![]() This blog post accompanies the SDPR Morning Macro segment that airs on Monday, May 13.

This blog post accompanies the SDPR Morning Macro segment that airs on Monday, May 13.

Macroeconomic growth relies on credit.

Credit is allocated in the financial system, where, by definition, individuals, firms, and governments with a surplus of funds—think, lenders, for example—transfer these funds to individuals, firms, and governments with a shortage of funds—think, borrowers, for example. Conceptually speaking, economists divide the financial system into two broad sectors: namely, financial markets and financial intermediaries. In financial markets, the transfer of funds is direct: an individual, firm, or government with a shortage of funds sells a security—a (direct) claim on the earnings or assets of the seller—to an individual, firm, or government with a surplus of funds. So, for example, stock and bond markets are financial markets, where equity securities (stocks) and debt securities (bonds) trade. In contrast, financial intermediaries are agents who administer the transfer of funds through the financial system; thus, in this way, the intermediated transfer of funds (from the saver to the ultimate borrower, say) is indirect. So, for example, depository institutions—banks, for the most part—are financial intermediaries.

Throughout the world, most credit is intermediated. And, the most common type of intermediary is a bank. Financial intermediation is the primary way that credit travels through the financial system for several reasons. First, by maximizing profits in response to competitive forces, financial intermediaries reduce the transaction costs of engaging in financial transactions. Second, by transforming short-term bank accounts (and other sources of short-term funding) into long-term loans (and other uses of short-term funding), financial intermediaries bridge a time-to-maturity gap that would otherwise impede the provision of credit. Third, by performing all manner of (fundamentally similar) financial services, financial intermediaries achieve economies of scope—underwriting a loan for the purchase of a recreational watercraft is relatively easy and inexpensive for an intermediary that already underwrites, say, loans for the purchases of automobiles. And fourth, and perhaps most importantly, by minimizing asymmetric-information problems, financial intermediaries allocate credit more efficiently than the financial system could otherwise.

An asymmetric-information problem is a form of market failure in which two parties to a contract do not have the same information. For concreteness, consider two parties to a loan contract: namely, the lender and the borrower. In this case, the information asymmetry (of consequence) occurs because the lender knows less about the borrower—her creditworthiness, her intentions to pay her debts, and so forth—than the borrower knows about the borrower. In effect, asymmetric information problems impede the provision of credit—this is the market failure. In the absence of information, lenders ration credit, providing it only to those about whom lenders have sufficient information. As a practical matter, credit rationing tends to impede the provision of credit to relatively small, unknown entities in the economy—think, for example, households and sole proprietorships. Thanks to their strong community ties, long-term customer relationships, and expertise in specific segments of the economy, financial intermediaries solve asymmetric-information problems in ways that financial markets, operating through direct finance, never could. An important corollary follows from this line of reasoning: relatively small, unknown entities in the economy depend on financial intermediaries—banks, for the most part—for credit.

Not surprisingly, perhaps, evidence that the supply of intermediated credit causes economic growth is difficult to demonstrate. As usual, reverse casualty may be at work: yes, the provision of credit rises and falls with economic output; but does the provision of credit cause economic output or does economic output—think, aggregate demand—cause the provision of credit? Careful investigations of this causal relationship abound. For example, Bernanke (1983) demonstrates that, for various reasons, the Great Depression severely compromised the abilities of financial intermediaries to solve asymmetric information problems; consequently, “some borrowers (especially households, farmers, and small firms) found credit to be expensive and difficult to obtain. The effects of this credit squeeze on aggregate demand helped convert the severe but not unprecedented downturn of 1929-30 into a protracted depression” (257). In a more-recent example, Klein, Peek, and Rosengren (2002) demonstrate that financial troubles in the Japanese banking sector in the 1990s reduced the supply of credit to bank-dependent firms, thereby reducing their foreign-direct investments in the United States. As with Bernanke (1983), these authors conclude that the fall in the supply of credit caused a reduction in aggregate demand.

Okay, banks matter; so what?

For reasons I describe below, the number of banks in the United States has fallen persistently since at least the 1990s. Moreover, for the most part, this persistent fall has occurred because banks have merged with or acquired one another. In other words, bank failures, which have occurred to a lesser extent, are not primarily responsible for the persistent fall in the number of banks; rather, on average, banks have grown larger. Meanwhile, as the Economist magazine reports this week, information technology is violently disrupting traditional banking. How this pattern will ultimately affect bank customers remains to be seen. Customers who seek transactional banking may appreciate the high-volume, low-touch models common to most larger institutions; meanwhile, customers who seek relationship banking may prefer the high-touch models common to most smaller institutions—community banks, in the parlance of financial intermediation—for which relationship banking is, in effect, a solution to the asymmetric-information problems that relatively small-scale borrowers present. To put the matter bluntly, to some of us, relatively small community banks represent extra credit we do not seek, while to others, relatively small community banks represent the only credit available.

