This blog post accompanies the SDPB Monday Macro segment that airs on Monday, January 3, 2022. Click here to listen to the segment.

The U.S. national debt is a problem, but luckily it’s a big problem. Intrigued? Welcome to the intersection of macroeconomics and global finance.

In the past year, much ink has spilled debating the U.S. national debt, how it affects the nation’s macroeconomic performance, and how it burdens future generations. To be sure, heated debates in Congress about whether to raise the nation’s debt limit—aka, debt ceiling, a congressionally authorized upper bound currently set around $31.4 trillion on the amount of national debt outstanding—are now commonplace, much to the dismay of most macroeconomists who prefer a much-less climactic budgetary process.

Meanwhile, little, if any, ink has spilled discussing a systemically important manifestation of the national debt, its alter ego, the U.S. Treasury securities market, where U.S. Treasury securities trade and where the prices and interest rates on these securities are determined. This is to say, the U.S. Treasury—the nation’s fisc (the term is the etymology of fiscal policy)—issues the national debt largely in the form of marketable U.S. Treasury securities: namely, U.S. Treasury bills, notes, and bonds, currently (face) valued at roughly $28 trillion—the size of the U.S. national debt, not coincidentally.

Bills, notes, and bonds are fixed-income debt securities the U.S. Treasury sells—the sale price is the amount the U.S. Treasury borrows at the point of sale—with the promise to pay the holder of the security a fixed U.S.-dollar-denominated face value—think, $100—at a specified future date; the arrangement may also include periodic interest (aka, coupon) payments, but ignoring them incurs no loss of generality for our purposes. Finally, the timespan between the initial sale of the security—the bill, the note, or the bond—and the specified future date on which the U.S. Treasury pays the holder of the security its face value is the security’s maturity: bills mature in a year or less, notes mature between 1 and 10 years, and bonds mature in 10 years or more. Put differently, then, the U.S. Treasury does not take out loans in the conventional way that you and I do. Rather the U.S. Treasury sells I.O.U.s in its name, something only large, well-known borrowers get to do.

The U.S. Treasury sells its securities in the primary market, where, by definition, so-called primary dealers—vetted by the Federal Reserve Bank of New York—purchase the securities from the U.S. Treasury at regularly scheduled auctions. By way of these auctions, the U.S. Treasury generates the proceeds necessary to fund spending it cannot otherwise fund with tax revenues. Currently, there are 24 primary dealers, banks and investment firms the Federal Reserve Bank of New York chooses based on (1) each dealer’s capacity and good faith to absorb at auction substantial amounts of U.S. Treasury securities and (2) each dealer’s commitment to ensure a sufficiently liquid secondary U.S. Treasury securities market, where, by definition, primary dealers and private investors trade the securities sold initially at auction in the primary market. Incidentally, primary dealers are also the counter-parties to Federal Reserve System open-market operations—the purchases and sales of U.S. Treasury (as well as other) securities in the secondary market that the central bank uses to implement its monetary policy. (For more on Federal Reserve System open-market operations see Monday Macro segment Last Resort.)

