This blog post accompanies the SDPB Monday Macro segment that airs on Tuesday, January 2, 2024. Click here to listen to the segment. For more macroeconomic analysis, follow J. M. Santos on Twitter @NSMEdirector.

In the September 19, 1966 issue of Newsweek, Nobel laureate American economist Paul Samuelson quipped, “Wall Street indexes predicted nine out of the last five recessions! And its mistakes were beauties.” Nine is greater than five; get it? Since then, macroeconomic enthusiasts—professionals and amateurs, alike—have generalized the sentiment; these days, we often hear something like, “economists have predicted nine of the last five recessions.” Still quippy.

Inaccurate predictions of recessions prevailed in 2023—a “dreadful year” for economists, according to the Economist magazine, during which “Mistaken recession calls were just part of it.” The rest of it included questionable empirical measures of income inequality (which, after accounting for taxes and transfers, may be no worse than in 1960), the costs—to housing construction and, thus, to the size of GDP—of zoning restrictions (which may not restrict the size of GDP as much as we thought), social mobility (which may be better than we thought, because social mobility early on was worse than we thought), and deaths of despair driven by drug overdoses (which may have less to do with desperate responses to labor-market prospects—the causes of overdose deaths of despair Angus Deaton and Anne Case popularized—and more to do with proximity to smuggled fentanyl).

From the dreadful year, the magazine offered three rather optimistic takeaways—resolutions, as it were: replicate extant studies—and arrive at different conclusions—because doing so is crucial work, nothing to be ashamed of in a social science that blends theory and practice; return to theory, the pendulum has swung too far toward practice—read, empirical work—as an unintended consequence of the opprobrium economic theorists received in the wake of the global financial crisis; and cheer up, because the alternative empirical measures researchers proposed in 2023 signaled good news: no recession, less income inequality, and fewer deaths of despair, for example.

I offer a fourth takeaway: for 2024, economists should resolve to keep thinking and working like economists, detractors be damned. Sometimes economists get it wrong and often we disagree (or, as I like to say, we vigorously interrogate ideas); but we consistently work from a generally accepted and rigorously reasoned body of knowledge. Let’s own that proudly. Economics, like space, is really hard.

Economics is a social science of decision making under the condition of scarce resources, including scarce or incomplete information—about the present or the future. Economists study the production, distribution, and consumption of goods and services; and in doing so, we analyze how individuals, businesses, governments, and societies more generally allocate limited resources to satisfy unlimited needs and wants. Sometimes we forecast—accurately or otherwise, often otherwise—economic outcomes, of course; but most times we examine economic behavior and its influences—think, incentives, prices, market structures, and public policies, for example—to understand economic phenomena to enhance efficiency and social welfare. Predicting a recession is interesting, yes; but modeling and, thus, understanding how a recession and government-policy responses to it shape household-level standards of living and innovation, for example, is more important.

The generally accepted and rigorously reasoned body of knowledge from which economists work is based on several principles. I focus on the ten Harvard economist Greg Mankiw (2021) enumerates in his well-known principles textbook. And then I return to the recession of 2023 that was not.

Stick to your principles.

First, because resources are scarce, people face trade-offs, such as whether to produce, distribute, and “consume” industrial goods—guns, in economics parlance—versus consumer goods—butter, in economics parlance; or whether to maximize efficiency—think, pay the most-productive workers the most—or equality—think, distribute income uniformly across all workers, unconditional on their productivity.

Second, because people face trade-offs, the true (opportunity) cost of something is what we give up to get it. For undergraduate students studying economics at South Dakota State University, for example, the true cost of attending university includes tuition, fees, and forgone income a student could have earned had they not attended university.

Third, people, whom economists assume to be (mostly) rational, think at the margin. Rational people make decisions by using all available information in the most sensible ways. And a rational person chooses action A if the marginal—think, additional—benefit of choosing action A exceeds the marginal cost of choosing action A. Thus, rational people pay more for diamonds than water—even though only the latter sustains life—and never throw good money after bad; sunk costs are just that: sunk.

Fourth, people respond to incentives, which effectively determine the marginal benefits or marginal costs of actions. Policymakers ignore incentives at their—and our—peril. To ignore incentives in a market economy, where marginal benefits and marginal costs determine outcomes, is to produce unintended—and, most likely, unwanted—consequences.

Fifth, trade can make everyone better off. Trade is, in effect, a production technology that increases efficiency, effectively allowing an economy to transform inputs—the goods and services the economy produces at a comparative advantage but does not desire—into outputs—the goods and services the economy desires but does not produce at a comparative advantage. Absent trade, an economy must be self sufficient—an autarky, in the parlance of international economics. An autarky necessarily ignores the objective of productive efficiency and, along with it, (opportunity) cost minimization. All else equal, then, international trade increases an economy’s standard of living. The terms of trade between nations are, at times, contentious. And, to be sure, such contentiousness is occasionally warranted; not all terms of trade—including, say, the institutions that govern ownership of intellectual property—are fair. Nevertheless, more often than not, opponents of international trade object to so-called trade imbalances, a pejoratively tinged term that, as a matter of fact, simply describes an aggregate-expenditures outcome in which imports exceeds exports. Exports measure the value of goods and services produced domestically and sold abroad; while imports measure the value of goods and services produced abroad and sold domestically. Most economists do not support this objection or its ostensible corollary: trade imbalances are the work of unscrupulous trading partners. Rather, most economists favor openness and view trade imbalances as the result of domestic features of a macroeconomy. (For more on trade, see Monday Macro segment, “Traitors.”).

