![]() This blog post accompanies the SDPR Morning Macro segment that airs on Monday, March 25.

This blog post accompanies the SDPR Morning Macro segment that airs on Monday, March 25.

Several years ago, then-Governor of the Bank of England, Mervyn King, quipped that monetary policy should be boring. As it happens, making monetary policy boring is a lot tougher than we might think. In the last year or so, and indeed just last week, the Federal Reserve System, the institution responsible for implementing monetary policy in the United States, has attracted unwanted attention inside the Beltway. And while such attention is not entirely new, it is no less disconcerting. I will explain, after a bit of background.

The Federal Reserve System is the central bank—or, more precisely, the central-banking system—of the United States. The system is quasi-public—a federal agency owned by its member commercial banks. It includes the Board of Governors located in Washington D.C. and twelve regional Federal Reserve Banks, each assigned to a separate Federal Reserve district and located in a city within that district. For example, the Federal Reserve Bank of Minneapolis is assigned to the ninth Federal Reserve district, which, incidentally, includes South Dakota, home to Morning Macro and SDPR. (For an excellent, comprehensive primer on the structure of the Federal Reserve, visit its Board of Governors website.) The Federal Reserve System, to which we refer (affectionately or otherwise) as the Fed, began operations in November 1914; though, modern central banking, informed by a monetary-policy framework (around an inflation target of low and stable inflation, for example), clearly defined tactics, and relative independence from political forces—an independence most economists deem essential to sound monetary policy—emerged much later.

Like all modern central banks, the Fed influences the money supply and, thus, interest rates in order to achieve macroeconomic outcomes, including low and stable inflation, full employment, a resilient financial system, and an efficient payments system (of clearing checks, transferring financial-account balances, and so forth). In any case, the defining feature of a central bank is that it issues the economy’s monetary base—central-bank notes in circulation. In the case of the Fed, the monetary base consists of Federal Reserve notes circulating as either currency—dollar bills in the hands of the nonbank public—or bank reserves—cash in the physical or virtual vaults of banks. Thus, the United States monetary base is a liability of the Fed (and an asset to everyone else). A Federal Reserve note is an IOU issued by the Fed to whomever holds the note. In similar fashion, then, Japan’s (yen-denominated) monetary base is a liability of the Bank of Japan, the United Kingdom’s (sterling-denominated) monetary base is a liability of the Bank of England, and so on.