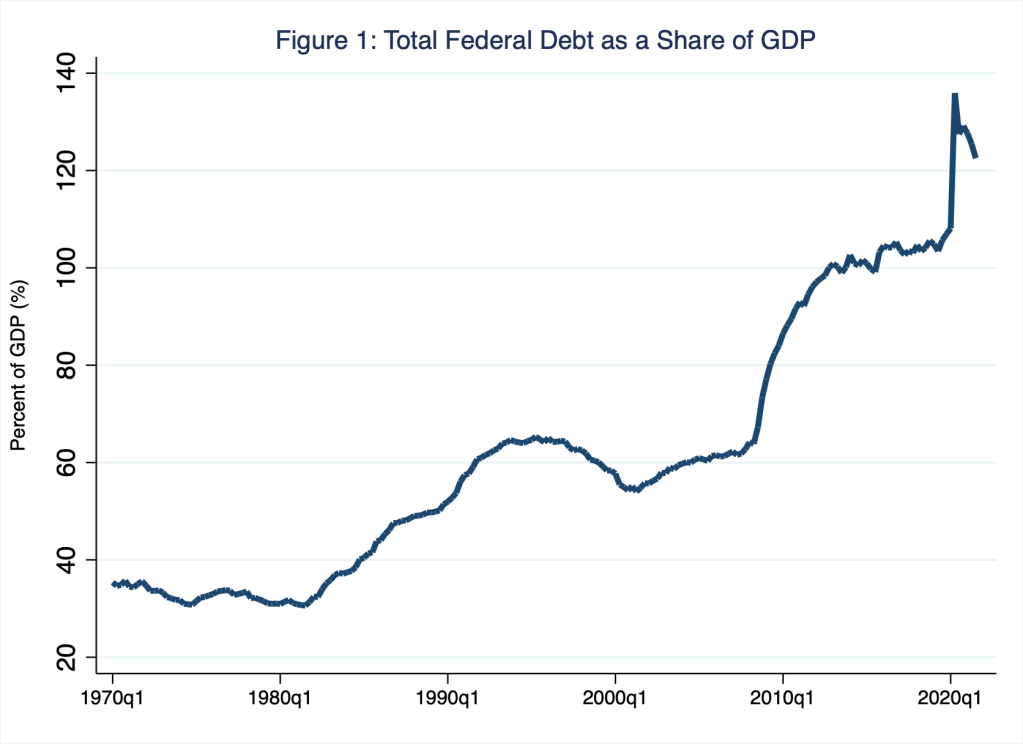

To get a sense of the size of the U.S. Treasury market, I begin with Figure 1, in which I illustrate the total amount of U.S. national debt outstanding as a share of the size of the U.S. macroeconomy, measured as GDP; in this way, we—macroeconomists and anyone else concerned about the national debt—often speak about the so-called debt-to-GDP ratio.

Figure 1 is familiar to Schooled readers who have read my analysis of whether the U.S. debt-to-GDP ratio is sustainable—spoiler alert: it’s not. (For more on the sustainability of the U.S. national debt and the U.S. government’s fiscal space to borrow even more, see Monday Macro segments, Fiscal Therapy and C-B-UH-OH.) The story of Figure 1 is well worn: since 1970, the U.S. national debt as a percentage of GDP rose from roughly 40 percent in 1970 to roughly 123 percent in the third quarter of 2021; the corresponding ratios for the U.S. national debt held by the public—that is, netting out the portion of the outstanding national debt that is owed to national-government agencies—are 27 percent and 96 percent, respectively. To be sure, the U.S. national debt is relatively large by either measure. The rather discontinuous and large increases in the debt-to-GDP ratio around 2009 and, again, in 2020 were driven by the large increases in deficit spending at those times, as well as large—or, more precisely in the case of 2020, enormous—decreases in GDP, a mechanical increase in the ratio caused by a fall in its denominator.

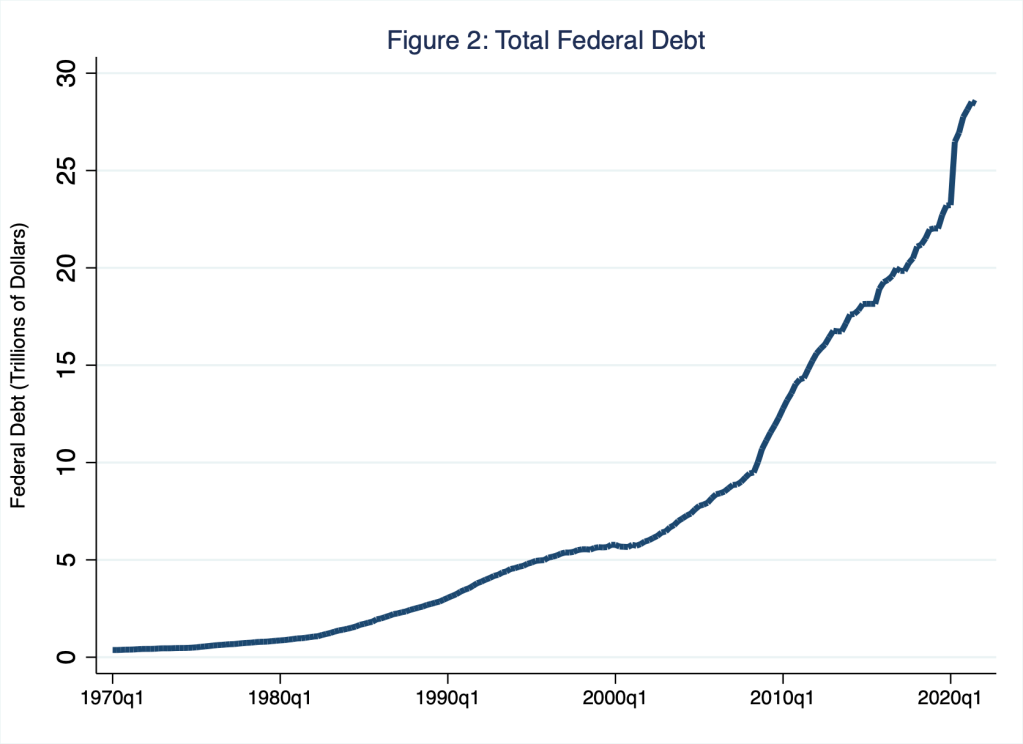

In Figure 2, I illustrate the total U.S.-dollar-denominated (face) value of the U.S. national debt, the numerator of the measure I illustrate in Figure 1; the patterns in the two figures are similar but not identical, because Figure 2 necessarily lacks the dynamics of GDP, the denominator of the measure I illustrate in Figure 1.