The United States relies on a so-called dual banking system, in which depository institutions broadly defined—commercial banks, savings associations, and credit unions—hold either a national/federal charter or a state charter. The Office of the Comptroller of the Currency charters national commercial banks and federal savings associations; state financial authorities charter state commercial banks, savings associations, and credit unions; and, the National Credit Union Administration (NCUA) charters federal credit unions. Institutions that hold a national/federal charter must insure their deposits (and shares in the case of credit unions); state-chartered institutions have the option to insure and the vast majority do. The Federal Deposit Insurance Corporation (FDIC) insures deposits of banks and savings associations; the NCUA insures deposits and shares of credit unions. Finally, national commercial banks and federal savings associations must be members of the Federal Reserve System; state commercial banks and savings associations have the option to be members.

As of June 2018, the FDIC reported that 5,541 FDIC-insured commercial banks and savings associations operated in the United States; of these institutions, 4,833 were commercial banks and the remaining 708 were savings associations. In Table 1, I report this information, alongside information on charter types, Federal Reserve System membership, and commercial banks and savings associations in South Dakota.

Table 1: FDIC-Insured Depository Institutions, June 2018

| United States | South Dakota | |||

| Charter | Commercial | Savings | Commercial | Savings |

| National/Federal | 850 | 320 | 19 | 4 |

| State | 3,983 | 388 | 61 | – |

| Fed Member | 764 | 350 | 8 | – |

| Fed Nonmember | 3,219 | 38 | 53 | – |

| Total | 4,833 | 708 | 80 | 4 |

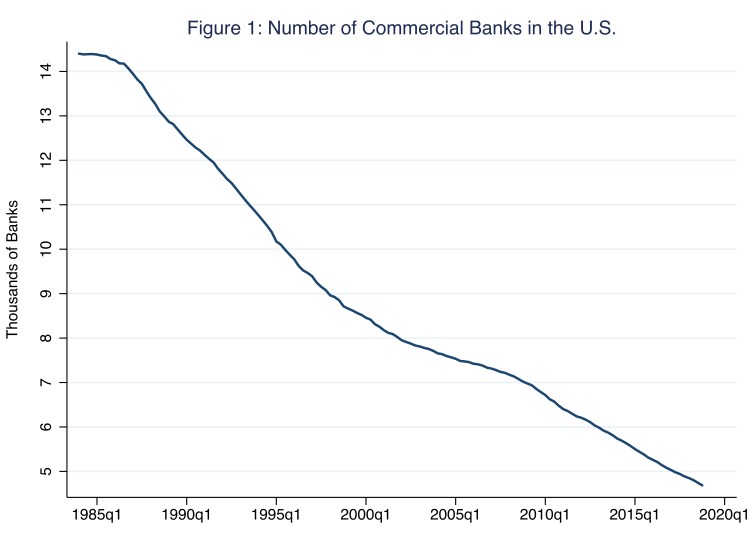

According to Table 1, the majority of commercial banks (82 percent) and savings associations (55 percent) in the United States hold state charters; and the majority of state-chartered commercial banks (81 percent) are not members of the Federal Reserve System. These patterns are evident in South Dakota, where the majority of commercial banks in the state (76 percent) hold state charters; and the majority of state-chartered commercial banks (87 percent) are not members of the Federal Reserve System. The four savings banks in South Dakota hold a federal charter. In any case, the number of banks in the United States today is far smaller than the number just a few decades ago, when interstate-branching restrictions in place since the McFadden Act of 1927 were lifted, allowing banks to merge; along the way, some banks failed as well. In Figure 1, I illustrate the number of commercial banks operating in the United States since the first quarter of 1984.