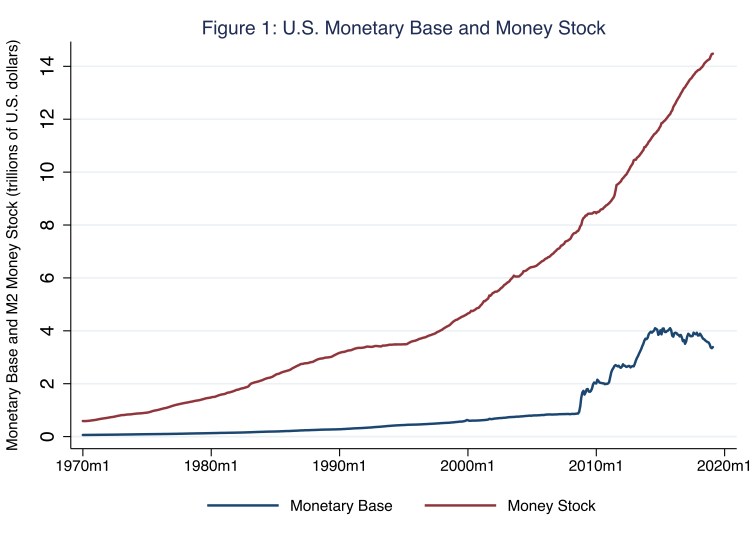

The Fed, like all central banks, directly controls its monetary base, but not the money supply. In the case of the Fed, the money supply consists of Federal Reserve notes circulating as currency—the currency portion of the monetary base—and checking-account deposits, both of which satisfy the definition of money: a generally accepted means of payment for goods, services, and debts. Because the sum of checking-account deposits depends on the collective interactions of the Fed (through its control of the monetary base and, thus, bank reserves), the nonbank public (through its use of the banking system and, thus, checking-account deposits), and the banking system (through its creation of loans and, thus, checking-account deposits), the Fed only indirectly influences the money supply. So, to summarize, the Fed, like all central banks, controls its monetary base—a monetary liability of the central bank and no one else—in order to influence the money supply and, thus, interest rates. In Figure 1, I illustrate the monetary base and the money supply, which, when measured at any moment in time, we refer to as the money stock.

In Figure 1, I measure the money stock as so-called M2, which mostly includes currency in circulation and liquid bank and other-intermediated deposits, all of which are generally accepted as a means of payment for goods, services, and debts—that is, money, by definition. Prior to the Great Recession, the monetary base grew at a reliably steady rate. During and after the Great Recession, the Fed increased the size of the monetary base to unprecedented levels (the subject of a future Morning Macro segment). For example, in 2007, just prior to the financial crisis, the monetary base measured about $850 billion (or about 6 percent of GDP); in 2014, it reached about $4 trillion (or about 23 percent of GDP); and currently, it measures about $3.4 trillion (or about 17 percent of GDP). Meanwhile, for the most part, the (M2) money stock has increased rather steadily. At any moment in time, the monetary base (β) and the money stock (M) are related according to a so-called money multiplier (μ) as follows.

Μ = μ × β

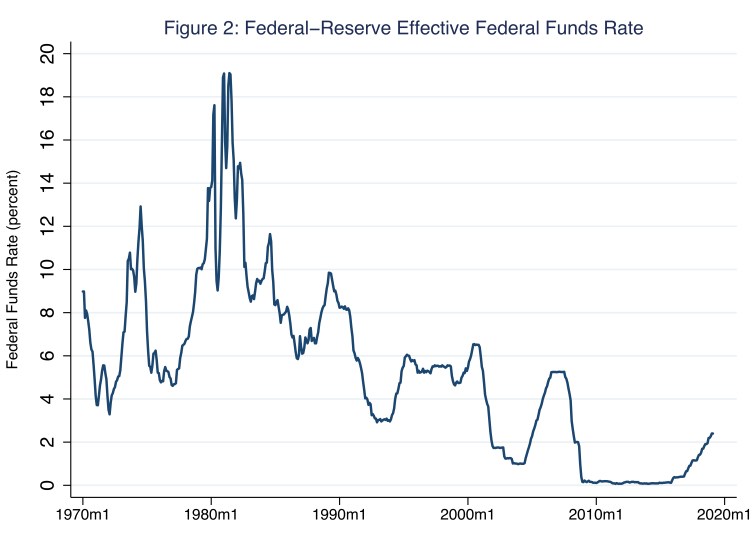

According to this relationship, the money stock (M) is some multiple (μ) of the monetary base (β), which the Fed controls. For example, in February 2019 the money stock (M) measured about $14.5 trillion while the monetary base (β) measured about $3.4 trillion, so the money stock was about 4.3 times larger than the monetary base; this is to say, the multiplier (μ) was about 4.3. Or, in terms of Figure 1, the red data point associated with February 2019 is about 4.3 times higher than the blue data point associated with the same date. Essentially, the multiplier is greater than one because of fractional-reserve banking: that is, colloquially speaking, banks lend other people’s money, multiplying the amount of claims—think, deposits—to a given amount of reserves. The Fed has four essential tools it uses to either control the monetary base or influence the money multiplier and, thus, the money stock. The effects of the Fed’s control and influence are reflected in the federal funds rate—the (interbank) rate that lending banks charge borrowing banks for bank reserves; in Figure 2, I illustrate this rate.