Sixth, an economy’s standard of living depends on its productivity. Productivity—and, specifically, labor productivity—is a measure of the average level of output—think, stuff—produced per hour of labor input. The amount of capital, like the machines and tools with which we equip labor, and the production technology, the recipes with which we combine labor and capital, determine labor productivity. Over time, increases in the amount of capital and improvements in technology grow labor productivity.

Seventh, markets are usually a good way to organize economic activity, because markets are decentralized allocation mechanisms that rely on the decisions of many (utility-maximizing) consumers and (profit-maximizing) firms that interact in marketplaces. Generally, economists reason productivity—the principal driver of economic growth and, thus, increases in our standard of living—is most likely to grow in an economic system of sensibly regulated market capitalism, complete with specialization and exchange (including international trade), as opposed to centrally planned communism (where free enterprise and private property are prohibited). To sustain high economic growth in a non-market economy, a central planner must rely on capital accumulation (aka, capital deepening)—as opposed to innovation and technological growth that market incentives inspire—to the point of repressing consumption. And, even then, the returns to such a repressive, welfare-reducing approach eventually disappear.

Eighth, governments can sometimes improve market outcomes. Sensibly regulated market capitalism relies on institutions that enforce property rights that allow people in an economy to own and control scarce resources; recall, people respond to incentives, if people do not own and control it, they will not manage it efficiently. Moreover, government can directly improve efficiency—think, the size of the economic pie—or equality—think, the slices of the economic pie; and government can stabilize the economy. Allocation policy shapes (long-run) features of economic growth and labor productivity; redistribution policy reshapes the (extant) distribution of income and wealth across households; and, stabilization policy shapes the (short-run) features of the business cycle, those irregular fluctuations in aggregate economic activity—expansions and recessions, for example—we closely associate with inflation and unemployment. Conventional monetary policy is stabilization policy, for example.

Ninth, the quantity of money determines the average price level. Put differently, inflation—a continual rise in the average price level—is ultimately a monetary phenomenon: the outcome of too much money chasing too few goods. The implication economists take from this proposition is that inflation—think, a fall in the purchasing power of money—is uniquely and ultimately an outcome of monetary policy. Monetary policy is a macroeconomic stabilization policy conducted by a central bank when it targets the money supply, interest rates, and aggregate demand to achieve macroeconomic outcomes, including low and stable inflation and full employment. (For [a lot] more on the relationship between money and the average price level, see Monday Macro segments, “Always and Everywhere,” “Exit Velocity,” and “It’s Only Money.”)

Tenth, an economy faces a short-run trade-off between rates of inflation and unemployment: as the rate of unemployment falls, the rate of inflation rises, a relationship we typically depict graphically with a downward sloping Phillips curve, for which the rate of inflation is measured on the vertical axis and the rate of unemployment is measured on the horizontal axis. The idea of the Phillips curve trade-off has enormous intellectual influence in macroeconomic theory and policy—think, the Federal Reserve dual (and, in the short run, internally conflicting) mandate of high employment and low and stable inflation. The Phillips curve revolutionized macroeconomic policy. (For more on the Phillips curve, see Monday Macro segment, “Revolutions.”)

No recession in 2023, in principle(s).

Our economic principles are the building blocks of our explanations of economic phenomena, including business cycles. Indeed, on the basis of the principles (and the benefit of hindsight, of course), we could explain why inaccurate predictions of recessions prevailed in 2023.