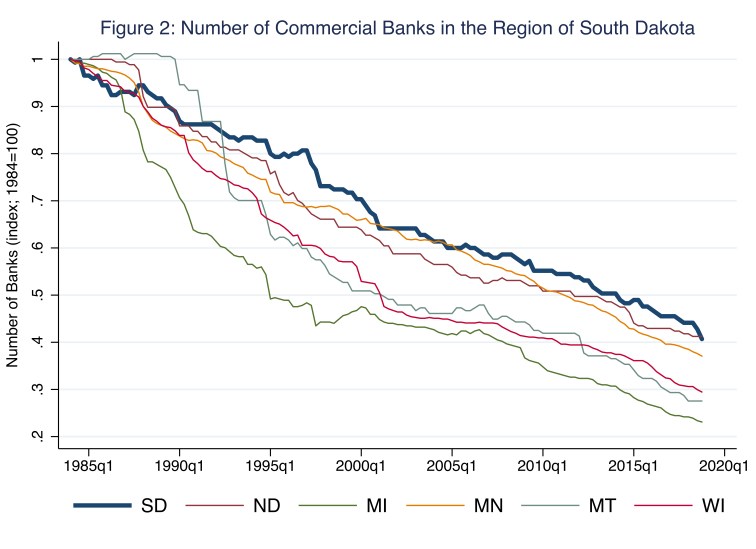

According to Figure 1, in the first quarter of 1984, 14,400 commercial banks operated in the United States; in the fourth quarter of 2018, the comparable figure was 4,687. The decline in commercial banking that Figure 1 illustrates has occurred among savings associations and credit unions as well. In all cases, the declines are due, to a very large extent, to mergers and acquisitions. Financial intermediaries generally incur relatively high fixed costs and relatively low marginal costs—consider, for example, the cost of servicing one additional deposit account, complying with one additional regulation, or implementing one additional information-technology-enhanced service. Thus, in banking, profit maximization—and, necessarily, cost minimization—incentivizes banks to increase the scale (and scope) of their operations. The national pattern evident in Figure 1 is also evident at the state level. In Figure 2, I illustrate (as an index) the numbers of commercial banks operating in South Dakota and the five other states served, in whole or in part, by the Federal Reserve Bank of Minneapolis.

According Figure 2, the decline in commercial banking in South Dakota has been less pronounced than the declines throughout the ninth district more generally. For example, in the first quarter of 1984, 145 commercial banks operated in South Dakota; in the fourth quarter of 2018, the comparable figure was 59, or 41 percent of 145; in Figure 2, 41 percent is the last data point associated with the series for South Dakota. In contrast, the decline in, say, Michigan, has been far more pronounced: in the first quarter of 1984, 368 commercial banks operated in Michigan; in the fourth quarter of 2018, the comparable figure was 85, or 23 percent of 368; in Figure 2, 23 percent is the last data point associated with the series for Michigan. Not surprisingly, because the decline in the number of depository institutions is largely the result of banks merging with or acquiring one another, banks throughout the United States have grown larger. In Table 2, I report, for the years 1998 and 2018, the percentage shares of commercial banks and savings associations according to FDIC-defined asset categories, or buckets.

Table 2: FDIC-Insured Commercial Banks and Savings Associations by Assets

| 1998 (10,734 institutions) | 2018 (5,550 institutions) | |||

| Assets | of Banks | Cumulative | of Banks | Cumulative |

| Less than $45 Million | 14% | 14% | 2% | 2% |

| $25 Million to $50 Million | 21% | 35% | 7% | 9% |

| $50 Million to $100 Million | 24% | 59% | 16% | 25% |

| $100 Million to $300 Million | 26% | 86% | 36% | 60% |

| $300 Million to $500 Million | 5% | 91% | 14% | 74% |

| $500 Million to $1 Billion | 4% | 95% | 12% | 86% |

| $1 Billion to $3 Billion | 3% | 98% | 8% | 94% |

| $3 Billion to $10 Billion | 1% | 99% | 3% | 98% |

| Greater than $10 Billion | 1% | 100% | 2% | 100% |

| Total | 100% | 100% | ||

According to Table 2, depository institutions were, on average, larger in 2018 than in 1998. To see this pattern, consider, for example, the row associated with the asset bucket, “$50 Million to $100 Million.” In 1998, based on the column headed, “of Banks,” 24 percent of FDIC-insured institutions (or 2,629 of 10,734 institutions) had assets valued between $50 million and $100 million; meanwhile, based on the column headed, “Cumulative,” 59 percent of institutions (or 6,382 of 10,734 institutions) had assets valued at $100 million or less. In contrast, in 2018, 16 percent of FDIC-insured institutions (or 868 of 5,550 institutions) had assets valued between $50 million and $100 million; meanwhile, 25 percent of institutions (or 1,372 of 5,550 institutions) had assets valued at $100 million or less. Meanwhile, at the top of the asset distribution (and, so, at the bottom of Table 2), in 1998, 82 institutions had assets valued at $10 billion or more; in 2018, the comparable number of institutions was 136. To be sure, the asset bucket “Greater than $10 Billion” is somewhat misleading; for example, as of May 9, 2019, the FDIC reported nine institutions each held total assets valued at more than $250 billion and one institution, JPMorgan Chase & Co., held total assets valued at more than $2 trillion.