According to Figure 2, like its debt-to-GDP counterpart measure (Figure 1), the U.S. national debt has generally grown since 1970; the large, seemingly discontinuous vertical rise in 2020 is hard to miss. As of the third quarter of 2021, the national debt registered roughly $28 trillion, the last data point illustrated in Figure 2.

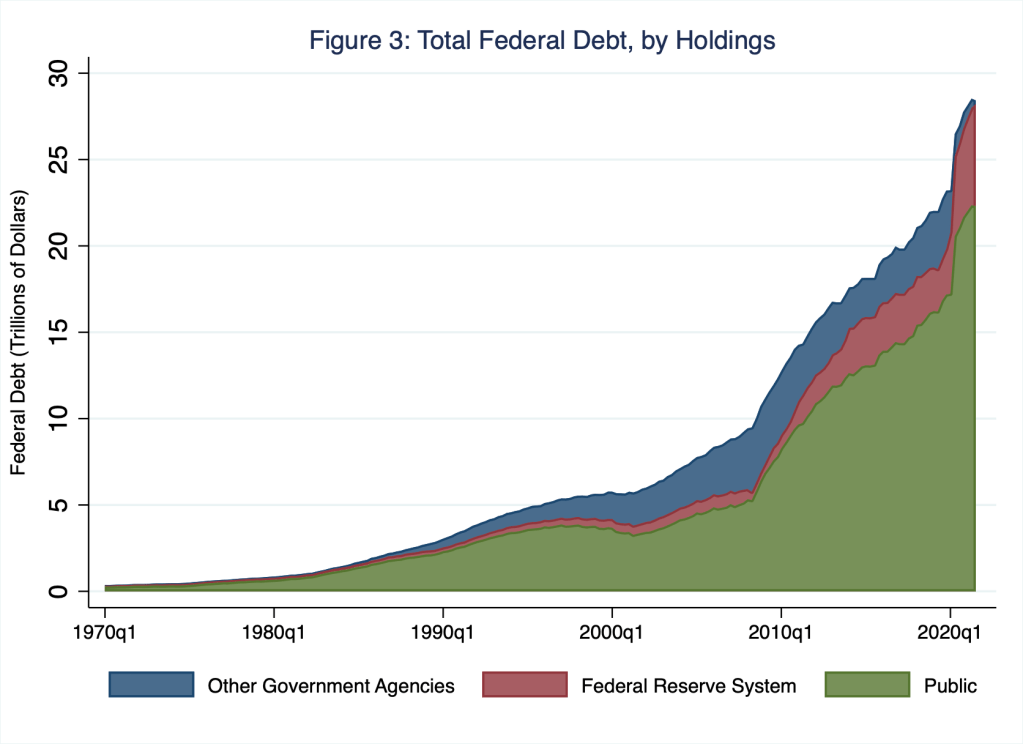

The U.S. Treasury securities that comprise the national debt are owned by the (non-U.S. governmental) public—domestic and foreign—and U.S. national government agencies. In Figure 3, I illustrate the broad composition of such debt holders, which I identify as either the (non-U.S. governmental) public, the Federal Reserve System, or other government agencies.