The federal funds rate, which now stands between a relatively low Fed-targeted range of 2.25 to 2.50 percent, is much talked about in the financial press, because the rate essentially tracks the Fed’s influence of the money stock and, thus, interest rates more generally. Notice, for example, how the federal funds rate fell dramatically to near zero around the start of the Great Recession when the monetary base (Figure 1) rose dramatically because of the concomitant increase in bank reserves. And, at the same time, as readers will no doubt recall, interest rates more generally fell as well. The Fed’s target for the federal funds rate is set by the Federal Open Market Committee (FOMC), which consists of the seven members of the Board of Governors and a rotating selection of five (of twelve) regional Federal Reserve Bank presidents.

Two tools the Fed uses to control the monetary base are open-market operations and the discount rate. Open-market operations are essentially purchases and sales of debt securities—U.S. Treasury bills, notes, and bonds, for the most part. (For more on the U.S. Treasury, which is distinct from the Federal Reserve System, see the Morning Macro segment, “Fiscal Therapy.”) As a practical matter, the Fed trades U.S. Treasury securities on the open (or secondary) market with banks, which hold these securities as investments or as inventory to trade with others. Suppose, for example, the Fed purchases a $100 Treasury bill from Bank A. In this example, the Fed receives a $100 Treasury bill, which adds to the Fed’s assets, and Bank A receives $100 of (newly created) bank reserves, which add to the Fed’s monetary liabilities and, thus, the monetary base. So, an open-market purchase increases the size of the monetary base; an open-market sale has the opposite effect. Looking again at Figures 1 and 2, the federal funds rate fell around the start of the Great Recession and the monetary base rose because the Fed purchased several trillions of dollars of debt securities.

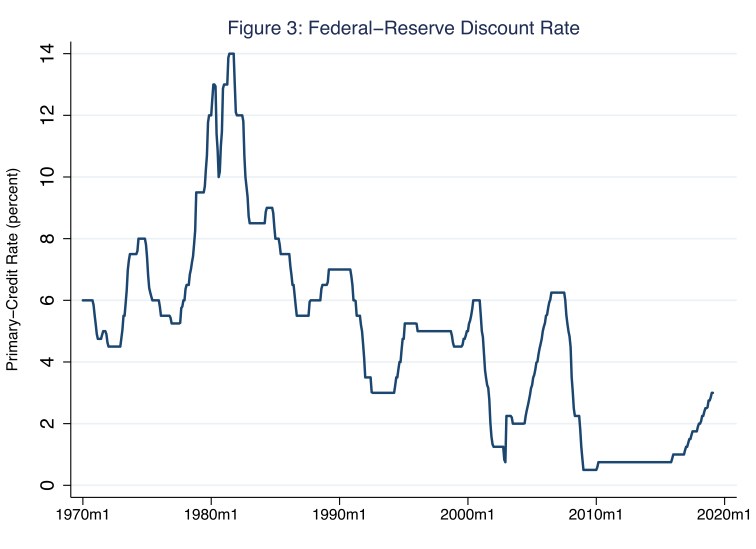

Meanwhile, the discount rate is the interest rate the Fed—and, more specifically, the regional Federal Reserve banks—charge depository institutions for mostly short-term loans, and mostly of a sort we call primary credit, which depository institutions access, in exchange for collateral the Fed deems eligible, via the metaphorical discount window. (It was not always a metaphor.) Discount lending is the oldest, most-important, and rarely used tool of the Fed. The discount window allows the central bank to serve as a lender of last resort—the fundamental raison d’être of any central bank. Functionally, discount lending increases the monetary base. Suppose, for example, the Fed lends $100 to Bank A. In this example, the Fed receives an IOU from Bank A, which adds to the Fed’s assets, and Bank A receives $100 of (newly created) bank reserves, which adds to the Fed’s monetary liabilities and, thus, the monetary base. In Figure 3, I illustrate the discount rate, which, unlike the federal funds rate, is a perfectly smooth step function, because the Fed administers—as opposed to targets—this rate.