Incidentally, this nationwide distribution of banks across asset buckets is evident at the state level as well. For example, as of May 9, 2019, the FDIC reported 83 percent of institutions domiciled in South Dakota each held total assets valued at less than $1 billion (when the comparable figure for the nation as a whole was 86 percent); 70 percent held total assets valued at less than $500 million (when the comparable figure for the nation as a whole was 74 percent). Meanwhile, a few relatively large banks operate in the state as well. In Table 3, I report the ten largest FDIC-insured depository institutions domiciled in South Dakota. To be sure, the consumer-credit operations of a few exceptionally large institutions skew the state-level distribution; nevertheless, the story for the nation holds for the state: most institutions in the state are relatively small; meanwhile, the number of institutions in the state is falling, as the average size of an institution is growing via mergers and acquisitions.

Table 3: Largest FDIC-Insured Depository Institutions in South Dakota, December 2018

| Institution | City | Total Assets |

| Wells Fargo Bank | Sioux Falls | $ 1,689,351,000 |

| Citibank | Sioux Falls | 1,406,717,000 |

| TCF National Bank | Sioux Falls | 23,708,028 |

| Great Western Bank | Sioux Falls | 12,568,651 |

| MetaBank | Sioux Falls | 6,168,996 |

| Dacotah Bank | Aberdeen | 2,567,120 |

| First Bank & Trust | Brookings | 1,952,920 |

| First PREMIER Bank | Sioux Falls | 1,761,153 |

| First Dakota National Bank | Yankton | 1,673,536 |

| The First National Bank in Sioux Falls | Sioux Falls | 1,245,686 |

As financial concerns, depository institutions—no matter their size—endeavor to maximize profits and, more specifically, to maximize return on equity. And, in the years since the financial crisis, maximizing return on equity has been particularly challenging for many financial institutions in the United States and around the world more generally. Thus, because profit maximization requires cost minimization, and banks benefit from economies of scale, the pressure on banks to grow larger has been particularly strong. To understand why, consider return on equity (ROE), which we define as profits (π) divided by equity (E)—or the ownership stake in the firm—as follows.

ROE = π / E

Next, decompose ROE as follows.

ROE = (π / A) × (A / E)

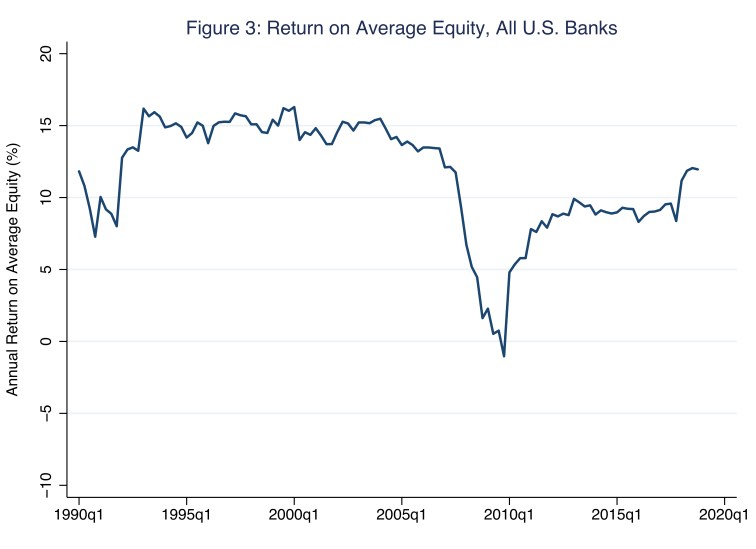

In this expression, the term π / A is return on assets (ROA) and the term A / E is the so-called equity multiplier. (In any case, the right-hand side of this expression simplifies to π / E—that is, ROE—so we know the decomposition is valid.) According to this decomposition, the primary drivers of ROE are ROA and debt financing—that is, financing assets with debt as opposed to equity and, in doing so, setting the ratio of assets to equity (A / E). In Figure 3, I illustrate ROE for all U.S. commercial banks since 1990.

