because we already have the tools to reduce it if we so wish. Redistribution policies, implemented with tax, transfer, and government-expenditure instruments—all three the domain of Congress and Treasury—are at the ready should we choose to use them accordingly.

References

Bénassy-Quéré, Agnès, Benoît Cœuré, Pierre Jacquet, and Jean Pisani-Ferry. 2018. Economic Policy: Theory and Practice. Oxford: Oxford University Press.

Coibion, Olivier, Yuriy Gorodnichenko, Lorenz Kueng, and John Silvia. 2017. “Innocent Bystanders? Monetary policy and inequality.” Journal of Monetary Economics, 88:70-89.

Mian, Atif, Ludwig Straub, and Amir Sufi. 2021. “What explains the decline in r*? Rising income inequality versus demographic shifts.” NBER Working Paper.

One thought on “three wishes”