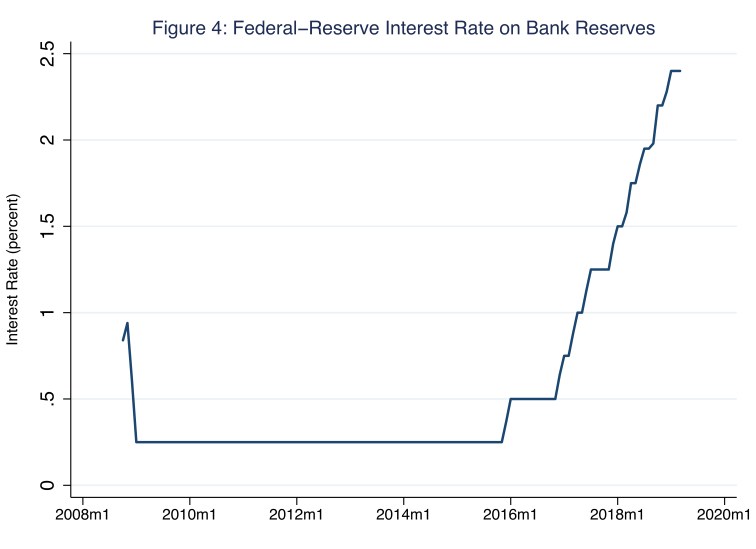

Two tools the Fed uses to influence the money multiplier are the required-reserve ratio and interest (the Fed pays) on reserves. The Fed requires each depository institution to hold a minimum amount of bank reserves for every dollar of the most-liquid deposits the institution holds. The Fed sets the required-reserve ratio in order to ensure the banking system is sufficiently liquid to withstand a bank run. The ratio also influences the amount of excess reserves—reserves institutions may lend at their discretion. All else equal, the greater the amount of excess reserves, the greater the potential multiplier and, thus, the money stock.

Meanwhile, the Fed pays depository institutions interest on their required and excess reserves. The interest rate paid on excess reserves shapes the incentives depository institutions have to lend excess reserves and, thus, effectively increase the money stock. For example, if the Fed raises this interest rate (as the central bank has done recently), then depository institutions have less incentive to lend reserves to, say, individuals or firms. Although loans to individuals or firms pay a higher interest rate than the Fed pays on reserves, loans expose depository institutions to default risk; in stark contrast, the Fed is a risk-free sure thing. The interest rate on reserves is the newest Fed tool, on which the Fed relies to manage the enormous quantity of excess reserves (Figure 1). In Figure 4, I illustrate the rate paid on excess reserves; the rates paid on excess and required reserves were equal during the sample period.

Throughout history, the relationship between the Fed and the legislative and executive branches of government has been, well, complicated. The Fed was fashioned by political compromise. The motivations for this institution varied widely. Its proponents shared the view that such a system could accommodate seasonal demands for currency and prevent the financial crises, common in the nineteenth century, that these demands precipitated from time to time (Miron 1996, 145-6). According to Binder and Spindel (2017), the Panic of 1907 revealed the limits of lender-of-last-resort governmental interventions absent a central bank; the authors describe these interventions as “precarious, primitive, partial, and probably illegal” (55). A central bank could “furnish an elastic currency” and, when necessary, serve as lender of last resort to the financial system and, in rare cases, the economy more generally (Friedman and Schwartz 1963, 189).

The Federal Reserve Act, which the United States Congress passed in December, 1913, omitted a “broad statement of purpose or policy objective” (Meltzer 2003, 65). No doubt, political support for the act demanded this lack of specificity. Nevertheless, that the act mentioned nothing about price stability as a framework for monetary policy had as much to do with the international monetary standard in place at the time (Meltzer 2003, 72). In 1913, the United States was on a gold standard, which required money stocks in participating countries to expand and contract along with gold inflows and outflows, respectively (Friedman and Schwartz 1963, 191). In principle, these flows balanced international payments and, in doing so, minimized otherwise-requisite persistent changes in national price levels (Bordo and Schwartz 1984, 24). Thus, the gold standard rendered monetary policy passive; price stability was, if anything, a desirable outcome rather than an objective of monetary policy (Meltzer 2003, 125; Timberlake 1993, 408).