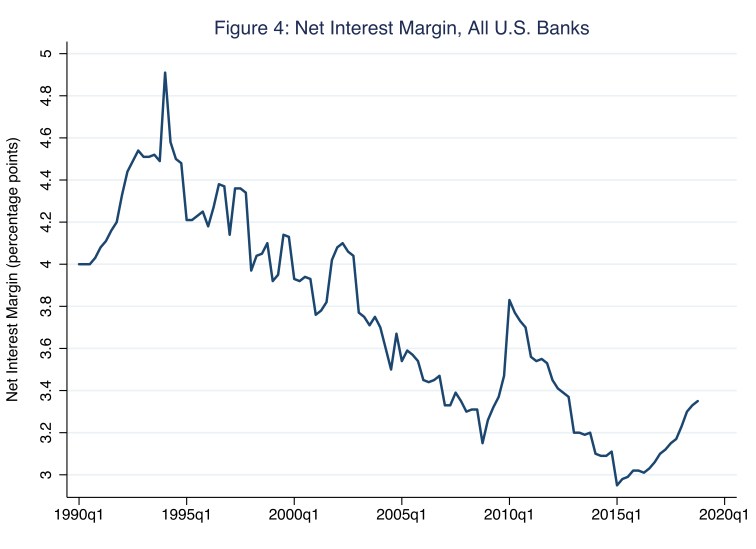

According to Figure 3, before the financial crisis of 2008 (and after the banking crisis of the early 1990s), return on average equity for all U.S. banks averaged about 15 percent; since the financial crisis, this return has, until only very recently, averaged about 10 percent. The reasons for this post-crisis persistent fall in ROE are evident in the earlier decomposition. First, a persistent fall in the net interest margin—the difference between the interest rate a bank earns on its uses of funds (say, loans) and the interest rate a bank pays for its sources of funds (say, savings deposits)—has restrained profits and, thus, ROA. In Figure 4, I illustrate the net interest margin for all banks.

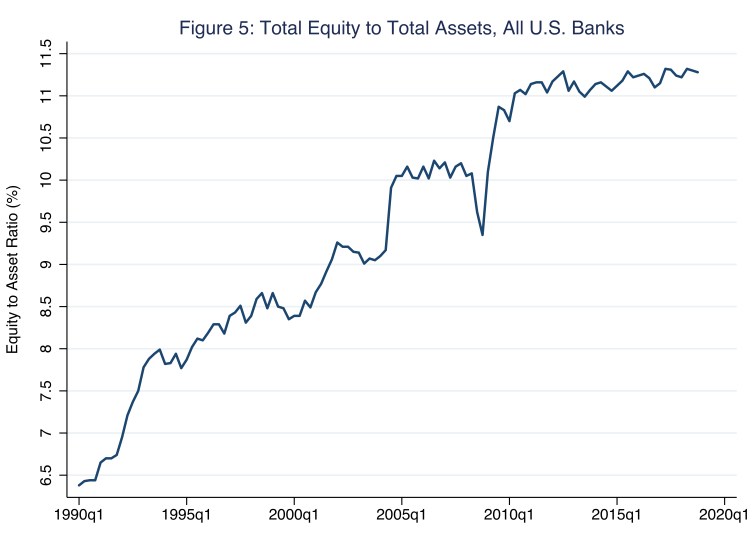

The net interest margin closely mimics general patterns in the yield curve—the relationship between interest rates or so-called yields to maturity on short-term bonds (like those that mature in, say, one year) and long-term bonds (like those that mature in, say, 10 or 30 years); for more on the yield curve, see the Morning Macro segment, “Yield Ahead.”). As the yield curve flattens, net interest margin tends to shrink, compromising profitability and ROA accordingly. Only recently has net interest margin risen, and even then, only slightly. Meanwhile, a persistent rise in the ratio of equity to assets—and, thus, a persistent fall in the ratio of assets to equity (A / E)—has restrained leverage. In Figure 5, I illustrate the ratio of equity to assets for all banks.

According to Figure 5, since the financial crisis, banks have generally increased the amount of equity they hold against their assets. Put differently, banks have drawn relatively more on equity as opposed to debt as a source of funds; doing so necessarily increases the financial resilience of these institutions, which are now better positioned to take losses, while it reduces ROE.

In summary, then, the pressures to maximize profits and, thus, minimize costs in an increasingly well-capitalized and information-technology-rich banking industry will continue to reduce the number of banks operating in the United States; meanwhile, these pressures will continue to increase the size of the average bank. There is no doubt that these patterns will significantly disrupt the banking industry. Meanwhile, how these patterns will ultimately affect the banking public—savers and borrowers—remains an open question. So long as relatively large banks and relatively small banks suit different sets of consumer preferences, one outcome is certain: there will be winners and losers.

References

Bernanke, Ben S. 1983. “Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression.” The American Economic Review, 73:257-276

Klein, Michael W., Joe Peek, and Eric S. Rosengren. 2002. “Troubled Banks, Impaired Foreign Direct Investment: The Role of Relative Access to Credit.” American Economic Review, 92:664-682

2 thoughts on “extra credit”