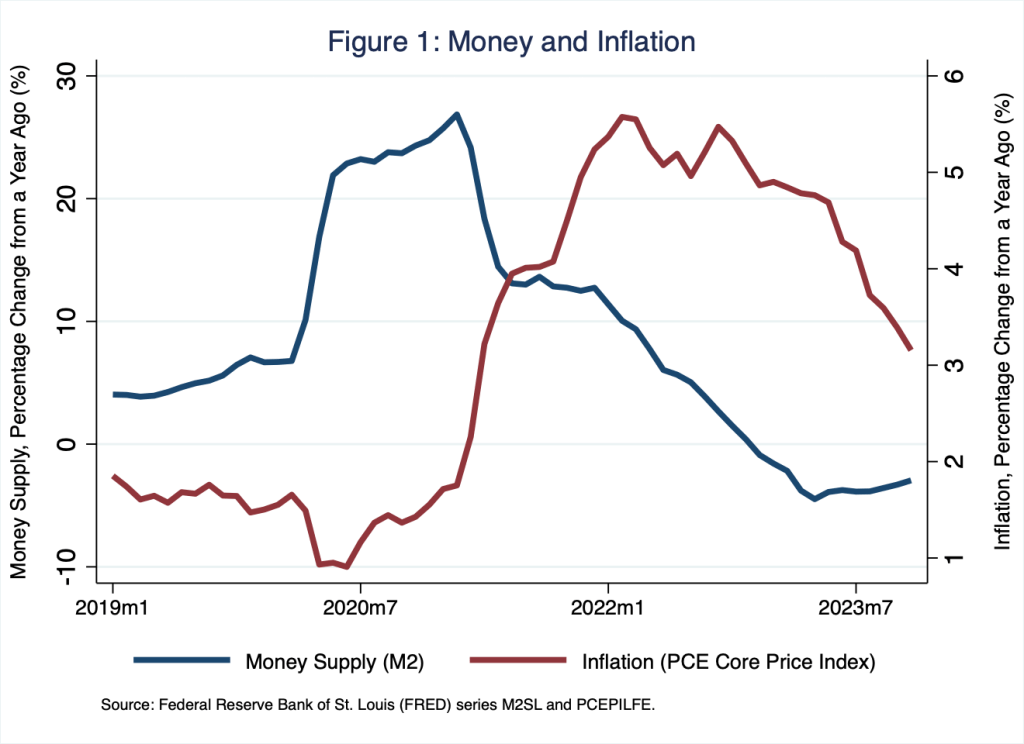

As Schooled readers know well, in about the last two years, monetary policymakers engineered a steep disinflation, producing a fall in the rate of inflation—measured by the core personal consumption expenditures (PCE) chain-type price index, which excludes food and energy—from 5.6 percent in February 2022 to 3.2 percent in November 2023. Today, monetary policy is the stabilization policy of choice in the U.S. economy (Principle 8). To accomplish the disinflation, policymakers reduced the quantity of money. To see this relationship between the quantity of money and the rate of inflation (Principle 9), consider Figure 1, in which I illustrate the growth in the quantity of money (blue line) and the rate of inflation (red line), based on the PCE core from just before the pandemic to now.

According to Figure 1, the exceptional growth in the quantity of money preceded by about one year the exceptional growth in the rate of inflation; this one-year-long lag between the growth rate of the quantity of money and the rate of inflation is typical: most estimates of the lag, which can vary from inflationary episode to inflationary episode of course, fall within 12 to 18 months. Likewise, an exceptional fall in the quantity of money preceded the current fall in the rate of inflation by about one year as well.

Reducing inflation is important. Low and stable inflation, what macroeconomists refer to as price stability, is essential in a market economy (Principle 7), in which relative prices—the price of coffee relative to the price of tea or the price of gasoline relative to the price of coal, for example—rightly inform decisions of households, firms, and governments, provided the purchasing power of money is stable. Price stability allows a market economy to allocate resources efficiently through trade (Principle 5), driving labor productivity and, thus, the standard of living (Principle 6).

A dual (Congressional) mandate informs Federal Reserve monetary policy: the central bank must achieve stable prices (or, practically speaking, low and stable inflation) and maximum employment (or, put differently, low unemployment). To aim simultaneously at its two targets, the central bank has one instrument, namely, the federal funds rate. Thus, because resources are scarce (Principle 1)—think, one instrument for two targets—the central bank confronts a trade-off and corresponding opportunity costs (Principle 2): the opportunity cost of achieving price stability [full employment] is disregarding maximum employment [price stability]. The short-run trade-off between inflation and employment has enormous intellectual influence in macroeconomic theory; policymakers, macroeconomists, and economic forecasters have the Phillips curve on their minds (Principle 10).

Economists expect disinflation to be costly in terms of employment and output; put differently, we expect disinflation to trigger recession. As the rate of inflation falls, workers who expect inflation to persist resist low or no cost of living adjustments and bargain instead for relatively high nominal wages, because workers respond to incentives (Principle 4) of higher real wages. In any case, higher real wages reduce the demand for labor and, thus, employment, inducing recession. Unless, of course, workers are rational and information the central bank is credibly committed to reducing inflation is available, in which case, workers use the available information in the most sensible ways (Principle 3): workers rightly reason a relatively high nominal wage—and thus, a relatively high real wage—is unwarranted; higher real wages do not materialize to reduce the demand for labor and, thus, employment. The disinflation is costless: predictions of recessions in 2023 prove inaccurate.

Economists may have predicted nine of the last five recessions, but our economic principles explain why each recession occurred, teaching us about what might cause the next one and how economic policy might mitigate its negative effects on household standards of living, knowledge we could use to improve standards of living in the future. Our economic principles are powerful ground truths we apply to understand all manner of economic phenomena—macroeconomic and otherwise. In 2024, economists will get it wrong now and then, of course; but we will learn from our mistakes—our forecast errors, our measurement errors, and our modeling errors, for example. We will end the year with a deeper understanding of economics, no apologies necessary.

References

Mankiw, N. Gregory. 2021. Principles of Macroeconomics. Boston, MA: Cengage Learning, Inc.