The role of monetary policy in the United States changed amid the Great Depression, when the country left the gold standard in 1933 and, consequently, the standard collapsed shortly thereafter (Miron 1996, 153). In 1935, Congress passed the Banking Act, which transformed the Federal Reserve System into the true central bank we recognize today. The act equipped the system with a more-powerful and potentially more-independent seven-member board of governors (chaired by Mariner Eccles and headquartered in Washington, D.C.) And, the act gave the Fed greater latitude on its discount-window policy (Meltzer 2003, 485-86). In any case, Federal Reserve monetary policy remained tethered to the Treasury—and, thus, the executive branch of the federal government—until after World War II. This is because in April 1942, the central bank committed indefinitely to peg yields on government debt in order to cap the cost of financing the war effort (Meltzer 2003, 579).

A relatively independent monetary policy emerged in March 1951 with the so-called Treasury-Federal Reserve Accord, in which the two federal agencies agreed to separate federal-debt management from monetary policy. In this very limited way, the Accord acknowledged central-bank independence as a sensible monetary policy framework for price stability. Nevertheless, U.S. monetary policy remained, for at least the next two decades, largely uncommitted to an unambiguous and formal framework; as such, it was discretionary, at times influenced by Treasury, and often inflationary (Timberlake 1993, 339-40).

Finally, a mandate, though not an explicit framework, for monetary policy emerged in 1977, when Congress amended the Federal Reserve Act to instruct the central bank to “promote effectively the goals of maximum employment, stable prices, and moderate long term interest rates” (Meltzer 2009, 986). This so-called dual mandate—maximum employment and stable prices—informs Federal Reserve monetary policy to this day. Moreover, on January 29, 2012, the FOMC released its “Statement on Long-Run Goals and Monetary Policy Strategy,” in which it agreed to a single numerical inflation-target value of 2 percent based on the personal consumption expenditures (PCE) price index; the objective is sufficiently flexible so as to be consistent with the dual mandate.

End-the-Fed rhetoric notwithstanding, today, the notion that a central bank must be able to implement monetary policy independently of the political preferences of, say, members of Congress or the president is mainstream thinking among the vast majority of macroeconomists, and for good reason: independent central banks tend to achieve low and stable inflation; whereas politically influenced central banks do not. Nevertheless, central banks—the Fed included—often find themselves in the crosshairs of political controversy. In The Myth of Independence, Sarah Binder and Mark Spindel offer a persuasive argument why: essentially, the Fed has never been independent. Rather, over time, Congress has increased the central bank’s authority—all the better to blame the central bank for macroeconomic failures—while asserting, often in response to executive-branch meddling, the legislature’s ultimate control of monetary policy. At best, such a relationship is dysfunctional; at worst, it poses a grave threat to economic well-being.

References

Binder, Sarah and Mark Spindel. 2017. The Myth of Independence: How Congress Governs the Federal Reserve (Princeton: Princeton University Press)

Bordo, Michael D. and Anna J. Schwartz (1984) “The gold standard: the traditional approach.” In A Retrospective on the Classical Gold Standard, 1821-1931,ed. Michael D. Bordo and Anna J. Schwartz, 23-119 (Chicago: The University of Chicago Press)

Friedman, M. and Anna J. Schwartz. 1963. A Monetary History of the United States, 1867-1960 (Princeton, New Jersey: Princeton University Press)

Meltzer, Allan H. 2003. A History of the Federal Reserve, Volume 1: 1913 – 1951 (Chicago: The University of Chicago Press)

Miron, Jeffrey A. 1996. The Economics of Seasonal Cycles (Cambridge, MA: The MIT Press)

Timberlake, Richard H. 1993. Monetary Policy in the United States: An Intellectual and Institutional History (Chicago: University of Chicago Press)

7 thoughts on “fed up”