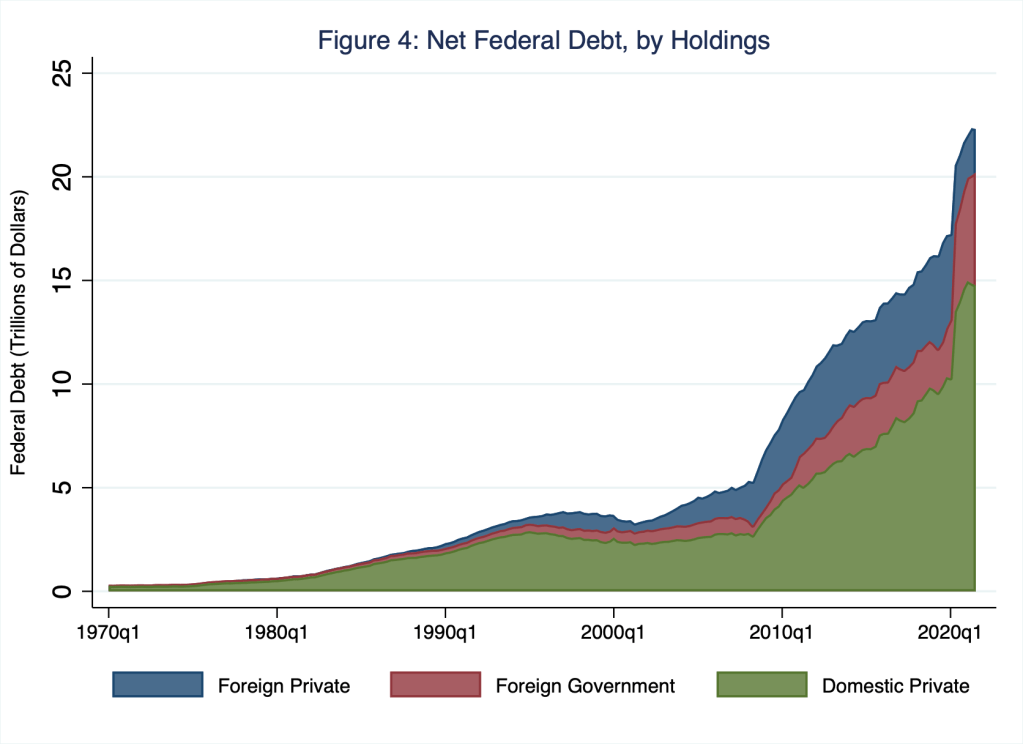

For any quarter in Figure 3, the sum of green, red, and blue areas equals the national debt—$28 trillion in the third quarter of 2021, for example. In general, the Federal Reserve System (red area) purchases and sells U.S. Treasury securities to implement the central bank’s monetary policy. Since the financial crisis, the central bank has been exceptionally active in this way: so-called quantitative easing—purchasing large quantities of financial assets, including U.S. Treasury securities to a very large extent—in response to the financial crisis around 2009 and, more recently, in response to the macroeconomic contraction imposed by the pandemic has raised rather dramatically the share of U.S. Treasury securities held by the Federal Reserve System—roughly $6 trillion as of the third quarter of 2021, according to Figure 3. Other government agencies (blue area)—think, for example, the Social Security Administration, which invests its surpluses in U.S. Treasury securities—held roughly $200 billion of U.S. Treasury securities. Finally, the public (green area)—that is, non-U.S. governmental entities, domestic or foreign—held the very-large remainder of roughly $22 trillion of U.S. Treasury securities. As a practical matter, these $22 trillion of publicly traded U.S. Treasury securities constitute the current secondary market for U.S. sovereign debt. As I illustrate in Figure 4, the holders of these securities include mostly domestic private investors (green area; roughly $15 trillion), as well as foreign governments (red area; roughly $5 trillion) and foreign private investors (blue area; roughly $2 trillion).

Full faith and credit of Uncle Sam is really a thing.

Importantly, investors throughout the global financial system unanimously perceive U.S. Treasury securities as a default-risk-free financial asset, as near to a sovereign-issued monetary store of value as one could get absent the U.S. monetary base—Federal Reserve notes in circulation and bank reserves held at the Federal Reserve. This is to say, U.S. Treasury securities embody the presumably immutable full faith and credit of the U.S. Treasury—an enviable reputation to be sure. Moreover, the U.S. Treasury securities market is exceptionally liquid: thanks to many buyers and many sellers, market participants can easily trade U.S. Treasury securities; trading-transaction costs are reliably low and prices are relatively stable. Thus, technically speaking, deep liquidity renders U.S. Treasury securities information insensitive: news that propagates potentially destabilizing one-sided trading—all buyers or all sellers—and, in doing so, generally distorts the prices of most other financial assets, leaves the prices of U.S. Treasury securities relatively unaffected.

Consequently, the global financial system relies on U.S. Treasury securities to stem systemic fragilities. “Recognizing [their] fortress-like quality, public regulation and private contracting rely systematically on Treasuries as the shield to protect capital markets against panic, collapse and runaway uncertainty” (Yadav and Yadav 2021; emphasis in the original). Indeed, U.S. Treasury securities are also the ideal collateral for that cornerstone of short-term financing, the so-called repo (or repurchase) agreement, with which a bank or an investment intermediary effectively borrows money by selling U.S. Treasury securities and simultaneously agreeing to repurchase the securities at a later date, often within a day of the sale; the positive difference between the repurchase price and the initial sale price—the so-called haircut—determines the rate of interest on this fully collateralized, safe, short-term loan. And, of course, its preferred status as a risk-free borrower affords the U.S. Treasury an extraordinary privilege to borrow at relatively low rates of interest; the nominal yields to maturity paid on U.S. Treasury securities are consistently among the lowest in the world. Moreover, these interest rates are the benchmark rates borrowers and lenders use to determine the cost of financing throughout the global financial system.

Conditional on risk-free status, bigger is better.

Thus, U.S. Treasury securities hold a special place in the global financial system because investors unanimously perceive U.S. Treasury securities as a default-risk-free financial asset and because the U.S. Treasury market is extremely liquid—necessary and sufficient conditions for the ideal information-insensitive fortress-like financial asset. Importantly, extremely safe (against default) and extremely liquid are, in principle, independent features of a financial asset. Why investors unanimously perceive a financial asset as extremely safe is, frankly, complicated; the story behind the default-risk-free status of U.S. Treasury securities is a long and winding one—a topic for another blog post. In contrast, why investors unanimously perceive a financial asset as very liquid is clearly due, at least in large part, to the size of the market for that financial asset. To be sure, the treasuries of other countries, such as Germany and Japan for example, enjoy something very much like if not identical to U.S.-styled default-risk-free status; nevertheless, the status of U.S. Treasury securities is preeminent. Why are they so special? According to one theory, there are at least 22 trillion reasons.

As I illustrate in Figure 4, roughly $22 trillion of U.S. Treasury securities trade publicly among domestic private investors (roughly $15 trillion), foreign governments (roughly $5 trillion), and foreign private investors (roughly $2 trillion). In contrast, for example, the entire, relatively large Japanese government securities market is (face) valued at roughly $14 trillion. Thus, in the world of U.S. Treasury securities, extraordinarily many buyers and extraordinarily many sellers interact in a well-organized primary-dealer led and buttressed financial market; finding a buyer or a seller of a U.S. Treasury security is reliably cheap and easy. (Though, some market observers argue rather persuasively that operational risks in secondary U.S. Treasury markets are increasingly nontrivial and serious [Yadav 2021]).

Some leading theoretical work on the sources of market liquidity and, thus, the preeminent status of a particular default-risk-free asset—think, a U.S. Treasury bond—implies that bigger is better. For example, He, Krishnamurthy, and Milbradt (2016) ask us to imagine a world in which two safe assets, A and B, trade side by side; Country A issues safe-asset A and Country B issues safe-asset B. Assume Country A issues much more debt than Country B does, so that the secondary market for safe-asset A is much larger than the secondary market for safe-asset B. In this case, fearing an illiquid market in which necessarily information sensitive financial assets trade, leading to costly price distortions, each investor seeking a safe asset will choose (ample) safe-asset A instead of (scarce) safe-asset B. Of course, if such a choice is optimal for each investor then all investors make that choice. Thus, the coordinated equilibrium, in which all investors choose safe-asset A, renders safe-asset A [safe-asset B] relatively liquid [illiquid] and, thus, information insensitive [sensitive]. Safe-asset A, made possible by Country-A’s high outstanding debt, is preeminent in this case.

So it seems at the intersection of macroeconomics and global finance, no good deed—think, low outstanding debt—goes unpunished. This is to say, in theory, more sovereign debt could be better than less sovereign debt, so long as—and this is crucial—investors throughout the global financial system unanimously perceive the sovereign-debt securities in question as default-risk-free financial assets. This is because extraordinarily liquid, information-insensitive sovereign debt markets require scale—lots of debt securities. Of course, none of this is to say that a government should increase its outstanding sovereign debt just to increase the liquidity of its sovereign-debt securities markets. To be sure, although in principle, extremely safe (against default) and extremely liquid are independent features of sovereign debt, presumably at some critically high level of outstanding sovereign debt, investors throughout the global financial system cease to perceive that sovereign debt as default-risk free.

Bigger is better, until it’s not.

References

He, Zhiguo, Arvind Krishnamurthy, and Konstantin Milbradt. 2016. “What Makes US Government Bonds Safe Assets?” American Economic Review: Papers & Proceedings, 106 (5): 519-523.

Yadav, Pradeep K. and Yesha Yadav. 2021. “Fragile Financial Regulation.” Vanderbilt Law Research Paper No. 20-46: 1-66.

Yadav, Yesha. 2021. “The Failed Regulation of U.S. Treasury Markets.” Colombia Law Review, 121 (4): 1173-1250.